Das könnte Ihnen auch gefallen

- CH 02Dokument84 SeitenCH 02Muhammad OwaisNoch keine Bewertungen

- Overview of Financial Accounting: Prasanna Kulkarni Chartered AccountantDokument29 SeitenOverview of Financial Accounting: Prasanna Kulkarni Chartered AccountantDhaval MehtaNoch keine Bewertungen

- Rulesofdebitandcredit 101029141535 Phpapp01Dokument85 SeitenRulesofdebitandcredit 101029141535 Phpapp01Elyse CameroNoch keine Bewertungen

- Analyzing TransactionsDokument85 SeitenAnalyzing TransactionswarsimaNoch keine Bewertungen

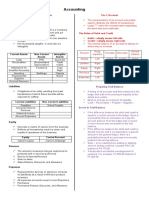

- What Is Accounting? What Is Accounting?Dokument22 SeitenWhat Is Accounting? What Is Accounting?akg gNoch keine Bewertungen

- The Accounting Cycle:: Capturing Economic EventsDokument44 SeitenThe Accounting Cycle:: Capturing Economic Eventsasifmalik2Noch keine Bewertungen

- Lec 7 8 9 10Dokument47 SeitenLec 7 8 9 10zee.k1ra7Noch keine Bewertungen

- Accounting: Assets Liabilities + Equity A L + EDokument4 SeitenAccounting: Assets Liabilities + Equity A L + EJohn LeeNoch keine Bewertungen

- Lesson 2 3 CashflowDokument3 SeitenLesson 2 3 CashflowGeraldine MayoNoch keine Bewertungen

- Fma 03 (I)Dokument43 SeitenFma 03 (I)Av ElaNoch keine Bewertungen

- Basic Accounting - First BridgingDokument20 SeitenBasic Accounting - First BridgingMae NamocNoch keine Bewertungen

- Chapter 2Dokument23 SeitenChapter 2Abrha636100% (1)

- Accounting at A GlanceDokument14 SeitenAccounting at A GlanceNiyaz AhamedNoch keine Bewertungen

- Introduction to Accounting BasicsDokument14 SeitenIntroduction to Accounting BasicsAmrinNoch keine Bewertungen

- Use The Accounting Equation To Analyze Business TransactionsDokument36 SeitenUse The Accounting Equation To Analyze Business TransactionsPradeep GuptaNoch keine Bewertungen

- Analyzing and Recording TransactionDokument24 SeitenAnalyzing and Recording TransactionĐàm Quang Thanh TúNoch keine Bewertungen

- Accounting BasicsDokument21 SeitenAccounting BasicsasifparwezNoch keine Bewertungen

- Accounting: Assets Liabilities + Equity A L + EDokument4 SeitenAccounting: Assets Liabilities + Equity A L + EjermaineNoch keine Bewertungen

- Basics of AccountingDokument30 SeitenBasics of AccountingNaina_Dwivedi_6514Noch keine Bewertungen

- Module 001: Review of The Basic Accounting Concepts and PrinciplesDokument18 SeitenModule 001: Review of The Basic Accounting Concepts and PrinciplesHo Ming LamNoch keine Bewertungen

- Bean Counter's Accounting and Bookkeeping "Cheat Sheet": Provided byDokument6 SeitenBean Counter's Accounting and Bookkeeping "Cheat Sheet": Provided byJoannah SalamatNoch keine Bewertungen

- BSBA 1 Topic 4 2022 For The StudentsDokument4 SeitenBSBA 1 Topic 4 2022 For The StudentsshanehermoginoNoch keine Bewertungen

- Module 4 - Double Entry Bookkeeping System and The Accounting EquationDokument9 SeitenModule 4 - Double Entry Bookkeeping System and The Accounting EquationMark Christian BrlNoch keine Bewertungen

- Module 2 - Double Entry Bookkeeping System and The Accounting EquationDokument9 SeitenModule 2 - Double Entry Bookkeeping System and The Accounting EquationPrincess Joy CabreraNoch keine Bewertungen

- Financial Accounting and ReportingDokument12 SeitenFinancial Accounting and ReportingDiane GarciaNoch keine Bewertungen

- 2 - The Accounting ProcessDokument4 Seiten2 - The Accounting ProcessWea AmorNoch keine Bewertungen

- Accounting For Non Accountants 1Dokument98 SeitenAccounting For Non Accountants 1Sherry Mae Esteleydes100% (1)

- PA 7 Accounting ReportDokument8 SeitenPA 7 Accounting ReportISAACNoch keine Bewertungen

- Review On Basic AccountingDokument19 SeitenReview On Basic AccountingRegina BengadoNoch keine Bewertungen

- Chapter 3 The Accounting Equation The Double Entry SystemDokument7 SeitenChapter 3 The Accounting Equation The Double Entry System2023302256Noch keine Bewertungen

- Basic AccountingDokument2 SeitenBasic Accountingram sagarNoch keine Bewertungen

- Supplementary 1 - Financial StatementsDokument21 SeitenSupplementary 1 - Financial StatementsQuốc Khánh100% (1)

- Accounting Equation - Part 1Dokument11 SeitenAccounting Equation - Part 1Krrish Bosamia100% (1)

- BMCE-770005Dokument6 SeitenBMCE-770005mendutokweNoch keine Bewertungen

- Chapter 02 - Double Entry Bookkeeping Part ADokument42 SeitenChapter 02 - Double Entry Bookkeeping Part AArkar.myanmar 2018Noch keine Bewertungen

- LESSON 7 The Accounting EquationDokument3 SeitenLESSON 7 The Accounting EquationUnamadable UnleomarableNoch keine Bewertungen

- Accounting Lecture 1Dokument3 SeitenAccounting Lecture 1Karl haddadNoch keine Bewertungen

- Module 02 - Financial AccountingDokument11 SeitenModule 02 - Financial AccountingJohn Martin L. AilesNoch keine Bewertungen

- Double Entry System & Accounting Equation: by - Mrs. Dilshad D. JalnawallaDokument34 SeitenDouble Entry System & Accounting Equation: by - Mrs. Dilshad D. JalnawallaTufail GanaieNoch keine Bewertungen

- 5# 4 Accounting Equation (UnSolved) PDFDokument4 Seiten5# 4 Accounting Equation (UnSolved) PDFZaheer SwatiNoch keine Bewertungen

- Potomac Accounting Test - AnswersDokument5 SeitenPotomac Accounting Test - AnswersJason PutotNoch keine Bewertungen

- 5 Major Accounts - Miss JeDokument83 Seiten5 Major Accounts - Miss Jeje-ann montejoNoch keine Bewertungen

- Acc1 Lesson Week10Dokument18 SeitenAcc1 Lesson Week10KeiNoch keine Bewertungen

- Fund W1-3Dokument55 SeitenFund W1-3Edren LoyloyNoch keine Bewertungen

- 3 AccountingDokument39 Seiten3 AccountingSaltanat ShamovaNoch keine Bewertungen

- Bookkeeping - Unit 2Dokument10 SeitenBookkeeping - Unit 2vanzylpetro208Noch keine Bewertungen

- Chapter Two - Fundamentals of AcctDokument14 SeitenChapter Two - Fundamentals of AcctGedionNoch keine Bewertungen

- Analyzing and Recording TransactionsDokument43 SeitenAnalyzing and Recording TransactionsAndrea ValdezNoch keine Bewertungen

- Lesson 3 - AccountsDokument13 SeitenLesson 3 - AccountsJeyem AscueNoch keine Bewertungen

- ACCT1111 Chapter 2 LectureDokument61 SeitenACCT1111 Chapter 2 LectureWky Jim100% (1)

- ACFM CH-THREE 2022-UpdatedDokument130 SeitenACFM CH-THREE 2022-Updatedmihiretche0Noch keine Bewertungen

- BBAW2103 - Tutorial 1Dokument69 SeitenBBAW2103 - Tutorial 1M THREE THOUSAND RESOURCESNoch keine Bewertungen

- Transaction 1: Company A Sold Its Products at $120 and Received The Full Amount in CashDokument24 SeitenTransaction 1: Company A Sold Its Products at $120 and Received The Full Amount in CashPoonam RedkarNoch keine Bewertungen

- Session 3 - PGP2017 - Accounting Mechanics PDFDokument37 SeitenSession 3 - PGP2017 - Accounting Mechanics PDFAjay DesaleNoch keine Bewertungen

- Accounting Equation and Double Entry BookkeepingDokument29 SeitenAccounting Equation and Double Entry BookkeepingArvin ToraldeNoch keine Bewertungen

- Accounting Journal EntriesDokument9 SeitenAccounting Journal EntriesadnanNoch keine Bewertungen

- Chapter - 2 @2003Dokument14 SeitenChapter - 2 @2003Tariku KolchaNoch keine Bewertungen

- Financial Accounting Module 2 SummaryDokument2 SeitenFinancial Accounting Module 2 Summarymohita.gupta4Noch keine Bewertungen

- Account Classification and Presentation: Account Title Classification Financial Statement A Normal BalanceDokument4 SeitenAccount Classification and Presentation: Account Title Classification Financial Statement A Normal BalanceGurusamy KNoch keine Bewertungen

- Teeter-Totter Accounting: Your Visual Guide to Understanding Debits and Credits!Von EverandTeeter-Totter Accounting: Your Visual Guide to Understanding Debits and Credits!Bewertung: 2 von 5 Sternen2/5 (1)

- Consolidated SoFP of TAR Bhd GroupDokument5 SeitenConsolidated SoFP of TAR Bhd GroupKelvin LeongNoch keine Bewertungen

- Chap 003Dokument52 SeitenChap 003Kelvin LeongNoch keine Bewertungen

- Course Plan: Universiti Tunku Abdul Rahman (Utar) Faculty of Accountancy and Management (Fam)Dokument22 SeitenCourse Plan: Universiti Tunku Abdul Rahman (Utar) Faculty of Accountancy and Management (Fam)Kelvin LeongNoch keine Bewertungen

- QuestionnairesDokument7 SeitenQuestionnairesKelvin LeongNoch keine Bewertungen

- Detecting Financial Statement Fraud: Best Known For Committing Accounting FraudDokument11 SeitenDetecting Financial Statement Fraud: Best Known For Committing Accounting FraudKelvin LeongNoch keine Bewertungen

- Old Ib Tutorial AnsDokument6 SeitenOld Ib Tutorial AnsKelvin LeongNoch keine Bewertungen

- Tutorial 3 MFRS8 Q PDFDokument3 SeitenTutorial 3 MFRS8 Q PDFKelvin LeongNoch keine Bewertungen

- Consolidated SoFP of TAR Bhd GroupDokument5 SeitenConsolidated SoFP of TAR Bhd GroupKelvin LeongNoch keine Bewertungen

- Tutorial 3 MFRS8 Q PDFDokument3 SeitenTutorial 3 MFRS8 Q PDFKelvin LeongNoch keine Bewertungen

- T9 Q3 Q4Dokument2 SeitenT9 Q3 Q4Kelvin LeongNoch keine Bewertungen

- Step AcquisitionsDokument7 SeitenStep AcquisitionsKelvin Leong100% (1)

- December 2015 Answer2 PDFDokument12 SeitenDecember 2015 Answer2 PDFKelvin LeongNoch keine Bewertungen

- Consolidated SoFP of TAR Bhd GroupDokument5 SeitenConsolidated SoFP of TAR Bhd GroupKelvin LeongNoch keine Bewertungen

- How To Use Bloomberg 3Dokument1 SeiteHow To Use Bloomberg 3Kelvin LeongNoch keine Bewertungen

- Tutorial QDokument6 SeitenTutorial QKelvin LeongNoch keine Bewertungen

- National Differences in Political EconomyDokument66 SeitenNational Differences in Political EconomyberitahrNoch keine Bewertungen

- F5 2013 Dec QDokument7 SeitenF5 2013 Dec Qkumassa kenyaNoch keine Bewertungen

- B&SDokument7 SeitenB&SKelvin LeongNoch keine Bewertungen

- Ma PyqDokument5 SeitenMa PyqKelvin LeongNoch keine Bewertungen

- FHBM1214 Week 2 SDokument48 SeitenFHBM1214 Week 2 SKelvin LeongNoch keine Bewertungen

- 2.A1-Table of ContentDokument2 Seiten2.A1-Table of ContentKelvin LeongNoch keine Bewertungen

- Break-Even Analysis: Cost-Volume-Profit AnalysisDokument64 SeitenBreak-Even Analysis: Cost-Volume-Profit AnalysisKelvin LeongNoch keine Bewertungen

- FHBM1214 Week 1 SDokument76 SeitenFHBM1214 Week 1 SKelvin LeongNoch keine Bewertungen

- FHBM1214 WK 8 9 Qns - LDokument3 SeitenFHBM1214 WK 8 9 Qns - LKelvin LeongNoch keine Bewertungen

- Math Functions ChapterDokument72 SeitenMath Functions ChapterKelvin LeongNoch keine Bewertungen

- Class Plan FHMM1314 201505Dokument1 SeiteClass Plan FHMM1314 201505Kelvin LeongNoch keine Bewertungen

- FHMM1314 IntroductionDokument16 SeitenFHMM1314 IntroductionKelvin LeongNoch keine Bewertungen

- FHEL 1014 BE Lecture Parts of Speech SCDokument4 SeitenFHEL 1014 BE Lecture Parts of Speech SCKelvin LeongNoch keine Bewertungen

- Lecture 1Dokument2 SeitenLecture 1Kelvin LeongNoch keine Bewertungen

- Coursebook Answers: Answers To Test Yourself QuestionsDokument3 SeitenCoursebook Answers: Answers To Test Yourself QuestionsDonatien Oulaii92% (13)

- PT SejahteraDokument9 SeitenPT Sejahteraxin longNoch keine Bewertungen

- Post Test AK2Dokument51 SeitenPost Test AK2thalita najellaNoch keine Bewertungen

- Learning Objective: - To Identify The Uses of The Two Books of Accounts: Journals and LedgersDokument4 SeitenLearning Objective: - To Identify The Uses of The Two Books of Accounts: Journals and LedgersGladzangel LoricabvNoch keine Bewertungen

- Account Statement: 0212482892 Chennai - MadippakkamDokument2 SeitenAccount Statement: 0212482892 Chennai - MadippakkamAJAYNoch keine Bewertungen

- Day 1 (Basic Accounting) PDFDokument32 SeitenDay 1 (Basic Accounting) PDFJO K ERNoch keine Bewertungen

- Cash BookDokument15 SeitenCash Bookswatee89Noch keine Bewertungen

- KashatoDokument15 SeitenKashatoAmadelle Faith100% (6)

- Multiple Choice - JOCDokument14 SeitenMultiple Choice - JOCMuriel MahanludNoch keine Bewertungen

- Various Forms For BrgysDokument47 SeitenVarious Forms For BrgysLala Laniba100% (1)

- Twelve Cases of AccountingDokument152 SeitenTwelve Cases of AccountingregiscardosoNoch keine Bewertungen

- U4A5 PracExerciseDokument7 SeitenU4A5 PracExerciseDrippy SnowflakeNoch keine Bewertungen

- Managerial Accounting PPDokument42 SeitenManagerial Accounting PPSaurav KumarNoch keine Bewertungen

- 12th STD Auditing EM OptimisedDokument184 Seiten12th STD Auditing EM OptimisedSasikumarNoch keine Bewertungen

- Sap Settlement ConfigurationDokument35 SeitenSap Settlement Configurationfaycel045100% (1)

- Electricity bill breakdownDokument2 SeitenElectricity bill breakdownRakeshKumarSinghNoch keine Bewertungen

- CPT Model Test Paper 1Dokument150 SeitenCPT Model Test Paper 1Tanya Hughes100% (1)

- Long-term Obligations Chapter 8Dokument21 SeitenLong-term Obligations Chapter 8Cathy Gu100% (1)

- Unit Exercises v.1.0.2Dokument24 SeitenUnit Exercises v.1.0.2Piumal PereraNoch keine Bewertungen

- Principles of Accounts KIT - G10 - G12Dokument122 SeitenPrinciples of Accounts KIT - G10 - G12ketiabukasa5Noch keine Bewertungen

- Gr9 EMS P1 (ENG) June 2022 Question PaperDokument7 SeitenGr9 EMS P1 (ENG) June 2022 Question PaperMfanafuthi100% (2)

- Ch06 Cash and ReceivablesDokument62 SeitenCh06 Cash and ReceivablesCerekiNoch keine Bewertungen

- Accounting For Managers 1Dokument43 SeitenAccounting For Managers 1nivedita_h424040% (1)

- RECONCILE BANK & CASH BOOK BALANCESDokument16 SeitenRECONCILE BANK & CASH BOOK BALANCESMichael AsieduNoch keine Bewertungen

- Level 5 Accounting For ManagersDokument7 SeitenLevel 5 Accounting For ManagerspseNoch keine Bewertungen

- Unit 7 Cash and Funds Flow StatementsDokument85 SeitenUnit 7 Cash and Funds Flow StatementsASIFNoch keine Bewertungen

- Ncert Solutions For Class 11 Accountancy Chapter 4 Recording of Transactions 2Dokument69 SeitenNcert Solutions For Class 11 Accountancy Chapter 4 Recording of Transactions 2Prateek TodurNoch keine Bewertungen

- CCA - Q - Oct - NTB - GhaziabadDokument36 SeitenCCA - Q - Oct - NTB - Ghaziabadpave.scgroupNoch keine Bewertungen

- Chapter 5 Incomplete RecordDokument20 SeitenChapter 5 Incomplete RecordNUR ADLIN ZAFIRAH BINTI NORAZLI KTNNoch keine Bewertungen

- Learning Competencies:: ABM - FABM12-Ia-b-1Dokument6 SeitenLearning Competencies:: ABM - FABM12-Ia-b-1Reynavec100% (1)