Das könnte Ihnen auch gefallen

- FM 1 Assignment 1Dokument3 SeitenFM 1 Assignment 1Jelly Ann AndresNoch keine Bewertungen

- PRACTICAL ACCOUNTING 1 Part 2Dokument9 SeitenPRACTICAL ACCOUNTING 1 Part 2Sophia Christina BalagNoch keine Bewertungen

- Computerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionVon EverandComputerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionNoch keine Bewertungen

- Cases (Cabrera)Dokument5 SeitenCases (Cabrera)Queenie100% (1)

- Theories and Problem Solving AKDokument19 SeitenTheories and Problem Solving AKJob CastonesNoch keine Bewertungen

- Practical Accounting 2: Theory & Practice Advance Accounting Partnership - Formation & AdmissionDokument46 SeitenPractical Accounting 2: Theory & Practice Advance Accounting Partnership - Formation & AdmissionKeith Anthony AmorNoch keine Bewertungen

- Mixed PDFDokument8 SeitenMixed PDFChris Tian FlorendoNoch keine Bewertungen

- Lesson 10 Assignment 4Dokument4 SeitenLesson 10 Assignment 4marcied357Noch keine Bewertungen

- This Study Resource Was: SolutionDokument6 SeitenThis Study Resource Was: SolutionChris Jay LatibanNoch keine Bewertungen

- Assignment: Assessment: Module 1: Banking and Other Financial InstitutionsDokument14 SeitenAssignment: Assessment: Module 1: Banking and Other Financial InstitutionsMiredoNoch keine Bewertungen

- Quiz in AE 09 (Current Liabilities)Dokument2 SeitenQuiz in AE 09 (Current Liabilities)Arlene Dacpano0% (1)

- You Have Successfully Unlocked This Question.: University of Cabuyao (Pamantasan NG Cabuyao) Acctg. ACCTG. 123Dokument3 SeitenYou Have Successfully Unlocked This Question.: University of Cabuyao (Pamantasan NG Cabuyao) Acctg. ACCTG. 123chiji chzzzmeowNoch keine Bewertungen

- Afar 02 P'ship Operation QuizDokument4 SeitenAfar 02 P'ship Operation QuizJohn Laurence LoplopNoch keine Bewertungen

- Chapter 7: What Is GAAP?Dokument4 SeitenChapter 7: What Is GAAP?Lysss EpssssNoch keine Bewertungen

- AndrewDokument1 SeiteAndrewCristine Salvacion Pamatian50% (2)

- Chapter-3 Homework CashDokument5 SeitenChapter-3 Homework CashKenneth Christian WilburNoch keine Bewertungen

- Cash and Cash EquivalentDokument50 SeitenCash and Cash EquivalentAurcus JumskieNoch keine Bewertungen

- Week 4 PDF FreeDokument5 SeitenWeek 4 PDF FreeM. Gibran KhalilNoch keine Bewertungen

- Partnership FormationDokument3 SeitenPartnership FormationJules AguilarNoch keine Bewertungen

- Assignment02 PDFDokument2 SeitenAssignment02 PDFAilene MendozaNoch keine Bewertungen

- Final Exam Joint Arrangements - ACTG341 Advanced Financial Accounting and Reporting 1Dokument7 SeitenFinal Exam Joint Arrangements - ACTG341 Advanced Financial Accounting and Reporting 1Marilou Arcillas PanisalesNoch keine Bewertungen

- Chapter 14, Modern Advanced Accounting-Review Q & ExrDokument18 SeitenChapter 14, Modern Advanced Accounting-Review Q & Exrrlg4814100% (4)

- Comprehensive ProblemDokument1 SeiteComprehensive ProblemDavid Con RiveroNoch keine Bewertungen

- MODULE 2 CVP AnalysisDokument8 SeitenMODULE 2 CVP Analysissharielles /Noch keine Bewertungen

- CMPC 131 Finals Quiz 1 Short Term AY 2018 2019 SolutionDokument4 SeitenCMPC 131 Finals Quiz 1 Short Term AY 2018 2019 SolutionAlinah AquinoNoch keine Bewertungen

- HOME OFFICE AND BRANCH ACCOUNTING ExprobDokument9 SeitenHOME OFFICE AND BRANCH ACCOUNTING ExprobJenaz Albert CorralesNoch keine Bewertungen

- Administrative Office ManagementDokument44 SeitenAdministrative Office ManagementLea VenturozoNoch keine Bewertungen

- Home Office and Branch ReviewerDokument1 SeiteHome Office and Branch ReviewerSheena ClataNoch keine Bewertungen

- Partnership Formation QuizDokument5 SeitenPartnership Formation QuizMJ NuarinNoch keine Bewertungen

- AdjustmentDokument5 SeitenAdjustmentBeta TesterNoch keine Bewertungen

- Comp 3Dokument28 SeitenComp 3CristineJoyceMalubayIINoch keine Bewertungen

- Assignment03 PDFDokument2 SeitenAssignment03 PDFAilene MendozaNoch keine Bewertungen

- QUIZ1Dokument4 SeitenQUIZ1alellieNoch keine Bewertungen

- Dhis Special Transactions 2019 by Millan Solman PDFDokument158 SeitenDhis Special Transactions 2019 by Millan Solman PDFQueeny Mae Cantre ReutaNoch keine Bewertungen

- Taxation: Multiple ChoiceDokument16 SeitenTaxation: Multiple ChoiceJomar VillenaNoch keine Bewertungen

- 6902 - Investment Property and Other InvestmentDokument3 Seiten6902 - Investment Property and Other InvestmentAljur SalamedaNoch keine Bewertungen

- 11 Just in Time Backflush CostingDokument3 Seiten11 Just in Time Backflush CostingIrish Gracielle Dela CruzNoch keine Bewertungen

- AE 18 Financial Market Prelim ExamDokument3 SeitenAE 18 Financial Market Prelim ExamWenjunNoch keine Bewertungen

- Acc 310 - M004Dokument12 SeitenAcc 310 - M004Edward Glenn BaguiNoch keine Bewertungen

- Colegio de La Purisima Concepcion: School of The Archdiocese of Capiz Roxas CityDokument5 SeitenColegio de La Purisima Concepcion: School of The Archdiocese of Capiz Roxas CityJhomel Domingo GalvezNoch keine Bewertungen

- 01 CashandCashEquivalentsNotesDokument7 Seiten01 CashandCashEquivalentsNotesVeroNoch keine Bewertungen

- AC 3101 Discussion ProblemDokument1 SeiteAC 3101 Discussion ProblemYohann Leonard HuanNoch keine Bewertungen

- Competency Appraisal UM Digos (PARTNERSHIP)Dokument10 SeitenCompetency Appraisal UM Digos (PARTNERSHIP)Diana Faye CaduadaNoch keine Bewertungen

- 10 Responsibility Accounting Live DiscussionDokument4 Seiten10 Responsibility Accounting Live DiscussionLee SuarezNoch keine Bewertungen

- CVP VAnswer Practice QuestionsDokument5 SeitenCVP VAnswer Practice QuestionsAbhijit AshNoch keine Bewertungen

- Chapter 12-14Dokument18 SeitenChapter 12-14Serena Van Der WoodsenNoch keine Bewertungen

- IA3 Mod 4 REDokument12 SeitenIA3 Mod 4 REjulia4razoNoch keine Bewertungen

- Homework On Statement of Cash FlowsDokument2 SeitenHomework On Statement of Cash FlowsAmy SpencerNoch keine Bewertungen

- Process CostingDokument18 SeitenProcess CostingCheliah Mae ImperialNoch keine Bewertungen

- Receipt and Disposition of InventoriesDokument5 SeitenReceipt and Disposition of InventoriesWawex DavisNoch keine Bewertungen

- IFRS 3 Business CombinationsDokument17 SeitenIFRS 3 Business CombinationsGround ZeroNoch keine Bewertungen

- Consolidated BS - Date of AcquisitionDokument2 SeitenConsolidated BS - Date of AcquisitionKharen Valdez0% (1)

- MASDokument2 SeitenMASClarisse AlimotNoch keine Bewertungen

- Partnership Dissolution 4Dokument6 SeitenPartnership Dissolution 4Karl Wilson GonzalesNoch keine Bewertungen

- Final Preboard May 08Dokument21 SeitenFinal Preboard May 08Ray Allen PabiteroNoch keine Bewertungen

- SATURDAYDokument20 SeitenSATURDAYkristine bandaviaNoch keine Bewertungen

- Abm QuizDokument5 SeitenAbm QuizCastleclash CastleclashNoch keine Bewertungen

- Accountancy Review Center (ARC) of The Philippines Inc.: First Pre-Board ExaminationDokument26 SeitenAccountancy Review Center (ARC) of The Philippines Inc.: First Pre-Board ExaminationCarlo AgravanteNoch keine Bewertungen

- Yummy N TummyDokument27 SeitenYummy N TummyMa Jemaris SolisNoch keine Bewertungen

- Business Ethics Group 4Dokument10 SeitenBusiness Ethics Group 4Ma Jemaris SolisNoch keine Bewertungen

- Business Ethics Row 2Dokument6 SeitenBusiness Ethics Row 2Ma Jemaris SolisNoch keine Bewertungen

- Roles and Functions Group 5Dokument20 SeitenRoles and Functions Group 5Ma Jemaris SolisNoch keine Bewertungen

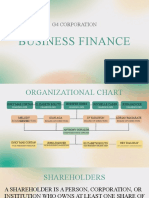

- The Corporate Organization Structure Row 3 Business FinanceDokument19 SeitenThe Corporate Organization Structure Row 3 Business FinanceMa Jemaris SolisNoch keine Bewertungen

- Give The Symbols For Drawing The Genogram or Family Tree.: MelcDokument6 SeitenGive The Symbols For Drawing The Genogram or Family Tree.: MelcMa Jemaris SolisNoch keine Bewertungen

- Health Protocols: School Health Nurse DesignateDokument7 SeitenHealth Protocols: School Health Nurse DesignateMa Jemaris SolisNoch keine Bewertungen

- Quiz - Business EthicsDokument3 SeitenQuiz - Business EthicsMa Jemaris SolisNoch keine Bewertungen

- Quiz - Business FinanceDokument3 SeitenQuiz - Business FinanceMa Jemaris SolisNoch keine Bewertungen

- The Accounting Equation PP TDokument15 SeitenThe Accounting Equation PP TMa Jemaris SolisNoch keine Bewertungen

- Department of Education Region VIII Division of Catbalogan City Catbalogan National Comprehensive High School Mercedes Catbalogan City, SamarDokument5 SeitenDepartment of Education Region VIII Division of Catbalogan City Catbalogan National Comprehensive High School Mercedes Catbalogan City, SamarMa Jemaris SolisNoch keine Bewertungen

- 10 Fun Facts About Accounting InfographicDokument1 Seite10 Fun Facts About Accounting InfographicMa Jemaris SolisNoch keine Bewertungen

- Activity Completion ReportDokument6 SeitenActivity Completion ReportMa Jemaris SolisNoch keine Bewertungen

- Bank of Rajasthan MergerDokument75 SeitenBank of Rajasthan MergerArunKumar100% (1)

- 2018 Integrated Report PDFDokument290 Seiten2018 Integrated Report PDFAndrea PalancaNoch keine Bewertungen

- PSK Assurance NoteDokument20 SeitenPSK Assurance NoteNTurin1435100% (1)

- Income Tax NotesDokument18 SeitenIncome Tax NotesVikash kumarNoch keine Bewertungen

- Assignment 4-WPS OfficeDokument3 SeitenAssignment 4-WPS OfficeChirag SabhayaNoch keine Bewertungen

- Debt Policy at Ust Case SolutionDokument2 SeitenDebt Policy at Ust Case Solutiontamur_ahan50% (2)

- Joint ArrangementDokument5 SeitenJoint ArrangementEzrah Lukes100% (2)

- Applications of Percentages AssignmentDokument5 SeitenApplications of Percentages AssignmentMathKeysNoch keine Bewertungen

- The Wizards of MoneyDokument193 SeitenThe Wizards of MoneyPrometeo HadesNoch keine Bewertungen

- Ledger 3Dokument138 SeitenLedger 3AWNoch keine Bewertungen

- Soalan Presentation FA 3Dokument12 SeitenSoalan Presentation FA 3Vasant SriudomNoch keine Bewertungen

- Essar SteelDokument15 SeitenEssar SteelKhushiyal M. KatreNoch keine Bewertungen

- Solved A Which of These Three Firms If Any Is ADokument1 SeiteSolved A Which of These Three Firms If Any Is AM Bilal SaleemNoch keine Bewertungen

- Graft & Corruption in The GovernmentDokument19 SeitenGraft & Corruption in The GovernmentNi CaNoch keine Bewertungen

- Job Interviewing & Salary NegotiationDokument14 SeitenJob Interviewing & Salary NegotiationRohit Sinha100% (2)

- Accounting Changes and Error Corrections Tutorial (3753)Dokument3 SeitenAccounting Changes and Error Corrections Tutorial (3753)Rawan YasserNoch keine Bewertungen

- Annual Report 12 13Dokument58 SeitenAnnual Report 12 13YASH PorwalNoch keine Bewertungen

- Chapter 5 Macay Holding Inc Group 4Dokument5 SeitenChapter 5 Macay Holding Inc Group 4ivy melgarNoch keine Bewertungen

- Orca Share Media1588817298193Dokument779 SeitenOrca Share Media1588817298193Ryo100% (1)

- Fap CombinedDokument77 SeitenFap CombinedKevin MehtaNoch keine Bewertungen

- 08 Corporate BondsDokument4 Seiten08 Corporate Bondspriandhita asmoro75% (4)

- Corporate+Presentation August 2015 Enercom FINALDokument27 SeitenCorporate+Presentation August 2015 Enercom FINALpco123Noch keine Bewertungen

- LRT Vs City of ManilaDokument4 SeitenLRT Vs City of ManilaKristine NavaltaNoch keine Bewertungen

- Kieso Inter Ch21 IFRS Leases SingaporeDokument89 SeitenKieso Inter Ch21 IFRS Leases Singaporetira MeliniaNoch keine Bewertungen

- Business PlanDokument51 SeitenBusiness PlanKyla Nicole100% (1)

- AR BDKI Versi ARA Lowress PDFDokument606 SeitenAR BDKI Versi ARA Lowress PDFluthfisNoch keine Bewertungen

- Parcor Chap 6 DoneDokument10 SeitenParcor Chap 6 DoneJohn Carlo CastilloNoch keine Bewertungen

- Crafting and Executing StarbucksDokument10 SeitenCrafting and Executing StarbucksBhuvanNoch keine Bewertungen

- Intermediate Accounting Vol 2 4th Edition Lo Solutions ManualDokument6 SeitenIntermediate Accounting Vol 2 4th Edition Lo Solutions Manualconvive.unsadden.hgp2100% (17)

- Gen EwsDokument2 SeitenGen EwsPramod ReddyNoch keine Bewertungen