Das könnte Ihnen auch gefallen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- TQM-obedized Syllabus (Final)Dokument15 SeitenTQM-obedized Syllabus (Final)Daphnie Lei Guzman Pascua-SalvadorNoch keine Bewertungen

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- MIS Handout IDokument22 SeitenMIS Handout IDaphnie Lei Guzman Pascua-SalvadorNoch keine Bewertungen

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- MIS Handout IDokument22 SeitenMIS Handout IDaphnie Lei Guzman Pascua-SalvadorNoch keine Bewertungen

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- 05chapter4 PDFDokument41 Seiten05chapter4 PDFGabriel Achacoso MonNoch keine Bewertungen

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- CH09 PPTDokument49 SeitenCH09 PPTJhemson ELisNoch keine Bewertungen

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

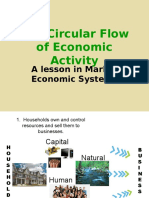

- The Circular Flow of Economic Activity: A Lesson in Market Economic SystemsDokument21 SeitenThe Circular Flow of Economic Activity: A Lesson in Market Economic SystemsDaphnie Lei Guzman Pascua-SalvadorNoch keine Bewertungen

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Example For ElasticDokument6 SeitenExample For ElasticDaphnie Lei Guzman Pascua-Salvador50% (14)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Attitudes, Values, and EthicsDokument20 SeitenAttitudes, Values, and EthicsAnchal JainNoch keine Bewertungen

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- Chap 1Dokument21 SeitenChap 1Hue NguyenNoch keine Bewertungen

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- CVSRTA-Land and Building PDFDokument1.975 SeitenCVSRTA-Land and Building PDFSureshNoch keine Bewertungen

- Question Paper Delhi University 2021Dokument15 SeitenQuestion Paper Delhi University 2021Siddhant MathurNoch keine Bewertungen

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- Elements of Demand and SupplyDokument15 SeitenElements of Demand and SupplyDolly Lyn ReyesNoch keine Bewertungen

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- Advanced Microeconomics Analysis Worked Solutions Jehle RenyDokument7 SeitenAdvanced Microeconomics Analysis Worked Solutions Jehle RenyJuan Solorzano67% (3)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- Class XI QPDokument100 SeitenClass XI QPDevansh DwivediNoch keine Bewertungen

- Mac - Tut 5 Saving and InvenstmentDokument4 SeitenMac - Tut 5 Saving and InvenstmentHiền NguyễnNoch keine Bewertungen

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- Chapter Two: Demand and SupplyDokument71 SeitenChapter Two: Demand and Supplykasech mogesNoch keine Bewertungen

- Demand, Supply, and Market Equilibrium: Anamitra RoyDokument40 SeitenDemand, Supply, and Market Equilibrium: Anamitra RoyGirmsh Yeshewaw GsNoch keine Bewertungen

- Basic Economics MCQs With AnswersDokument32 SeitenBasic Economics MCQs With AnswersNasir Nadeem73% (30)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- Demski 2004Dokument22 SeitenDemski 2004rajeshriskNoch keine Bewertungen

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- Non Linear DynamicsDokument309 SeitenNon Linear DynamicsZomishah Kakakhail100% (4)

- Principles of MacroeconomicsDokument52 SeitenPrinciples of Macroeconomicsmoaz21100% (1)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- OLIGOPOLY and GAME THEORYDokument14 SeitenOLIGOPOLY and GAME THEORYMae TracenaNoch keine Bewertungen

- Tutorial 11 Suggested SolutionsDokument6 SeitenTutorial 11 Suggested SolutionsChloe GuilaNoch keine Bewertungen

- Business Environment MCQsDokument17 SeitenBusiness Environment MCQsDrs InresearchNoch keine Bewertungen

- University of Liberal Arts Bangladesh (ULAB)Dokument13 SeitenUniversity of Liberal Arts Bangladesh (ULAB)HasanZakariaNoch keine Bewertungen

- Engineering EconomicsDokument60 SeitenEngineering EconomicsAbhineet GuptaNoch keine Bewertungen

- Padhle 11th - 8 - Producer's Equilibrium - Microeconomics - EconomicsDokument5 SeitenPadhle 11th - 8 - Producer's Equilibrium - Microeconomics - EconomicsRushil ThindNoch keine Bewertungen

- DocxDokument16 SeitenDocxaksNoch keine Bewertungen

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- Economics Sample Papers IIIDokument5 SeitenEconomics Sample Papers IIIMaithri MurthyNoch keine Bewertungen

- Business Economics Chapter 4 - Consumer Demand AnalysisDokument41 SeitenBusiness Economics Chapter 4 - Consumer Demand Analysispriyanka mudhliyarNoch keine Bewertungen

- Term Paper Supply and DemandDokument8 SeitenTerm Paper Supply and DemandHelpWithAPaperCanada100% (1)

- Chapter 18Dokument43 SeitenChapter 18yexin003Noch keine Bewertungen

- Applied Economics: First Quarter Learning Activity SheetDokument31 SeitenApplied Economics: First Quarter Learning Activity SheetAlvin GadutNoch keine Bewertungen

- J. S. Mill and Reciprocal Demand: Principles of Political EconomyDokument16 SeitenJ. S. Mill and Reciprocal Demand: Principles of Political EconomyAndreas S. KurniawanNoch keine Bewertungen

- ECON MidtermDokument71 SeitenECON MidtermNam AnhNoch keine Bewertungen

- IB Economics Essay Questions P1 2005-2016Dokument15 SeitenIB Economics Essay Questions P1 2005-2016Sidhartha Pahwa50% (2)

- Managerial Economics 3rd Edition Froeb McCann Ward Shor Test BankDokument6 SeitenManagerial Economics 3rd Edition Froeb McCann Ward Shor Test Bankcasey100% (16)

- Assignment UnitVI ManagerialEconomicsDokument13 SeitenAssignment UnitVI ManagerialEconomicsDuncanNoch keine Bewertungen

- Project On Domestic Aviation MPRDokument16 SeitenProject On Domestic Aviation MPRDivya GourNoch keine Bewertungen

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)