Das könnte Ihnen auch gefallen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5795)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1091)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- ICRC - Global Vsat Forum (GVF)Dokument30 SeitenICRC - Global Vsat Forum (GVF)Mahmoud RoshdyNoch keine Bewertungen

- Accounting UC3M Midterm Mock ExamDokument5 SeitenAccounting UC3M Midterm Mock ExamInterecoNoch keine Bewertungen

- Dispute Letter TemplateDokument1 SeiteDispute Letter TemplatePerla Villacan ArguillaNoch keine Bewertungen

- Work Plan - Lisa Rizka AmeliaDokument2 SeitenWork Plan - Lisa Rizka AmeliaLisa Rizka AmeliaNoch keine Bewertungen

- Pledge Point 1 - Small Group ActivityDokument3 SeitenPledge Point 1 - Small Group ActivityLisa Rizka AmeliaNoch keine Bewertungen

- Project Idea For Combating Climate Change Budget Template Project Name: Your Name: Project Duration: Project Location: Line Item Estimated CostDokument2 SeitenProject Idea For Combating Climate Change Budget Template Project Name: Your Name: Project Duration: Project Location: Line Item Estimated CostLisa Rizka AmeliaNoch keine Bewertungen

- Catatan TransportDokument8 SeitenCatatan TransportLisa Rizka AmeliaNoch keine Bewertungen

- Pembahasan Contoh Soal Kompre Struktur: Catatan: Jika Ada Kesalahan Mohon DikoreksiDokument12 SeitenPembahasan Contoh Soal Kompre Struktur: Catatan: Jika Ada Kesalahan Mohon DikoreksiLisa Rizka AmeliaNoch keine Bewertungen

- Catatan RSADokument7 SeitenCatatan RSALisa Rizka AmeliaNoch keine Bewertungen

- Bai Tap Tieng Anh 7 I Learn Smart World Unit 7Dokument3 SeitenBai Tap Tieng Anh 7 I Learn Smart World Unit 7namthuong2010Noch keine Bewertungen

- Cost Acc Chapter 7Dokument14 SeitenCost Acc Chapter 7ElleNoch keine Bewertungen

- SOA Acct 2738103 32023Dokument2 SeitenSOA Acct 2738103 32023L&L TransportNoch keine Bewertungen

- Chapter 3 Testbank Topic Grid: Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition 3-1Dokument6 SeitenChapter 3 Testbank Topic Grid: Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition 3-1Beatrice TehNoch keine Bewertungen

- Audit Responsibilities and ObjectivesDokument43 SeitenAudit Responsibilities and ObjectivesToufiq AgungNoch keine Bewertungen

- Audit Report.: 2021/10 T-Mobile's Data Performance in 4 Markets, USDokument19 SeitenAudit Report.: 2021/10 T-Mobile's Data Performance in 4 Markets, USrazafarhanNoch keine Bewertungen

- SAP Retail Overview Material PurchasingDokument75 SeitenSAP Retail Overview Material PurchasingSUBHOJIT BANERJEENoch keine Bewertungen

- 2 Wal Mart Supply ChainDokument41 Seiten2 Wal Mart Supply Chainanam_shoaib9036100% (1)

- GSRTC Undva Mandli BorderDokument1 SeiteGSRTC Undva Mandli BorderNIRMAL PATELNoch keine Bewertungen

- Shopclues HistoryDokument3 SeitenShopclues HistoryRahul VeldhanaNoch keine Bewertungen

- Exhibit A Generic - Bank Readiness Notification (UBS To La Caixa) 7-3-13Dokument2 SeitenExhibit A Generic - Bank Readiness Notification (UBS To La Caixa) 7-3-13lion100_saadNoch keine Bewertungen

- MA5600T&MA5603T&MA5608T V800R017C10 Product DescriptionDokument68 SeitenMA5600T&MA5603T&MA5608T V800R017C10 Product Descriptionmuayyad_jumahNoch keine Bewertungen

- Assignment: Connectivity Wireless RevolutionDokument4 SeitenAssignment: Connectivity Wireless RevolutionT BabëNoch keine Bewertungen

- Kuwait LeadsDokument2 SeitenKuwait LeadsLahari Chidu TanishkhaNoch keine Bewertungen

- Postpaid TN CDokument67 SeitenPostpaid TN CHimanshu MahorNoch keine Bewertungen

- POM104C Ex2Dokument2 SeitenPOM104C Ex2Rowelle Princess Guilas0% (1)

- Coretrax, P.O Box 7639, Dammam 34325, Kingdom of Saudi Arabia Phone +966 13 833 0919Dokument1 SeiteCoretrax, P.O Box 7639, Dammam 34325, Kingdom of Saudi Arabia Phone +966 13 833 0919Tahir Iqbal. Kharpa RehanNoch keine Bewertungen

- Receivables ProblemsDokument43 SeitenReceivables ProblemsxagocipNoch keine Bewertungen

- ListDokument6 SeitenListTicketmaster customer serviceNoch keine Bewertungen

- Invoice NF29188202112850Dokument3 SeitenInvoice NF29188202112850Prem KumarNoch keine Bewertungen

- IC Cash Receipt TemplateDokument1 SeiteIC Cash Receipt TemplateGentiNoch keine Bewertungen

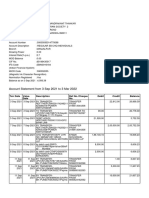

- Account Statement From 3 Sep 2021 To 3 Mar 2022: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDokument8 SeitenAccount Statement From 3 Sep 2021 To 3 Mar 2022: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceViral ThakkarNoch keine Bewertungen

- Morgan Rizvi PDFDokument1 SeiteMorgan Rizvi PDFSuttonFakesNoch keine Bewertungen

- Career Test Result: Personality Types and Holland CodesDokument4 SeitenCareer Test Result: Personality Types and Holland Codesapi-307132793Noch keine Bewertungen

- Eland Cables Invoice 00001159452Dokument2 SeitenEland Cables Invoice 00001159452yousuf dokamNoch keine Bewertungen

- 18 46 PDFDokument7 Seiten18 46 PDFHimanshu PatelNoch keine Bewertungen

- Soacp: Fundamental SOA, Services & MicroservicesDokument2 SeitenSoacp: Fundamental SOA, Services & MicroservicesmlotfyNoch keine Bewertungen