Das könnte Ihnen auch gefallen

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (345)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Credit FINALS ReviewerDokument37 SeitenCredit FINALS ReviewerLynielle CrisologoNoch keine Bewertungen

- Personal Financial ManagementDokument42 SeitenPersonal Financial ManagementBleoobi Isaac A Bonney100% (1)

- Sula Vineyards Case StudyDokument3 SeitenSula Vineyards Case StudyPRIYA KUMARI33% (3)

- Real Estate Mortgage - 2 Title - CorporationDokument2 SeitenReal Estate Mortgage - 2 Title - CorporationgeorenceNoch keine Bewertungen

- AMG, Inc. & Forsythe Solutions - Lease vs. Buy DecisionsDokument8 SeitenAMG, Inc. & Forsythe Solutions - Lease vs. Buy DecisionsPRIYA KUMARINoch keine Bewertungen

- Kinetic Engineering CompanyDokument13 SeitenKinetic Engineering CompanyPRIYA KUMARINoch keine Bewertungen

- Sales and Distribution ManagementDokument6 SeitenSales and Distribution ManagementPRIYA KUMARINoch keine Bewertungen

- Dealership Evaluation SystemsDokument31 SeitenDealership Evaluation SystemsPRIYA KUMARINoch keine Bewertungen

- Oreo 1Dokument16 SeitenOreo 1PRIYA KUMARI100% (1)

- OREODokument15 SeitenOREOPRIYA KUMARINoch keine Bewertungen

- Valuation of EquityDokument40 SeitenValuation of EquityPRIYA KUMARINoch keine Bewertungen

- Hard Rock Cafe - Case StudyDokument4 SeitenHard Rock Cafe - Case StudyPRIYA KUMARI100% (3)

- Session 1&2: by Suman Kumar Deb B.Sc. (H) Maths, M.Sc. Stats, PGDM-Marketing, Six Sigma Black Belt CertifiedDokument21 SeitenSession 1&2: by Suman Kumar Deb B.Sc. (H) Maths, M.Sc. Stats, PGDM-Marketing, Six Sigma Black Belt CertifiedPRIYA KUMARINoch keine Bewertungen

- JKBS Broadcast #2Dokument3 SeitenJKBS Broadcast #2PRIYA KUMARINoch keine Bewertungen

- Consumer Markets and Consumer Buyer BehaviorDokument37 SeitenConsumer Markets and Consumer Buyer BehaviorPRIYA KUMARINoch keine Bewertungen

- Group No.7: Increasing Growth of Maruti-Suzuki in Rural AreaDokument10 SeitenGroup No.7: Increasing Growth of Maruti-Suzuki in Rural AreaPRIYA KUMARINoch keine Bewertungen

- Unit-3 New-Product DevelopmentDokument19 SeitenUnit-3 New-Product DevelopmentPRIYA KUMARINoch keine Bewertungen

- IDFCSHRIRAMMERGERDokument8 SeitenIDFCSHRIRAMMERGERMee MeeNoch keine Bewertungen

- Philippine Supreme Court Jurisprudence: Home Law Firm Law Library Laws Jurisprudence Contact UsDokument6 SeitenPhilippine Supreme Court Jurisprudence: Home Law Firm Law Library Laws Jurisprudence Contact Usinternation businesstradeNoch keine Bewertungen

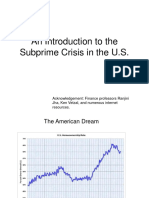

- An Introduction To The Subprime Crisis in The U.SDokument25 SeitenAn Introduction To The Subprime Crisis in The U.SAdeel RanaNoch keine Bewertungen

- Wise Transaction Invoice Transfer 720336148 1271654884 PTDokument2 SeitenWise Transaction Invoice Transfer 720336148 1271654884 PTruizitoxNoch keine Bewertungen

- TermsDokument1 SeiteTermsedNoch keine Bewertungen

- Challan KUGET1ZK152E257900 22082023 132815Dokument1 SeiteChallan KUGET1ZK152E257900 22082023 132815Serial story Kannada Serial story KannadaNoch keine Bewertungen

- Sales Brochure 91Dokument3 SeitenSales Brochure 91prudhvi rajNoch keine Bewertungen

- Real Estate MortgageDokument2 SeitenReal Estate MortgageDundee M. OzoaNoch keine Bewertungen

- I888 Food Catering Payslip & AttendanceDokument5 SeitenI888 Food Catering Payslip & AttendanceMark LopezNoch keine Bewertungen

- 2019 TSP Catch-Up Contributions and Effective Date ChartDokument1 Seite2019 TSP Catch-Up Contributions and Effective Date ChartRayNoch keine Bewertungen

- Unit 2 - Module 2Dokument18 SeitenUnit 2 - Module 2Sujata SarkarNoch keine Bewertungen

- HDFC Life InsuranceDokument12 SeitenHDFC Life Insurancesaswat mohantyNoch keine Bewertungen

- Current Account - 19140200000546 Cenozoic Remedies PVT LTDDokument2 SeitenCurrent Account - 19140200000546 Cenozoic Remedies PVT LTDvinamratiwari7278Noch keine Bewertungen

- FOR ASSIGNMENT. Bank Reco.Dokument1 SeiteFOR ASSIGNMENT. Bank Reco.Shekainah BNoch keine Bewertungen

- MONEY AND CREDIT Day 13 2024asdfghjkDokument2 SeitenMONEY AND CREDIT Day 13 2024asdfghjkfivestar12042015Noch keine Bewertungen

- The Orange Book Vol 11 PDFDokument13 SeitenThe Orange Book Vol 11 PDFShreshtha SinghNoch keine Bewertungen

- Chapter 2 - Time Value of Money and Its ApplicationDokument69 SeitenChapter 2 - Time Value of Money and Its ApplicationQUYÊN VŨ THỊ THUNoch keine Bewertungen

- Home Equity Loan CalculatorDokument18 SeitenHome Equity Loan Calculatorvijay sainiNoch keine Bewertungen

- Statement of AccountDokument34 SeitenStatement of AccountMVN HodalNoch keine Bewertungen

- Chapter 1 - QuizDokument4 SeitenChapter 1 - QuizCk WilliumNoch keine Bewertungen

- Ifr PRC Banks in Loan Trading Plea Sept19Dokument3 SeitenIfr PRC Banks in Loan Trading Plea Sept19tracy.jiang0908Noch keine Bewertungen

- SkyfiberDokument2 SeitenSkyfiberdanocuments.editNoch keine Bewertungen

- TataDokument8 SeitenTataSherry SahaNoch keine Bewertungen

- Accounting For BondsDokument11 SeitenAccounting For BondsChrisus Joseph SarchezNoch keine Bewertungen

- WSP Levered DCF Model VFDokument5 SeitenWSP Levered DCF Model VFBlahNoch keine Bewertungen

- Principles of Money and Time RelationshipsDokument1 SeitePrinciples of Money and Time RelationshipsChris Alunan67% (3)

- StatementOfAccount 50456096257 16082023 141039Dokument186 SeitenStatementOfAccount 50456096257 16082023 141039Praveen SainiNoch keine Bewertungen