Das könnte Ihnen auch gefallen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (890)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (587)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (119)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2219)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (265)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- Memo - Submission of Required ReportsDokument1 SeiteMemo - Submission of Required Reportsopep7763% (8)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (73)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- MCQs On Transfer of Property ActDokument46 SeitenMCQs On Transfer of Property ActRam Iyer75% (4)

- FPO Application GuideDokument33 SeitenFPO Application GuideIsrael Miranda Zamarca100% (1)

- Algebra, Equations and FormulaeDokument29 SeitenAlgebra, Equations and FormulaeDr Kishor BhanushaliNoch keine Bewertungen

- ECO2201 MacroeconomicsDokument7 SeitenECO2201 MacroeconomicsDr Kishor Bhanushali0% (1)

- SecuritizationDokument12 SeitenSecuritizationDr Kishor Bhanushali100% (1)

- Strategic Leadership (Partha S Ghosh)Dokument4 SeitenStrategic Leadership (Partha S Ghosh)Dr Kishor Bhanushali100% (1)

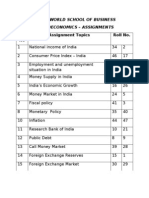

- Unitedworld School of Business Macroeconomics - Assignments Sr. No 1Dokument2 SeitenUnitedworld School of Business Macroeconomics - Assignments Sr. No 1Dr Kishor BhanushaliNoch keine Bewertungen

- GDP DataDokument6 SeitenGDP DataDr Kishor BhanushaliNoch keine Bewertungen

- Cloth RecycleDokument4 SeitenCloth RecycleMuhammad Ammar KhanNoch keine Bewertungen

- FWN Magazine 2017 - Hon. Cynthia BarkerDokument44 SeitenFWN Magazine 2017 - Hon. Cynthia BarkerFilipina Women's NetworkNoch keine Bewertungen

- Oil Industry of Kazakhstan: Name: LIU XU Class: Tuesday ID No.: 014201900253Dokument2 SeitenOil Industry of Kazakhstan: Name: LIU XU Class: Tuesday ID No.: 014201900253cey liuNoch keine Bewertungen

- The Millennium Development Goals Report: United NationsDokument21 SeitenThe Millennium Development Goals Report: United Nationshst939Noch keine Bewertungen

- IIP - Vs - PMI, DifferencesDokument5 SeitenIIP - Vs - PMI, DifferencesChetan GuptaNoch keine Bewertungen

- Licensed Contractor Report - June 2015 PDFDokument20 SeitenLicensed Contractor Report - June 2015 PDFSmith GrameNoch keine Bewertungen

- Final Report For Print and CDDokument170 SeitenFinal Report For Print and CDmohit_ranjan2008Noch keine Bewertungen

- Faith in Wooden Toys: A Glimpse into Selecta SpielzeugDokument2 SeitenFaith in Wooden Toys: A Glimpse into Selecta SpielzeugAvishekNoch keine Bewertungen

- AUH DataDokument702 SeitenAUH DataParag Babar33% (3)

- Print - Udyam Registration Certificate AnnexureDokument2 SeitenPrint - Udyam Registration Certificate AnnexureTrupti GhadiNoch keine Bewertungen

- Regenerative Braking SystemDokument27 SeitenRegenerative Braking SystemNavaneethakrishnan RangaswamyNoch keine Bewertungen

- Extra Oligopolio PDFDokument17 SeitenExtra Oligopolio PDFkako_1984Noch keine Bewertungen

- General Terms and ConditionsDokument8 SeitenGeneral Terms and ConditionsSudhanshu JainNoch keine Bewertungen

- Industrial Visit ReportDokument6 SeitenIndustrial Visit ReportgaureshraoNoch keine Bewertungen

- Germany Vs Singapore by Andrew BaeyDokument12 SeitenGermany Vs Singapore by Andrew Baeyacs1234100% (2)

- A4 - Productivity - City Plan 2036 Draft City of Sydney Local Strategic Planning StatementDokument31 SeitenA4 - Productivity - City Plan 2036 Draft City of Sydney Local Strategic Planning StatementDorjeNoch keine Bewertungen

- Lic Plans at A GlanceDokument3 SeitenLic Plans at A GlanceTarun GoyalNoch keine Bewertungen

- "Tsogttetsii Soum Solid Waste Management Plan" Environ LLCDokument49 Seiten"Tsogttetsii Soum Solid Waste Management Plan" Environ LLCbatmunkh.eNoch keine Bewertungen

- E734415 40051 2nd Announcement International Seminar Bridge Inspection and Rehabilitation Techniques Tunis February 2023Dokument9 SeitenE734415 40051 2nd Announcement International Seminar Bridge Inspection and Rehabilitation Techniques Tunis February 2023jihad1568Noch keine Bewertungen

- PDACN634Dokument69 SeitenPDACN634sualihu22121100% (1)

- Kobra 260.1 S4Dokument1 SeiteKobra 260.1 S4Mishmash PurchasingNoch keine Bewertungen

- Bid Data SheetDokument3 SeitenBid Data SheetEdwin Cob GuriNoch keine Bewertungen

- Steel-A-thon Strategy & Supply Chain CaseletsDokument8 SeitenSteel-A-thon Strategy & Supply Chain CaseletsAnkit SahuNoch keine Bewertungen

- Principle of Economics1 (Chapter2)Dokument7 SeitenPrinciple of Economics1 (Chapter2)MA ValdezNoch keine Bewertungen

- Safari - Nov 2, 2017 at 4:13 PM PDFDokument1 SeiteSafari - Nov 2, 2017 at 4:13 PM PDFAmy HernandezNoch keine Bewertungen

- Aec 2101 Production Economics - 0Dokument4 SeitenAec 2101 Production Economics - 0Kelvin MagiriNoch keine Bewertungen

- Industrial Sector in BDDokument30 SeitenIndustrial Sector in BDImtiaz AhmedNoch keine Bewertungen