Das könnte Ihnen auch gefallen

- Lease AccountingDokument52 SeitenLease Accountinglei veraNoch keine Bewertungen

- Operating Lease Accounting for LessorsDokument4 SeitenOperating Lease Accounting for LessorsikiNoch keine Bewertungen

- Sales Type Lease Journal EntriesDokument15 SeitenSales Type Lease Journal Entrieseulhiemae arong0% (1)

- Lease Modules ContinuedDokument8 SeitenLease Modules ContinuedKenneth Marcial Ege0% (1)

- Chapter 15 and 16 IA Valix Sales Type LeaseDokument13 SeitenChapter 15 and 16 IA Valix Sales Type LeaseMiko ArniñoNoch keine Bewertungen

- MODULE Midterm FAR 3 LeasesDokument36 SeitenMODULE Midterm FAR 3 LeasesKrizza Jane PayumoNoch keine Bewertungen

- Activity 3-4 SB CompensationDokument3 SeitenActivity 3-4 SB CompensationNhel Alvaro0% (1)

- Group-1-Chap-4 & 5Dokument10 SeitenGroup-1-Chap-4 & 5Cherie Soriano AnanayoNoch keine Bewertungen

- Sale and LeasebackDokument10 SeitenSale and LeasebackShinny Jewel VingnoNoch keine Bewertungen

- Learning Resource 12: Accounting For Employee BenefitsDokument6 SeitenLearning Resource 12: Accounting For Employee BenefitsRemedios Capistrano CatacutanNoch keine Bewertungen

- CSC 201-Leones, Mary Grace O. - IntermediateDokument28 SeitenCSC 201-Leones, Mary Grace O. - IntermediateMary Grace Ocampo LeonesNoch keine Bewertungen

- Lease Problem With SolutionDokument19 SeitenLease Problem With SolutionJeane Mae Boo100% (1)

- Leases Part 3 - Other Accounting IssuesDokument33 SeitenLeases Part 3 - Other Accounting IssuesDanica RamosNoch keine Bewertungen

- Quiz 2-Current LiabilitiesDokument6 SeitenQuiz 2-Current LiabilitiesJam SurdivillaNoch keine Bewertungen

- FdsedjwhajdhkudshdhxDokument28 SeitenFdsedjwhajdhkudshdhxJoylyn CombongNoch keine Bewertungen

- Chapter 13 Ia2Dokument18 SeitenChapter 13 Ia2JM Valonda Villena, CPA, MBANoch keine Bewertungen

- Cabug-Os, Lovely A. (Assignment 9)Dokument2 SeitenCabug-Os, Lovely A. (Assignment 9)Joylyn CombongNoch keine Bewertungen

- Valix 2 Chapt 24 25 PDFDokument20 SeitenValix 2 Chapt 24 25 PDFivyaguasarnaldo4everNoch keine Bewertungen

- Learning Resource 9: Lessor Accounting: Lesson 1: Operating LeaseDokument6 SeitenLearning Resource 9: Lessor Accounting: Lesson 1: Operating LeaseRemedios Capistrano Catacutan0% (1)

- Accounting 132Dokument2 SeitenAccounting 132Anne Marieline BuenaventuraNoch keine Bewertungen

- St. Paul University PhilippinesDokument4 SeitenSt. Paul University PhilippinesGarp BarrocaNoch keine Bewertungen

- Bond Issuance and AmortizationDokument1 SeiteBond Issuance and AmortizationRhitzelynn Ann BarredoNoch keine Bewertungen

- c2 Premium Liability Lets Get It PDFDokument15 Seitenc2 Premium Liability Lets Get It PDFCris VillarNoch keine Bewertungen

- Chapter 15 Ia2Dokument21 SeitenChapter 15 Ia2JM Valonda Villena, CPA, MBANoch keine Bewertungen

- Problems Problem 9-1 (ACP)Dokument11 SeitenProblems Problem 9-1 (ACP)Emey Calbay33% (3)

- Quiz 2 Compound Financial Instruments Notes PayableDokument17 SeitenQuiz 2 Compound Financial Instruments Notes PayableRey Clarence BanggayanNoch keine Bewertungen

- Postemployment Benefits: Employee's Employee Employee Obligation DecemberDokument25 SeitenPostemployment Benefits: Employee's Employee Employee Obligation DecemberGabriel PanganNoch keine Bewertungen

- Marine Engineering Problems Chapter 11 & 12Dokument24 SeitenMarine Engineering Problems Chapter 11 & 12Sean AustinNoch keine Bewertungen

- Finance LeaseDokument26 SeitenFinance LeaseJudith GabuteroNoch keine Bewertungen

- Chapter 15,16, & 17 IA Valix Sales Type LeaseDokument15 SeitenChapter 15,16, & 17 IA Valix Sales Type LeaseMiko ArniñoNoch keine Bewertungen

- Employee Benefits ChapterDokument11 SeitenEmployee Benefits ChapterJM Valonda Villena, CPA, MBANoch keine Bewertungen

- Bonds PayableDokument5 SeitenBonds PayableSky SoronoiNoch keine Bewertungen

- Financial Assets at Fair Value Problem with ChangesDokument106 SeitenFinancial Assets at Fair Value Problem with Changesmore100% (1)

- Practical Accounting 1 - Review Leases 2019Dokument15 SeitenPractical Accounting 1 - Review Leases 2019Gabrielle100% (1)

- Warranty Liability Lesson on Accrual and Expense RecognitionDokument15 SeitenWarranty Liability Lesson on Accrual and Expense RecognitionCirelle Faye Silva0% (1)

- ACC 211 SIM Week 6 7Dokument40 SeitenACC 211 SIM Week 6 7Threcia Rota50% (2)

- Debt Restructuring - Prof PDFDokument6 SeitenDebt Restructuring - Prof PDFDonise Ronadel Santos50% (2)

- Finals Questionnaire A31 PDFDokument8 SeitenFinals Questionnaire A31 PDFAnne Marieline BuenaventuraNoch keine Bewertungen

- 62230126Dokument20 Seiten62230126ROMULO CUBIDNoch keine Bewertungen

- Practice and exercises for Unit 2Dokument3 SeitenPractice and exercises for Unit 2Daniella Mae ElipNoch keine Bewertungen

- This Study Resource Was Shared Via: de La Salle LipaDokument2 SeitenThis Study Resource Was Shared Via: de La Salle LipaAngel ObligacionNoch keine Bewertungen

- Hotcake Mix Premium Expense and Liability CalculationDokument4 SeitenHotcake Mix Premium Expense and Liability CalculationChristian N MagsinoNoch keine Bewertungen

- Recording equity swap and debt restructuring entriesDokument7 SeitenRecording equity swap and debt restructuring entriesJam SurdivillaNoch keine Bewertungen

- Bonds Payable 1Dokument2 SeitenBonds Payable 1els emsNoch keine Bewertungen

- Estimating warranty liabilityDokument12 SeitenEstimating warranty liabilityRiza Kristine DaytoNoch keine Bewertungen

- Contingent Liability LessonDokument14 SeitenContingent Liability LessonJerald Jay Capistrano Catacutan100% (1)

- Examination About Investment 13Dokument2 SeitenExamination About Investment 13BLACKPINKLisaRoseJisooJennieNoch keine Bewertungen

- Midterm Review QuestionsDokument19 SeitenMidterm Review Questionschiji chzzzmeowNoch keine Bewertungen

- Project in Fin Acc Chester Gutierrez Project in Fin Acc Chester GutierrezDokument17 SeitenProject in Fin Acc Chester Gutierrez Project in Fin Acc Chester GutierrezJoseph Asis50% (2)

- Lease - Lessee's Perspective: Lecture NotesDokument9 SeitenLease - Lessee's Perspective: Lecture NotesDonise Ronadel SantosNoch keine Bewertungen

- San Beda College Alabang Homework Exercise-Act851RDokument4 SeitenSan Beda College Alabang Homework Exercise-Act851RJomel BaptistaNoch keine Bewertungen

- Premium Liability AccountingDokument2 SeitenPremium Liability AccountingAngelica MadsonNoch keine Bewertungen

- CSTC College of Sciences Technology and Communication, IncDokument35 SeitenCSTC College of Sciences Technology and Communication, IncJohn Patrick MercurioNoch keine Bewertungen

- Quiz 1-Current LiabDokument11 SeitenQuiz 1-Current LiabBadAssNoch keine Bewertungen

- Module 5 - Ia2 Final CBLDokument13 SeitenModule 5 - Ia2 Final CBLErik Lorenz Palomares0% (1)

- Activity 1 Employee Benefits AKDokument7 SeitenActivity 1 Employee Benefits AKRalph Rivera SantosNoch keine Bewertungen

- Assignment 7 On Chapt 3 Problem 3 17 On Page 93Dokument2 SeitenAssignment 7 On Chapt 3 Problem 3 17 On Page 93Joylyn CombongNoch keine Bewertungen

- Intacc Finals Sw&QuizzesDokument57 SeitenIntacc Finals Sw&QuizzesIris FenelleNoch keine Bewertungen

- Leasing As A Form of DebtDokument24 SeitenLeasing As A Form of DebtSheila Mae Guerta LaceronaNoch keine Bewertungen

- Accounting For LeasesDokument12 SeitenAccounting For LeasesvladsteinarminNoch keine Bewertungen

- Your Birthstone: Its Meaning, Significance and Healing PropertiesDokument8 SeitenYour Birthstone: Its Meaning, Significance and Healing PropertiesJudyNoch keine Bewertungen

- A MartyrDokument1 SeiteA MartyrJudyNoch keine Bewertungen

- Findings and RecommendationsDokument3 SeitenFindings and RecommendationsJudyNoch keine Bewertungen

- Accounts Receivable ProblemsDokument12 SeitenAccounts Receivable ProblemsJudyNoch keine Bewertungen

- AnswerDokument11 SeitenAnswerJudyNoch keine Bewertungen

- What Is MortgageDokument4 SeitenWhat Is MortgageJudyNoch keine Bewertungen

- BG CompanyDokument1 SeiteBG CompanyJudyNoch keine Bewertungen

- RulesDokument3 SeitenRulesJudyNoch keine Bewertungen

- HumanitiesDokument3 SeitenHumanitiesJudyNoch keine Bewertungen

- What Is MortgageDokument4 SeitenWhat Is MortgageJudyNoch keine Bewertungen

- MAS1Dokument2 SeitenMAS1JudyNoch keine Bewertungen

- BackgroundDokument7 SeitenBackgroundJudyNoch keine Bewertungen

- MAS1Dokument2 SeitenMAS1JudyNoch keine Bewertungen

- Audit Evidence and DocumentationDokument4 SeitenAudit Evidence and DocumentationJudy100% (1)

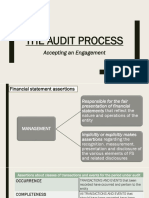

- The Audit ProcessDokument24 SeitenThe Audit ProcessJudyNoch keine Bewertungen

- AnswerDokument11 SeitenAnswerJudyNoch keine Bewertungen

- DepletionDokument7 SeitenDepletionJudyNoch keine Bewertungen

- The Audit ProcessDokument24 SeitenThe Audit ProcessJudyNoch keine Bewertungen

- Financial Accounting ReportDokument9 SeitenFinancial Accounting ReportJudyNoch keine Bewertungen

- The Audit ProcessDokument24 SeitenThe Audit ProcessJudyNoch keine Bewertungen

- Ed Sheeran LyricsDokument2 SeitenEd Sheeran LyricsJudyNoch keine Bewertungen

- Chapter 11 Answers RepportDokument12 SeitenChapter 11 Answers RepportJudy56% (16)

- Related Literature and StudiesDokument2 SeitenRelated Literature and StudiesJudyNoch keine Bewertungen

- WHAT IS ACCOUNTINGDokument7 SeitenWHAT IS ACCOUNTINGJudyNoch keine Bewertungen

- WC2Dokument3 SeitenWC2JudyNoch keine Bewertungen

- Dmat ReportDokument130 SeitenDmat ReportparasarawgiNoch keine Bewertungen

- Needs and Language Goals of Students, Creating Learning Environments andDokument3 SeitenNeeds and Language Goals of Students, Creating Learning Environments andapi-316528766Noch keine Bewertungen

- SAP HANA Analytics Training at MAJUDokument1 SeiteSAP HANA Analytics Training at MAJUXINoch keine Bewertungen

- Experiment 5 ADHAVANDokument29 SeitenExperiment 5 ADHAVANManoj Raj RajNoch keine Bewertungen

- Academic Transcript Of:: Issued To StudentDokument3 SeitenAcademic Transcript Of:: Issued To Studentjrex209Noch keine Bewertungen

- Ardipithecus Ramidus Is A Hominin Species Dating To Between 4.5 and 4.2 Million Years AgoDokument5 SeitenArdipithecus Ramidus Is A Hominin Species Dating To Between 4.5 and 4.2 Million Years AgoBianca IrimieNoch keine Bewertungen

- Second Periodic Test - 2018-2019Dokument21 SeitenSecond Periodic Test - 2018-2019JUVELYN BELLITANoch keine Bewertungen

- Cambridge Intl. Sr. Sec. School Class: X, Preboard Examination-1 Subject: Mathematics Time Allowed: 3Hrs. M.M: 80Dokument5 SeitenCambridge Intl. Sr. Sec. School Class: X, Preboard Examination-1 Subject: Mathematics Time Allowed: 3Hrs. M.M: 80Suyash PandeyNoch keine Bewertungen

- Day1 1Dokument17 SeitenDay1 1kaganp784Noch keine Bewertungen

- Bluetooth Mobile Based College CampusDokument12 SeitenBluetooth Mobile Based College CampusPruthviraj NayakNoch keine Bewertungen

- Ethical CRM PracticesDokument21 SeitenEthical CRM Practicesanon_522592057Noch keine Bewertungen

- Graphic Design Review Paper on Pop Art MovementDokument16 SeitenGraphic Design Review Paper on Pop Art MovementFathan25 Tanzilal AziziNoch keine Bewertungen

- Contribution Sushruta AnatomyDokument5 SeitenContribution Sushruta AnatomyEmmanuelle Soni-DessaigneNoch keine Bewertungen

- Corneal Ulcers: What Is The Cornea?Dokument1 SeiteCorneal Ulcers: What Is The Cornea?me2_howardNoch keine Bewertungen

- As 3778.6.3-1992 Measurement of Water Flow in Open Channels Measuring Devices Instruments and Equipment - CalDokument7 SeitenAs 3778.6.3-1992 Measurement of Water Flow in Open Channels Measuring Devices Instruments and Equipment - CalSAI Global - APACNoch keine Bewertungen

- Duah'sDokument3 SeitenDuah'sZareefNoch keine Bewertungen

- B.A./B.Sc.: SyllabusDokument185 SeitenB.A./B.Sc.: SyllabusKaran VeerNoch keine Bewertungen

- Book of ProtectionDokument69 SeitenBook of ProtectiontrungdaongoNoch keine Bewertungen

- HexaflexDokument10 SeitenHexaflexCharlie Williams100% (1)

- Productivity in Indian Sugar IndustryDokument17 SeitenProductivity in Indian Sugar Industryshahil_4uNoch keine Bewertungen

- Downloaded From Uva-Dare, The Institutional Repository of The University of Amsterdam (Uva)Dokument12 SeitenDownloaded From Uva-Dare, The Institutional Repository of The University of Amsterdam (Uva)Iqioo RedefiniNoch keine Bewertungen

- Automatic Night LampDokument22 SeitenAutomatic Night LampAryan SheoranNoch keine Bewertungen

- Midterms and Finals Topics for Statistics at University of the CordillerasDokument2 SeitenMidterms and Finals Topics for Statistics at University of the Cordillerasjohny BraveNoch keine Bewertungen

- Ice Task 2Dokument2 SeitenIce Task 2nenelindelwa274Noch keine Bewertungen

- Converting Units of Measure PDFDokument23 SeitenConverting Units of Measure PDFM Faisal ChNoch keine Bewertungen

- ME Flowchart 2014 2015Dokument2 SeitenME Flowchart 2014 2015Mario ManciaNoch keine Bewertungen

- Exodus Post Apocalyptic PDF 10Dokument2 SeitenExodus Post Apocalyptic PDF 10RushabhNoch keine Bewertungen

- UTS - Comparative Literature - Indah Savitri - S1 Sastra Inggris - 101201001Dokument6 SeitenUTS - Comparative Literature - Indah Savitri - S1 Sastra Inggris - 101201001indahcantik1904Noch keine Bewertungen

- TemplateDokument1 SeiteTemplatemaheshqwNoch keine Bewertungen

- United States v. Christopher King, 724 F.2d 253, 1st Cir. (1984)Dokument9 SeitenUnited States v. Christopher King, 724 F.2d 253, 1st Cir. (1984)Scribd Government DocsNoch keine Bewertungen