Das könnte Ihnen auch gefallen

- Risk & ReturnDokument20 SeitenRisk & Returnjhumli100% (1)

- Simplified by Florendo D. Damaso, JR., Cbe InstructorDokument17 SeitenSimplified by Florendo D. Damaso, JR., Cbe InstructorFlor DamasoNoch keine Bewertungen

- Two Views of Social ResponsibilityDokument4 SeitenTwo Views of Social ResponsibilityKathc Azur100% (1)

- History of Economic ThoughtDokument49 SeitenHistory of Economic ThoughtMateuNoch keine Bewertungen

- CA2 Cost Concepts and ClassificationDokument19 SeitenCA2 Cost Concepts and ClassificationhellokittysaranghaeNoch keine Bewertungen

- Theory of ProductionDokument31 SeitenTheory of ProductionSom AcharyaNoch keine Bewertungen

- Lecture 1 Chapter 1 TodaroDokument24 SeitenLecture 1 Chapter 1 TodaroKhadeeza ShammeeNoch keine Bewertungen

- Chapter 2Dokument5 SeitenChapter 2Sundaramani SaranNoch keine Bewertungen

- TATA 1MG Healthcare Solutions Private Limited: Wadi On Jalamb Road Khamgaon,, Buldhana, 444303, IndiaDokument1 SeiteTATA 1MG Healthcare Solutions Private Limited: Wadi On Jalamb Road Khamgaon,, Buldhana, 444303, IndiaTejas Talole0% (1)

- The Philippine Financial SystemDokument17 SeitenThe Philippine Financial SystemCharisa SamsonNoch keine Bewertungen

- Module 2Dokument17 SeitenModule 2Maxine RubiaNoch keine Bewertungen

- Labor Quality: Investing in Human CapitalDokument41 SeitenLabor Quality: Investing in Human CapitalMuhammad HassamNoch keine Bewertungen

- Simple Linear RegressionDokument24 SeitenSimple Linear Regressionইশতিয়াক হোসেন সিদ্দিকীNoch keine Bewertungen

- Hyundai Forklift Trucks Service Manual Updated 09 2021 Offline DVDDokument23 SeitenHyundai Forklift Trucks Service Manual Updated 09 2021 Offline DVDwalterwatts010985wqa100% (129)

- Sallys Struthers - Answer KeyDokument7 SeitenSallys Struthers - Answer KeyLlyod Francis LaylayNoch keine Bewertungen

- 5.tender Process N DocumentationDokument35 Seiten5.tender Process N DocumentationDilanka MJ Dassanayake100% (1)

- Interest Rates and Bond ValuationDokument75 SeitenInterest Rates and Bond ValuationOday Ru100% (1)

- Lecture Note in EconomicsDokument3 SeitenLecture Note in EconomicsJohn Remmel RogaNoch keine Bewertungen

- FINC 304 Managerial EconomicsDokument21 SeitenFINC 304 Managerial EconomicsJephthah BansahNoch keine Bewertungen

- Module Financial InstitutionDokument13 SeitenModule Financial InstitutionZeeshan NazirNoch keine Bewertungen

- Impacts of Economics System On International BusinessDokument8 SeitenImpacts of Economics System On International BusinessKhalid AminNoch keine Bewertungen

- Top Differences Between Economic Growth and Economic DevelopmentDokument9 SeitenTop Differences Between Economic Growth and Economic Developmentsho555redhot_4840874Noch keine Bewertungen

- MBA 103 Chapter 12Dokument27 SeitenMBA 103 Chapter 12Art Virgel DensingNoch keine Bewertungen

- Admas University Faculty of Business: Department of Accounting and Finance Course OutlineDokument5 SeitenAdmas University Faculty of Business: Department of Accounting and Finance Course Outlineeyob astatkeNoch keine Bewertungen

- 5.3 Break-Even Analysis Test PDFDokument2 Seiten5.3 Break-Even Analysis Test PDFGermanRobertoFong100% (1)

- Financial InstitutionsDokument17 SeitenFinancial InstitutionsNuahs MagahatNoch keine Bewertungen

- An Overview of Financial SystemDokument4 SeitenAn Overview of Financial SystemYee Sin MeiNoch keine Bewertungen

- CONSUMPTION and SAVINGSDokument26 SeitenCONSUMPTION and SAVINGShyunsuk fhebieNoch keine Bewertungen

- Introduction To Public FinanceDokument9 SeitenIntroduction To Public FinanceJ lodhi50% (2)

- Financial Market in Pakistan: Financial Markets and Their Roles: Commercial BanksDokument5 SeitenFinancial Market in Pakistan: Financial Markets and Their Roles: Commercial BanksAnamMalikNoch keine Bewertungen

- Chapter 1 - Introduction To InvestmentDokument30 SeitenChapter 1 - Introduction To InvestmentAnh ĐỗNoch keine Bewertungen

- Capital Budgeting Case StudyDokument2 SeitenCapital Budgeting Case StudyAnand Prakash Sharma100% (1)

- Continuous Distributions and The Normal Distribution: Notation: Probability Density Function PDFDokument5 SeitenContinuous Distributions and The Normal Distribution: Notation: Probability Density Function PDFPal AjayNoch keine Bewertungen

- Statement of Cash Flows: Learning ObjectivesDokument49 SeitenStatement of Cash Flows: Learning ObjectivesPrima Rosita AriniNoch keine Bewertungen

- Cmrmiranda Powerpoint Presentation November2011 Macro EconomicsDokument15 SeitenCmrmiranda Powerpoint Presentation November2011 Macro EconomicsjameskagomeNoch keine Bewertungen

- Griffin Fob 1e Chapter 15Dokument23 SeitenGriffin Fob 1e Chapter 15Ace LaliconNoch keine Bewertungen

- Estimating Demand FunctionDokument45 SeitenEstimating Demand FunctionManisha AdliNoch keine Bewertungen

- Managerial EconomicsDokument7 SeitenManagerial EconomicsRam SoniNoch keine Bewertungen

- Factors Affecting Economic Development PDFDokument2 SeitenFactors Affecting Economic Development PDFTara0% (2)

- 001b 10 Principles of EconomicsDokument7 Seiten001b 10 Principles of EconomicsAbigael Esmena100% (1)

- Chapter 2-Market and Market SegmentationDokument25 SeitenChapter 2-Market and Market SegmentationMA ValdezNoch keine Bewertungen

- Rostow's TheoryDokument3 SeitenRostow's TheoryNazish SohailNoch keine Bewertungen

- Business EthicsDokument23 SeitenBusiness EthicsjonathanNoch keine Bewertungen

- Economics Chapter 4-9Dokument51 SeitenEconomics Chapter 4-9Warwick PangilinanNoch keine Bewertungen

- Accounting Conceptual FrameworkDokument2 SeitenAccounting Conceptual FrameworkCasey CallaghanNoch keine Bewertungen

- UNIT 4 AnswerDokument3 SeitenUNIT 4 AnswerSantiago Orellana CNoch keine Bewertungen

- Chapter 3 Classical Theories For Economic Growth and DevelopmentDokument6 SeitenChapter 3 Classical Theories For Economic Growth and DevelopmentJoseph DoctoNoch keine Bewertungen

- I. Introduction To Managerial EconomicsDokument5 SeitenI. Introduction To Managerial EconomicsJerico ManaloNoch keine Bewertungen

- Adjusting Entries ActsDokument5 SeitenAdjusting Entries ActsLori100% (1)

- MFI Unit 01Dokument13 SeitenMFI Unit 01Shreejan PandeyNoch keine Bewertungen

- Managerial Economics - A Decision Science andDokument5 SeitenManagerial Economics - A Decision Science andSam NietNoch keine Bewertungen

- Obstacles and Implementation of Accounting Software System in Small Medium Enterprises (SMEs) : Case of South Asian Perspective.Dokument9 SeitenObstacles and Implementation of Accounting Software System in Small Medium Enterprises (SMEs) : Case of South Asian Perspective.ijsab.comNoch keine Bewertungen

- Econometrics Module 2Dokument38 SeitenEconometrics Module 2chatfieldlohrNoch keine Bewertungen

- 1621 - Stat6111 - Loba - TK1 - W1 - S2 - Team5Dokument5 Seiten1621 - Stat6111 - Loba - TK1 - W1 - S2 - Team5Murni HandayaniNoch keine Bewertungen

- Ordinary Least Square EstimationDokument30 SeitenOrdinary Least Square Estimationthrphys1940Noch keine Bewertungen

- Investment and Portfolio Chapter 4Dokument48 SeitenInvestment and Portfolio Chapter 4MarjonNoch keine Bewertungen

- Interest Rates and Their Role in FinanceDokument17 SeitenInterest Rates and Their Role in FinanceClyden Jaile RamirezNoch keine Bewertungen

- Document 1Dokument38 SeitenDocument 1gosaye desalegnNoch keine Bewertungen

- InvestmentDokument31 SeitenInvestmentCarlo Emmanuel Balane100% (1)

- The Financial SystemDokument11 SeitenThe Financial SystemDipika TambeNoch keine Bewertungen

- Value Chain Management Capability A Complete Guide - 2020 EditionVon EverandValue Chain Management Capability A Complete Guide - 2020 EditionNoch keine Bewertungen

- The real Keynesian Theory, explained brief and simpleVon EverandThe real Keynesian Theory, explained brief and simpleNoch keine Bewertungen

- Organizational Behavior and Leadership A Complete GuideVon EverandOrganizational Behavior and Leadership A Complete GuideNoch keine Bewertungen

- Amul Project Report FinalsssDokument38 SeitenAmul Project Report FinalsssPratik Rakesh BakliwalNoch keine Bewertungen

- The Research On Impact of International Trade On China's EconomicDokument2 SeitenThe Research On Impact of International Trade On China's EconomicLukman MasaNoch keine Bewertungen

- Toppan Merrill Technology ListDokument2 SeitenToppan Merrill Technology ListKilty ONealNoch keine Bewertungen

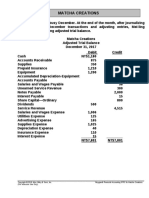

- MC4 Matcha Creations: (For Instructor Use Only)Dokument2 SeitenMC4 Matcha Creations: (For Instructor Use Only)Reza eka PutraNoch keine Bewertungen

- Guide To SQL 9th Edition by Pratt Last Solution ManualDokument13 SeitenGuide To SQL 9th Edition by Pratt Last Solution Manualcatherinebergtjkxfanwod100% (25)

- Tutorial Letter 201/1/2017: Distinctive Financial ReportingDokument8 SeitenTutorial Letter 201/1/2017: Distinctive Financial ReportingItumeleng KekanaNoch keine Bewertungen

- The Star SydneyDokument12 SeitenThe Star SydneyKLIOMARIE ANNE CURUGANNoch keine Bewertungen

- Other SourceDokument43 SeitenOther SourceJai RajNoch keine Bewertungen

- M3 - Run Checklist (MUDA, MURI, MURA) : M3 - Topic What Do You See? (Issue) How To Improve (Action)Dokument3 SeitenM3 - Run Checklist (MUDA, MURI, MURA) : M3 - Topic What Do You See? (Issue) How To Improve (Action)abhasNoch keine Bewertungen

- 30 Pantry Organization Ideas and Tricks - How To Organize A PantryDokument1 Seite30 Pantry Organization Ideas and Tricks - How To Organize A PantryCKNoch keine Bewertungen

- Epiforce: Protecting Personal InformationDokument4 SeitenEpiforce: Protecting Personal InformationLuke TerringtonNoch keine Bewertungen

- Employee Performance Management Literature ReviewDokument6 SeitenEmployee Performance Management Literature Reviewea8d1b6nNoch keine Bewertungen

- Wiley CFA Test Bank 180527 (20 Preguntas)Dokument12 SeitenWiley CFA Test Bank 180527 (20 Preguntas)rafav10Noch keine Bewertungen

- Salem2019 PDFDokument10 SeitenSalem2019 PDFRifa ArvandoNoch keine Bewertungen

- Construction ContractDokument17 SeitenConstruction ContractYvonne Gam-oyNoch keine Bewertungen

- Golden Rules For AccountingDokument4 SeitenGolden Rules For AccountingRoshani ChaudhariNoch keine Bewertungen

- 01-CalapanCity2019 Transmittal LetterDokument6 Seiten01-CalapanCity2019 Transmittal LetterkQy267BdTKNoch keine Bewertungen

- Strother v. 3464920 Canada Inc.Dokument2 SeitenStrother v. 3464920 Canada Inc.Alice JiangNoch keine Bewertungen

- Jakawali ParachuteDokument1 SeiteJakawali Parachuteparasailing jakartaNoch keine Bewertungen

- Causes of Low Literacy Rate in PakistanDokument27 SeitenCauses of Low Literacy Rate in PakistanSaba Naeem82% (17)

- L.C.Gupta Committee PurposeDokument3 SeitenL.C.Gupta Committee PurposeAbhishek Kumar SinghNoch keine Bewertungen

- Problems On Ages Questions Specially For Sbi Po PrelimsDokument18 SeitenProblems On Ages Questions Specially For Sbi Po Prelimsabinusundaram0Noch keine Bewertungen

- PMP 2022Dokument96 SeitenPMP 2022Kim Katey KanorNoch keine Bewertungen

- Research On Fastrack WatchesDokument23 SeitenResearch On Fastrack Watcheskk_kamal40% (5)

- Hdpe Pipe Electro Fusion Fittings Price ListDokument18 SeitenHdpe Pipe Electro Fusion Fittings Price ListSantiago MoraNoch keine Bewertungen

- Food DayDokument15 SeitenFood DaydigdagNoch keine Bewertungen