Das könnte Ihnen auch gefallen

- USA State-Wise Email Leads PDFDokument6 SeitenUSA State-Wise Email Leads PDFSimeon Dwight100% (1)

- Slides International Taxation 2Dokument17 SeitenSlides International Taxation 2yebegashetNoch keine Bewertungen

- Module 1 - Basics of CostingDokument40 SeitenModule 1 - Basics of Costingmaheshbendigeri5945Noch keine Bewertungen

- Cost AccountingDokument13 SeitenCost AccountingTanishq KambojNoch keine Bewertungen

- The Foreign Exchange MarketDokument16 SeitenThe Foreign Exchange Marketmanojpatel5167% (3)

- Industrial RelationsDokument13 SeitenIndustrial Relationsmashion87Noch keine Bewertungen

- Financial Accounting Theory Craig Deegan Chapter 2Dokument34 SeitenFinancial Accounting Theory Craig Deegan Chapter 2Siti AdawiyahNoch keine Bewertungen

- Blackbook Project On Venture Capital PDFDokument83 SeitenBlackbook Project On Venture Capital PDFSam ShaikhNoch keine Bewertungen

- AMUL's Distribution ChannelDokument16 SeitenAMUL's Distribution ChannelPrateek Jain100% (1)

- Structure of AccountingDokument62 SeitenStructure of AccountingSyafira AdeliaNoch keine Bewertungen

- Balance of PaymentDokument4 SeitenBalance of PaymentAMALA ANoch keine Bewertungen

- Accounting Theory Project 1 - MayaDokument18 SeitenAccounting Theory Project 1 - MayaDima AbdulhayNoch keine Bewertungen

- The Nature of Accounting Theory and The Development of TheoryDokument6 SeitenThe Nature of Accounting Theory and The Development of TheoryEngrAbeer Arif100% (1)

- Direct TaxDokument3 SeitenDirect TaxkashanircNoch keine Bewertungen

- Cost and Management AccountingDokument51 SeitenCost and Management Accountingabhijeet0% (1)

- Lease Financing: Learning OutcomesDokument31 SeitenLease Financing: Learning Outcomesravi sharma100% (1)

- ACCOUNTING: Concepts & ConventionsDokument34 SeitenACCOUNTING: Concepts & Conventionsmehul100% (11)

- Module 2.1-Cost of CapitalDokument12 SeitenModule 2.1-Cost of CapitalBheemeswar ReddyNoch keine Bewertungen

- AcctTheory - Chap06 Structure of Accounting Theory (Belkaoui)Dokument29 SeitenAcctTheory - Chap06 Structure of Accounting Theory (Belkaoui)Aurora AzzahraNoch keine Bewertungen

- 19P0310314 - Corporate Tax Planning - Meaning, Objectives and ScopeDokument8 Seiten19P0310314 - Corporate Tax Planning - Meaning, Objectives and ScopePriya KudnekarNoch keine Bewertungen

- TdsDokument22 SeitenTdsFRANCIS JOSEPHNoch keine Bewertungen

- Principles of Accounting (Chapter-01) Lecture Sheet BBA VISIONDokument9 SeitenPrinciples of Accounting (Chapter-01) Lecture Sheet BBA VISIONJareen Binte AsadNoch keine Bewertungen

- Taxation - Income TaxDokument158 SeitenTaxation - Income Taxnaren197667% (6)

- Risk and ReturnDokument19 SeitenRisk and ReturnLeny MichaelNoch keine Bewertungen

- The Management of Foreign Exchange RiskDokument97 SeitenThe Management of Foreign Exchange RiskVajira Weerasena100% (1)

- Intermediate Accounting, 11th Ed. Kieso, Weygandt, and WarfieldDokument27 SeitenIntermediate Accounting, 11th Ed. Kieso, Weygandt, and Warfieldheart05100% (1)

- Tax Planning With Reference To Managerial RemunerationDokument3 SeitenTax Planning With Reference To Managerial RemunerationashurebelNoch keine Bewertungen

- Designing Capital StructureDokument13 SeitenDesigning Capital StructuresiddharthdileepkamatNoch keine Bewertungen

- Components of Financial SystemDokument11 SeitenComponents of Financial SystemromaNoch keine Bewertungen

- Transfer PricingDokument20 SeitenTransfer PricingPhaniraj Lenkalapally0% (1)

- Financial Intermediaries and Their FunctionsDokument2 SeitenFinancial Intermediaries and Their FunctionsBrandon LumibaoNoch keine Bewertungen

- Uniform CostDokument5 SeitenUniform CostJASMINE REGI100% (2)

- Hire Purchase SystemDokument13 SeitenHire Purchase SystemDeepak Dhingra100% (1)

- Corporate Governance Report of InfosysDokument33 SeitenCorporate Governance Report of InfosysAstha Shiv100% (2)

- 11 Determinants of Working Capital - Financial ManagementDokument3 Seiten11 Determinants of Working Capital - Financial ManagementsharmilaNoch keine Bewertungen

- Tradeoff Theory of Capital StructureDokument10 SeitenTradeoff Theory of Capital StructureSyed Peer Muhammad ShahNoch keine Bewertungen

- Advance TaxDokument11 SeitenAdvance TaxAdv Aastha MakkarNoch keine Bewertungen

- Ch-2 Elements of Cost and Classification of CostDokument25 SeitenCh-2 Elements of Cost and Classification of CostEruNoch keine Bewertungen

- 6,6 Taxation of Income of PersonsDokument29 Seiten6,6 Taxation of Income of Personsjoseph mbuguaNoch keine Bewertungen

- Working Capital Management FinanceDokument16 SeitenWorking Capital Management FinanceHims75% (8)

- Financial ServicesDokument40 SeitenFinancial ServicesIsha Chandok100% (1)

- How Financial Statements Are UsedDokument75 SeitenHow Financial Statements Are UsedKristina KittyNoch keine Bewertungen

- Public Awareness of TaxDokument12 SeitenPublic Awareness of TaxDilli Raj PandeyNoch keine Bewertungen

- Cost and Management AccountingDokument18 SeitenCost and Management AccountingAbdur RahmanNoch keine Bewertungen

- 1 - 4. Issues Involved in Overseas Funding ChoicesDokument7 Seiten1 - 4. Issues Involved in Overseas Funding ChoicesShubham ArgadeNoch keine Bewertungen

- Chapter 7 CapitalisationDokument19 SeitenChapter 7 CapitalisationPooja SheoranNoch keine Bewertungen

- Chapter TwoDokument54 SeitenChapter Twoyechale tafereNoch keine Bewertungen

- Integrated and Non Integrated System of AccountingDokument46 SeitenIntegrated and Non Integrated System of AccountingGanesh Nikam67% (3)

- Factoring Advantages and Dis AdvantagesDokument1 SeiteFactoring Advantages and Dis AdvantagesSiva RockNoch keine Bewertungen

- The Cost of CapitalDokument18 SeitenThe Cost of CapitalzewdieNoch keine Bewertungen

- Cost of Capital PDFDokument34 SeitenCost of Capital PDFMathilda UllyNoch keine Bewertungen

- 1.01 GAAP PowerPoint 1-5Dokument56 Seiten1.01 GAAP PowerPoint 1-5Anonymous 1IzSQFJR100% (1)

- Government Without Any Expectation of Direct Return in Benefit ". Ability To Pay. Taxed in The Same Way Without Any DiscriminationDokument42 SeitenGovernment Without Any Expectation of Direct Return in Benefit ". Ability To Pay. Taxed in The Same Way Without Any DiscriminationyebegashetNoch keine Bewertungen

- Job, Batch, ContractDokument25 SeitenJob, Batch, ContractParminder Bajaj100% (1)

- 1 TaxplanningchapterDokument60 Seiten1 TaxplanningchapterGieanne Prudence Venculado100% (1)

- IFRS Ethiopia D1S3 Presentation and Disclosure 3Dokument69 SeitenIFRS Ethiopia D1S3 Presentation and Disclosure 3Yalem Alemayehu100% (1)

- Advanced Financial Accounting Under IFRS - Lecture Notes - FinalDokument89 SeitenAdvanced Financial Accounting Under IFRS - Lecture Notes - Finalnicodimoana100% (1)

- Accounting Theory (Question Patterns)Dokument2 SeitenAccounting Theory (Question Patterns)Shaheen Mahmud100% (3)

- Note 4Dokument116 SeitenNote 4sohamdivekar9867Noch keine Bewertungen

- Transfer PricingDokument111 SeitenTransfer PricingMamun0% (1)

- Bos 53930 CP 1Dokument121 SeitenBos 53930 CP 1arashpreet kaur dhanjuNoch keine Bewertungen

- Id Kai Transfer Pricing 2016 NewDokument12 SeitenId Kai Transfer Pricing 2016 NewMarsheliana PutriNoch keine Bewertungen

- Vodacoin Is The Product Selected To Implement in The Rwandese MarketDokument3 SeitenVodacoin Is The Product Selected To Implement in The Rwandese MarketHamza ZainNoch keine Bewertungen

- Online - Chapter 2Dokument10 SeitenOnline - Chapter 2Gladys CanterosNoch keine Bewertungen

- Accenture Tying The Knot Between Risk and Performance ManagementDokument16 SeitenAccenture Tying The Knot Between Risk and Performance Managementkinky72100% (1)

- Sustainability 13 01029 v3Dokument89 SeitenSustainability 13 01029 v3Getacho EjetaNoch keine Bewertungen

- Business Markets and Business Buyer BehaviorDokument21 SeitenBusiness Markets and Business Buyer BehaviorMansoor KhalidNoch keine Bewertungen

- Classification of Financial MarketsDokument12 SeitenClassification of Financial Marketsvijaybhaskarreddymee67% (6)

- Strama Quiz 4Dokument5 SeitenStrama Quiz 4Norhel FangedNoch keine Bewertungen

- Related Local LiteratureDokument3 SeitenRelated Local LiteratureGlaidel Rodenas PeñaNoch keine Bewertungen

- This Example Business Meeting Is Followed by The Two Sections Which Provide Key Language and Phrases Appropriate For Typical Business MeetingsDokument2 SeitenThis Example Business Meeting Is Followed by The Two Sections Which Provide Key Language and Phrases Appropriate For Typical Business MeetingsfatimetouNoch keine Bewertungen

- Essay Test ECO 111 - IB1717Dokument4 SeitenEssay Test ECO 111 - IB1717Phan Thị Thanh ThảoNoch keine Bewertungen

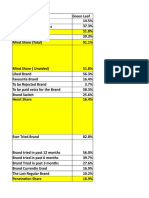

- Brand Health Analysis TemplateDokument4 SeitenBrand Health Analysis Templateanon_493704527Noch keine Bewertungen

- On Marketing Mba 2nd SemesterDokument6 SeitenOn Marketing Mba 2nd SemesterVIKASHPUROHITNoch keine Bewertungen

- Boutique (Riwaj) EditDokument15 SeitenBoutique (Riwaj) Editapi-3700872100% (5)

- TDLR Chart Book 2010-05-03Dokument34 SeitenTDLR Chart Book 2010-05-03Anthony DavianNoch keine Bewertungen

- AssignmentDokument11 SeitenAssignmentMuhammad MuazzamNoch keine Bewertungen

- Transition Economies: An IMF Perspective On Progress and ProspectsDokument15 SeitenTransition Economies: An IMF Perspective On Progress and Prospectsphani_rapNoch keine Bewertungen

- Economics Today The Macro View 19th Edition Miller Solutions ManualDokument19 SeitenEconomics Today The Macro View 19th Edition Miller Solutions Manualtusseh.itemm0lh100% (22)

- Cost of CapitalDokument2 SeitenCost of Capitalkomal100% (1)

- Product Life CycleDokument3 SeitenProduct Life CycleHarry LobleNoch keine Bewertungen

- Usha Quartz Room HeaterDokument1 SeiteUsha Quartz Room HeaterArunNoch keine Bewertungen

- Sri Handaru Yuliati Business Plan 3 Faculty Economics and Business Universitas Gadjah MadDokument25 SeitenSri Handaru Yuliati Business Plan 3 Faculty Economics and Business Universitas Gadjah MadAfifah KhairunaNoch keine Bewertungen

- Minggu 8 - MonopoliDokument80 SeitenMinggu 8 - MonopoliDevina GabriellaNoch keine Bewertungen

- Proposal For Property Investment & Sales ServicesDokument3 SeitenProposal For Property Investment & Sales ServicesMuhammad AsifNoch keine Bewertungen

- Customer Service in Supply Chain ManagementDokument9 SeitenCustomer Service in Supply Chain ManagementRaghavendra KaladiNoch keine Bewertungen

- Invisible HandDokument12 SeitenInvisible HanddebangeesahooNoch keine Bewertungen

- Blue Ocean Strategy: From Theory To Practice: Case AnalysisDokument8 SeitenBlue Ocean Strategy: From Theory To Practice: Case Analysisshukla224Noch keine Bewertungen

- Finance pt2 QB NEWDokument71 SeitenFinance pt2 QB NEWBharath BMNoch keine Bewertungen