Das könnte Ihnen auch gefallen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5795)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1091)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- Lesson 2 - The RPA Business Analyst - Role, Skills and Challenges PDFDokument5 SeitenLesson 2 - The RPA Business Analyst - Role, Skills and Challenges PDFCECILIA ESPINOZA FUMEAUXNoch keine Bewertungen

- Final EtechDokument21 SeitenFinal EtechApril AguigamNoch keine Bewertungen

- Tutorial 9 Suggested SolutionsDokument11 SeitenTutorial 9 Suggested SolutionsChloe GuilaNoch keine Bewertungen

- Elementary - Stop & Check - 1Dokument6 SeitenElementary - Stop & Check - 1Nursultan100% (2)

- The Accounting Cycle:: Accruals and DeferralsDokument41 SeitenThe Accounting Cycle:: Accruals and DeferralsNursultanNoch keine Bewertungen

- Williams 08Dokument63 SeitenWilliams 08NursultanNoch keine Bewertungen

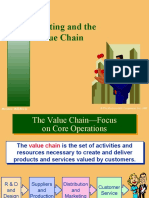

- Costing and The Value Chain: Mcgraw-Hill/IrwinDokument36 SeitenCosting and The Value Chain: Mcgraw-Hill/IrwinNursultanNoch keine Bewertungen

- Global Business and Accounting: Mcgraw-Hill/IrwinDokument23 SeitenGlobal Business and Accounting: Mcgraw-Hill/IrwinNursultanNoch keine Bewertungen

- Reflective Essay 3 - PDIC Truth in Lending Act & Secrecy of Bank DepositDokument2 SeitenReflective Essay 3 - PDIC Truth in Lending Act & Secrecy of Bank DepositCha BuenaventuraNoch keine Bewertungen

- Marketing Management (PDFDrive)Dokument356 SeitenMarketing Management (PDFDrive)Kiko HuitNoch keine Bewertungen

- National Tyre Services Limited: Abridged Audited Financial Results For The Year Ended 31 March 2018Dokument2 SeitenNational Tyre Services Limited: Abridged Audited Financial Results For The Year Ended 31 March 2018Absai MausaNoch keine Bewertungen

- International MarketingDokument7 SeitenInternational MarketingNikunj BajajNoch keine Bewertungen

- Solar Engineering Consultants - SgurrEnergyDokument6 SeitenSolar Engineering Consultants - SgurrEnergySgurr EnergyNoch keine Bewertungen

- Internship Report FormatDokument21 SeitenInternship Report FormatSakshi SinghNoch keine Bewertungen

- Woolworths Limited Risk Management PolicyDokument3 SeitenWoolworths Limited Risk Management PolicyQuang HuyNoch keine Bewertungen

- The Performance Appraisal Handbook-Lega Lpractical Rules For ManagersDokument224 SeitenThe Performance Appraisal Handbook-Lega Lpractical Rules For ManagersNagashree Ranjith100% (2)

- Bank Reconciliation: BankrecDokument3 SeitenBank Reconciliation: BankrecAlice SongNoch keine Bewertungen

- Unit IDokument40 SeitenUnit IVeronica SafrinaNoch keine Bewertungen

- Employee Engagement: Conceptual Clarification From Existing Confusion and Towards An Instrument of Measuring ItDokument26 SeitenEmployee Engagement: Conceptual Clarification From Existing Confusion and Towards An Instrument of Measuring ItNhan NguyenNoch keine Bewertungen

- GL Bajaj Institute of Management and Research Greater Noida: Abhishek Srivastava ROLL NO: GM19010 Section: BDokument6 SeitenGL Bajaj Institute of Management and Research Greater Noida: Abhishek Srivastava ROLL NO: GM19010 Section: Brahul singhNoch keine Bewertungen

- Zamboanga City: The SiteDokument36 SeitenZamboanga City: The SiteDiana TraniNoch keine Bewertungen

- Human Resource ManagementDokument15 SeitenHuman Resource Managementsomasekhar reddy1908Noch keine Bewertungen

- Ais WK2Dokument33 SeitenAis WK2MikaNoch keine Bewertungen

- Gelinas Dull and Wheeler - Chapter 9Dokument41 SeitenGelinas Dull and Wheeler - Chapter 9bendermacherrickNoch keine Bewertungen

- Applied Eco Q4 Lesson 3Dokument11 SeitenApplied Eco Q4 Lesson 3Alfred Jornalero CartaNoch keine Bewertungen

- LSM DA-3 Topic: Business Plans: 18BME2110 Kartikey SinghDokument5 SeitenLSM DA-3 Topic: Business Plans: 18BME2110 Kartikey SinghkartikeyNoch keine Bewertungen

- Liabilities: The ofDokument13 SeitenLiabilities: The ofMCDABCNoch keine Bewertungen

- Max SIP ProjectDokument103 SeitenMax SIP ProjectRuhiNoch keine Bewertungen

- Portfolio Management Services Literature ReviewDokument8 SeitenPortfolio Management Services Literature Reviewea3f29j7Noch keine Bewertungen

- Operation ManagementDokument10 SeitenOperation ManagementPritam RoyNoch keine Bewertungen

- Commercial Law Review Cases in InsuranceDokument1 SeiteCommercial Law Review Cases in InsuranceCinja ShidoujiNoch keine Bewertungen

- HRDDokument20 SeitenHRDSiti NuraziraNoch keine Bewertungen

- The World of Commercial Real Estate - GelbtuckDokument7 SeitenThe World of Commercial Real Estate - GelbtuckJacob YangNoch keine Bewertungen

- Dawlance 1Dokument11 SeitenDawlance 1SparksNoch keine Bewertungen

- Olap Analytical Solution For Human Resource Management Performance Measurement and Evaluation: From Theoretical Concepts To ApplicationDokument5 SeitenOlap Analytical Solution For Human Resource Management Performance Measurement and Evaluation: From Theoretical Concepts To Applicationvjayz77Noch keine Bewertungen