Das könnte Ihnen auch gefallen

- International Corporate FinanceDokument31 SeitenInternational Corporate FinancegagafikNoch keine Bewertungen

- Cash and Liquidity ManagementDokument27 SeitenCash and Liquidity ManagementgagafikNoch keine Bewertungen

- Credit and Inventory ManagementDokument32 SeitenCredit and Inventory ManagementgagafikNoch keine Bewertungen

- Options and Corporate FinanceDokument26 SeitenOptions and Corporate FinancegagafikNoch keine Bewertungen

- Cost of CapitalDokument35 SeitenCost of CapitalgagafikNoch keine Bewertungen

- Financial Statements, Taxes, and Cash FlowDokument46 SeitenFinancial Statements, Taxes, and Cash FlowgagafikNoch keine Bewertungen

- Raising CapitalDokument64 SeitenRaising CapitalgagafikNoch keine Bewertungen

- De Beers and NestleDokument4 SeitenDe Beers and NestlegagafikNoch keine Bewertungen

- Dutch Flower Cluster v2Dokument9 SeitenDutch Flower Cluster v2gagafikNoch keine Bewertungen

- Working With Financial StatementsDokument32 SeitenWorking With Financial StatementsgagafikNoch keine Bewertungen

- Dutch Flower and IcelandDokument5 SeitenDutch Flower and IcelandgagafikNoch keine Bewertungen

- Questions AnswersDokument13 SeitenQuestions Answersgagafik100% (1)

- EconDokument2 SeitenEcongagafikNoch keine Bewertungen

- Analyzing The Economic Situation in Cot D'ivoire, It Is Developing Country With IncreasingDokument1 SeiteAnalyzing The Economic Situation in Cot D'ivoire, It Is Developing Country With IncreasinggagafikNoch keine Bewertungen

- Competitividad Internacional AD-6010: CaseDokument3 SeitenCompetitividad Internacional AD-6010: CasegagafikNoch keine Bewertungen

- The Dutch Flower Cluster ReportDokument18 SeitenThe Dutch Flower Cluster ReportgagafikNoch keine Bewertungen

- Tsis Analysis of Cot D'ivoire Economics: Department of Economics and Management Principle of EconomicsDokument3 SeitenTsis Analysis of Cot D'ivoire Economics: Department of Economics and Management Principle of EconomicsgagafikNoch keine Bewertungen

- Tsis Analysis of Namibia EconomicsDokument7 SeitenTsis Analysis of Namibia EconomicsgagafikNoch keine Bewertungen

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (345)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- Finance QuizDokument13 SeitenFinance QuizNadaineNoch keine Bewertungen

- Formato Cis DanielDokument5 SeitenFormato Cis DanielDaniel Toro100% (5)

- Commodity Exchanges Best PracticesDokument18 SeitenCommodity Exchanges Best PracticesoriontherecluseNoch keine Bewertungen

- Major Project ReportDokument76 SeitenMajor Project Reportrahulrawat02Noch keine Bewertungen

- Final ProspectusDokument106 SeitenFinal ProspectusAhsan Iftikhar QureshiNoch keine Bewertungen

- Convertible Note Financing Term SheetDokument2 SeitenConvertible Note Financing Term Sheet4natomas100% (1)

- Iron Condor Vs Steady Condor - How We Trade OptionsDokument12 SeitenIron Condor Vs Steady Condor - How We Trade Optionsbarkha raniNoch keine Bewertungen

- Structured Finance in IndiaDokument7 SeitenStructured Finance in Indiaanjali_parekh37Noch keine Bewertungen

- Goldsep0314review DundeeDokument19 SeitenGoldsep0314review Dundeelodstar33Noch keine Bewertungen

- Spitzer IndictmentDokument32 SeitenSpitzer Indictmentjmaglich1Noch keine Bewertungen

- Nism Doce Training Module: HR - L & D Team, HDFC BankDokument213 SeitenNism Doce Training Module: HR - L & D Team, HDFC BankPrem PrakashNoch keine Bewertungen

- A Mini Project On SapmDokument28 SeitenA Mini Project On SapmPraveen KumarNoch keine Bewertungen

- Outlook Task2Dokument79 SeitenOutlook Task2Rajveer singh PariharNoch keine Bewertungen

- BankingDokument19 SeitenBankingTipu SultanNoch keine Bewertungen

- 4.FIM-Module IV-Spot Market and Future MarketDokument21 Seiten4.FIM-Module IV-Spot Market and Future MarketAmarendra PattnaikNoch keine Bewertungen

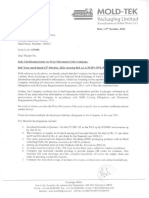

- Mold-Tek: Packaging LimitedDokument2 SeitenMold-Tek: Packaging LimitedKeigan ChatterjeeNoch keine Bewertungen

- ISJ009Dokument100 SeitenISJ0092imediaNoch keine Bewertungen

- What Is Currency ConvertibilityDokument8 SeitenWhat Is Currency Convertibilitybrahmesh_raoNoch keine Bewertungen

- ReadingthemarketDokument66 SeitenReadingthemarketMugavaiselvam Govindaraj100% (16)

- FTIL Annual Report 2009Dokument180 SeitenFTIL Annual Report 2009Alwyn FurtadoNoch keine Bewertungen

- 2010 - 05 ProspectusDokument293 Seiten2010 - 05 ProspectusPak DefanceNoch keine Bewertungen

- 2016-2017-IBL Finals NotesDokument35 Seiten2016-2017-IBL Finals Noteslaw abad raNoch keine Bewertungen

- Bajaj Finserve Limited: Quarterly Result UpdateDokument2 SeitenBajaj Finserve Limited: Quarterly Result UpdateSagar JainNoch keine Bewertungen

- Apollo HealthDokument542 SeitenApollo HealthabulaskarNoch keine Bewertungen

- AssignmentDokument13 SeitenAssignmentabdur RahmanNoch keine Bewertungen

- FTSE 100 Index FactsheetDokument2 SeitenFTSE 100 Index FactsheetGaurang GuptaNoch keine Bewertungen

- Literature ReviewDokument8 SeitenLiterature ReviewAshi GargNoch keine Bewertungen

- Securities and Exchange Commission (SEC) - Form11-KDokument2 SeitenSecurities and Exchange Commission (SEC) - Form11-Khighfinance100% (1)

- BCL Swift User GuideDokument191 SeitenBCL Swift User GuideM.Medina100% (1)

- Sample Test Chap04Dokument9 SeitenSample Test Chap04Niamul HasanNoch keine Bewertungen