Das könnte Ihnen auch gefallen

- Carbon Accounting in IndiaDokument2 SeitenCarbon Accounting in IndiaPrramakrishnanRamaKrishnanNoch keine Bewertungen

- Unique Share Management LTD.: Chart of AccountsDokument34 SeitenUnique Share Management LTD.: Chart of AccountsFarida YesminNoch keine Bewertungen

- SAP ConsolidationDokument110 SeitenSAP Consolidationnanduri.aparna161Noch keine Bewertungen

- Operation MGT Practice QuestionDokument60 SeitenOperation MGT Practice Questionmalik92305Noch keine Bewertungen

- Accounting TheoryDokument38 SeitenAccounting Theoryomar waheedNoch keine Bewertungen

- Final Account With AnswersDokument23 SeitenFinal Account With Answerskunjap0% (1)

- RFP For Jet Airways v2Dokument17 SeitenRFP For Jet Airways v2rahulalwayzzNoch keine Bewertungen

- Synovus Statement JulDokument2 SeitenSynovus Statement JulВалентина Швечикова100% (1)

- Steel IndustryDokument31 SeitenSteel IndustrypracashNoch keine Bewertungen

- Accounting Theory Approach PDFDokument104 SeitenAccounting Theory Approach PDFabiyya salsabilNoch keine Bewertungen

- CHP 02 Accounting Theory JADokument35 SeitenCHP 02 Accounting Theory JAShekh Rakin MosharrofNoch keine Bewertungen

- Journal of Medical Marketing - Device, Diagnostic and Pharmaceutical Marketing-2006-Appelt-195-202Dokument8 SeitenJournal of Medical Marketing - Device, Diagnostic and Pharmaceutical Marketing-2006-Appelt-195-202Sumanth KolliNoch keine Bewertungen

- Ethical Problem of OutsourcingDokument2 SeitenEthical Problem of OutsourcingVũ RainNoch keine Bewertungen

- SCM Notes Sunil ChopraDokument9 SeitenSCM Notes Sunil ChopraRohit singhNoch keine Bewertungen

- BP Case StudyDokument4 SeitenBP Case StudyLaxmiNoch keine Bewertungen

- Qadri Group PDFDokument19 SeitenQadri Group PDFAhmed NiazNoch keine Bewertungen

- Chen - Yu - Market Entry Strategy in AsiaDokument10 SeitenChen - Yu - Market Entry Strategy in Asiasalmansince86Noch keine Bewertungen

- Marita Smith Case StudyDokument5 SeitenMarita Smith Case StudyPremnath jayaprakashNoch keine Bewertungen

- Open InnovationDokument5 SeitenOpen InnovationBerthaNoch keine Bewertungen

- Axiatavsmaxis 150701063457 Lva1 App6892Dokument26 SeitenAxiatavsmaxis 150701063457 Lva1 App6892Raj DubeyNoch keine Bewertungen

- De Vera - Johnson PharmaceuticalsDokument2 SeitenDe Vera - Johnson PharmaceuticalsJųpiter De VeraNoch keine Bewertungen

- Principles of StrategyDokument15 SeitenPrinciples of StrategysanazhNoch keine Bewertungen

- VODafoneDokument46 SeitenVODafoneAshish Sah100% (1)

- 2A12 - Christabella Chiquita - Individual Assigment Marketing ManagementDokument7 Seiten2A12 - Christabella Chiquita - Individual Assigment Marketing ManagementChristabella ChiquitaNoch keine Bewertungen

- Business Environment PESTLE ANALYSISDokument19 SeitenBusiness Environment PESTLE ANALYSISAbhay GuptaNoch keine Bewertungen

- Case 15 Savola GroupDokument21 SeitenCase 15 Savola GroupKad Saad50% (2)

- A Critical Application of Strategy DichotomiesDokument5 SeitenA Critical Application of Strategy DichotomiesDerek RealeNoch keine Bewertungen

- Sexual Descrimination at Eastern AirlinesDokument4 SeitenSexual Descrimination at Eastern AirlinesMario RodriguezNoch keine Bewertungen

- Implementation of ISO 14000 in Luggage Manufacturing Industry: A Case StudyDokument14 SeitenImplementation of ISO 14000 in Luggage Manufacturing Industry: A Case StudyDevspringNoch keine Bewertungen

- Cost Leadership Term PaperDokument19 SeitenCost Leadership Term PaperNitesh ShettyNoch keine Bewertungen

- Limitations of Balance SheetDokument6 SeitenLimitations of Balance Sheetshoms_007Noch keine Bewertungen

- Marketting AssignementDokument4 SeitenMarketting Assignementmulabbi brianNoch keine Bewertungen

- Ford Motor Company: Total Quality Management: Presented By:Sahil ReyazDokument14 SeitenFord Motor Company: Total Quality Management: Presented By:Sahil ReyazYASIR IMBA21Noch keine Bewertungen

- Presented by - Abilash D Reddy Ravindar .R Sandarsh SureshDokument15 SeitenPresented by - Abilash D Reddy Ravindar .R Sandarsh SureshSandarsh SureshNoch keine Bewertungen

- Deep Change Referee ReportDokument3 SeitenDeep Change Referee ReportMadridista KroosNoch keine Bewertungen

- Assignment 1 - Marketing ManagementDokument9 SeitenAssignment 1 - Marketing Managementwidi tigustiNoch keine Bewertungen

- Avari Group: Organizational Values and Crisis LeadershipDokument6 SeitenAvari Group: Organizational Values and Crisis LeadershipAhmar ChNoch keine Bewertungen

- Summer Intership - HOmework - The Ordinary Heroes of The Taj Hotel Rohit Deshpande at TEDxNewEnglandDokument11 SeitenSummer Intership - HOmework - The Ordinary Heroes of The Taj Hotel Rohit Deshpande at TEDxNewEnglandgirish_gupta509575100% (1)

- Models of InternationaisationDokument8 SeitenModels of InternationaisationShreyas RautNoch keine Bewertungen

- 04.CNOOC Engages With Canadian Stakeholders PDFDokument14 Seiten04.CNOOC Engages With Canadian Stakeholders PDFAdilNoch keine Bewertungen

- Louis Vuitton - Final SlidesDokument32 SeitenLouis Vuitton - Final SlideszeeshanNoch keine Bewertungen

- Kim, W. C., & Mauborgne, R. (2005) - How To Make The Competition IrrelevantDokument5 SeitenKim, W. C., & Mauborgne, R. (2005) - How To Make The Competition IrrelevantCarlos FuentesNoch keine Bewertungen

- FACTS OF CASE EnronDokument8 SeitenFACTS OF CASE EnronChincel G. ANINoch keine Bewertungen

- Commercial Aviation Industry Suppliers Conference: Speednews 28Th AnnualDokument1 SeiteCommercial Aviation Industry Suppliers Conference: Speednews 28Th Annuala_sharafiehNoch keine Bewertungen

- Case Study Newland Medical TechnologiesDokument5 SeitenCase Study Newland Medical TechnologiesAbanise Orojo100% (1)

- Strategic Planning and ImplementationDokument12 SeitenStrategic Planning and ImplementationShiva LKLNoch keine Bewertungen

- Assignment On Shell LogisticsDokument7 SeitenAssignment On Shell LogisticsAravind Sethumadhavan100% (1)

- Daimler ChryslerDokument2 SeitenDaimler ChryslerRaghav Rohila100% (1)

- Global Supply Chain Assignment 1Dokument3 SeitenGlobal Supply Chain Assignment 1Neha204Noch keine Bewertungen

- HR ProjectDokument20 SeitenHR ProjectKrishna MoorthyNoch keine Bewertungen

- Expansion Strategy For Spirit Airlines - Yesenia AlvarezDokument88 SeitenExpansion Strategy For Spirit Airlines - Yesenia Alvarezyesse411jecmNoch keine Bewertungen

- The Strategic Radar Model-Business EthicsDokument5 SeitenThe Strategic Radar Model-Business EthicsNjorogeNoch keine Bewertungen

- BiovailCorporation CaseDokument8 SeitenBiovailCorporation Caseaaa__sNoch keine Bewertungen

- ReportDokument8 SeitenReportale_antNoch keine Bewertungen

- Cae Study11Dokument9 SeitenCae Study11Srivatsav SriNoch keine Bewertungen

- Strategic AlliancesDokument15 SeitenStrategic AlliancesAli AhmadNoch keine Bewertungen

- 1.4 Research QuestionDokument66 Seiten1.4 Research QuestionAnthony Shalith FernandoNoch keine Bewertungen

- Module Wise Important Questions and AnswersDokument31 SeitenModule Wise Important Questions and AnswersViraja GuruNoch keine Bewertungen

- Cadbury Case StudyDokument3 SeitenCadbury Case Studyashish4485Noch keine Bewertungen

- Ansoff's Product-Market Expansion GridDokument5 SeitenAnsoff's Product-Market Expansion GridPravinsinh Attarde100% (1)

- Case Format ProcterDokument6 SeitenCase Format Procterlovelysweet_gaby100% (1)

- Aviation and Climate Change IATADokument2 SeitenAviation and Climate Change IATAChinmai Hemani100% (1)

- What Is A TheoryDokument6 SeitenWhat Is A TheoryChoiLi_Ang_7602Noch keine Bewertungen

- Topic 8-Power PoliticsDokument19 SeitenTopic 8-Power PoliticsHema DarshiniNoch keine Bewertungen

- ICS (D) Alpha (Group 4)Dokument17 SeitenICS (D) Alpha (Group 4)Hema DarshiniNoch keine Bewertungen

- Chapter 5 - Capital AllowancesDokument14 SeitenChapter 5 - Capital AllowancesHema DarshiniNoch keine Bewertungen

- Sime Darby Plantation 2019 Annual Report PDFDokument404 SeitenSime Darby Plantation 2019 Annual Report PDFHema DarshiniNoch keine Bewertungen

- Cost FullDokument352 SeitenCost FullRao RehanNoch keine Bewertungen

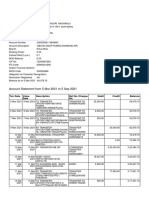

- 5 Mar 2021 To 5 Sep 2021Dokument13 Seiten5 Mar 2021 To 5 Sep 2021KanakaReddyKannaNoch keine Bewertungen

- Competency Appraisal UM Digos (PARTNERSHIP)Dokument10 SeitenCompetency Appraisal UM Digos (PARTNERSHIP)Diana Faye CaduadaNoch keine Bewertungen

- Accounting in Business: Lecture 1 & 2Dokument42 SeitenAccounting in Business: Lecture 1 & 2Noraishah IsmailNoch keine Bewertungen

- Q&a CfasDokument16 SeitenQ&a CfasRyan Malanum AbrioNoch keine Bewertungen

- Chapter 3 - The Adjusting ProcessDokument55 SeitenChapter 3 - The Adjusting ProcessfitrieyfieyNoch keine Bewertungen

- Suggested Answer - Syl12 - Dec13 - Paper 12 Intermediate ExaminationDokument23 SeitenSuggested Answer - Syl12 - Dec13 - Paper 12 Intermediate ExaminationsmrndrdasNoch keine Bewertungen

- Copy - 2 - of Principles of Accounting Note Year 1Dokument213 SeitenCopy - 2 - of Principles of Accounting Note Year 1Rexford Atta-boakye JnrNoch keine Bewertungen

- Mobifin 11 1 - New - 7Dokument65 SeitenMobifin 11 1 - New - 7amittsaxenaNoch keine Bewertungen

- Amalgamation of CompaniesDokument40 SeitenAmalgamation of CompaniesalexanderNoch keine Bewertungen

- Rus Form 7Dokument8 SeitenRus Form 7joneeazucenaNoch keine Bewertungen

- Midterm ExamDokument25 SeitenMidterm Examarnel buanNoch keine Bewertungen

- Audit of Cash and Cash EquivalentsDokument2 SeitenAudit of Cash and Cash EquivalentsJhedz Cartas0% (1)

- Lead ScheduleDokument23 SeitenLead SchedulesjNoch keine Bewertungen

- FAC MCQs UnitwiseDokument7 SeitenFAC MCQs UnitwiseSamNoch keine Bewertungen

- Intro To Accounting - One Credit Assignment ContdDokument8 SeitenIntro To Accounting - One Credit Assignment Contdapi-342895963Noch keine Bewertungen

- Accounting 7th Edition Horngren Solutions ManualDokument35 SeitenAccounting 7th Edition Horngren Solutions Manualmellow.duncical.v9vuq100% (14)

- ACC 6050 Milestone 1 FinalDokument14 SeitenACC 6050 Milestone 1 FinalvertmeddNoch keine Bewertungen

- Intermediate Accounting NotesDokument7 SeitenIntermediate Accounting NotesKyle Angela IlanNoch keine Bewertungen

- Aarambh 2024: Half Yearly Test 2023 Time Allowed: 3 Hours Total Marks 80 Accountancy General InstructionsDokument5 SeitenAarambh 2024: Half Yearly Test 2023 Time Allowed: 3 Hours Total Marks 80 Accountancy General InstructionsPranjal GuptaNoch keine Bewertungen

- Answer Key Chapter 3Dokument60 SeitenAnswer Key Chapter 3HectorNoch keine Bewertungen

- CBSE Class 11 Accounting-Vouchers and Their Preparation PDFDokument13 SeitenCBSE Class 11 Accounting-Vouchers and Their Preparation PDFDiksha60% (5)

- Tutorial Letter 202/2/2014: Selected Accounting Standards and Simple Group StructuresDokument11 SeitenTutorial Letter 202/2/2014: Selected Accounting Standards and Simple Group StructuresJerome ChettyNoch keine Bewertungen

- Introductory Financial Accounting For Business 2Nd Edition Mark A Edmonds Full ChapterDokument67 SeitenIntroductory Financial Accounting For Business 2Nd Edition Mark A Edmonds Full Chapterelisha.gardner158100% (5)

- Investment AccountsDokument10 SeitenInvestment AccountsMani kandan.GNoch keine Bewertungen

- Answers For The ActivityDokument36 SeitenAnswers For The ActivityLakshyaNoch keine Bewertungen