Das könnte Ihnen auch gefallen

- BLS18234 BRO Book 006.1 CH5Dokument20 SeitenBLS18234 BRO Book 006.1 CH5G.D SinghNoch keine Bewertungen

- Design Informed: Driving Innovation with Evidence-Based DesignVon EverandDesign Informed: Driving Innovation with Evidence-Based DesignNoch keine Bewertungen

- 7 Entrepreneurial Leadership Workouts: A Guide to Developing Entrepreneurial Leadership in TeamsVon Everand7 Entrepreneurial Leadership Workouts: A Guide to Developing Entrepreneurial Leadership in TeamsNoch keine Bewertungen

- Food and Sustainability in the Twenty-First Century: Cross-Disciplinary PerspectivesVon EverandFood and Sustainability in the Twenty-First Century: Cross-Disciplinary PerspectivesPaul CollinsonNoch keine Bewertungen

- Winning the Global Game: A Strategy for Linking People and ProfitsVon EverandWinning the Global Game: A Strategy for Linking People and ProfitsNoch keine Bewertungen

- What Every Social Entrepreneur Needs to Know About InvestorsVon EverandWhat Every Social Entrepreneur Needs to Know About InvestorsNoch keine Bewertungen

- Fire in the Machine: Driving Entrepreneurial Innovation in Large CPG OrganizationsVon EverandFire in the Machine: Driving Entrepreneurial Innovation in Large CPG OrganizationsNoch keine Bewertungen

- Network Advantage: How to Unlock Value From Your Alliances and PartnershipsVon EverandNetwork Advantage: How to Unlock Value From Your Alliances and PartnershipsNoch keine Bewertungen

- The Flourishing Community: A Story of Hope for America's Distressed PlacesVon EverandThe Flourishing Community: A Story of Hope for America's Distressed PlacesNoch keine Bewertungen

- Strategic Managing in a Turbulent World: Learning to Make Your Organization Future-proofVon EverandStrategic Managing in a Turbulent World: Learning to Make Your Organization Future-proofBewertung: 4 von 5 Sternen4/5 (1)

- Ecosystem Edge: Sustaining Competitiveness in the Face of DisruptionVon EverandEcosystem Edge: Sustaining Competitiveness in the Face of DisruptionNoch keine Bewertungen

- VISION: Our Strategic Infrastructure Roadmap ForwardVon EverandVISION: Our Strategic Infrastructure Roadmap ForwardNoch keine Bewertungen

- Waiting on Retirement: Aging and Economic Insecurity in Low-Wage WorkVon EverandWaiting on Retirement: Aging and Economic Insecurity in Low-Wage WorkNoch keine Bewertungen

- Turning the Pyramid Upside Down: A New Leadership ModelVon EverandTurning the Pyramid Upside Down: A New Leadership ModelNoch keine Bewertungen

- The New Builders: Face to Face With the True Future of BusinessVon EverandThe New Builders: Face to Face With the True Future of BusinessNoch keine Bewertungen

- Evasive Entrepreneurs and the Future of Governance: How Innovation Improves Economies and GovernmentsVon EverandEvasive Entrepreneurs and the Future of Governance: How Innovation Improves Economies and GovernmentsNoch keine Bewertungen

- 1. Uncovering the Treasures of Africa: A Guide to Documenting Indigenous Knowledge Management: 1Von Everand1. Uncovering the Treasures of Africa: A Guide to Documenting Indigenous Knowledge Management: 1Bewertung: 5 von 5 Sternen5/5 (1)

- Social Project Management A Complete Guide - 2020 EditionVon EverandSocial Project Management A Complete Guide - 2020 EditionNoch keine Bewertungen

- Achieving Post-Merger Success: A Stakeholder's Guide to Cultural Due Diligence, Assessment, and IntegrationVon EverandAchieving Post-Merger Success: A Stakeholder's Guide to Cultural Due Diligence, Assessment, and IntegrationNoch keine Bewertungen

- Welcome to the Urban Revolution: How Cities Are Changing the WorldVon EverandWelcome to the Urban Revolution: How Cities Are Changing the WorldBewertung: 4 von 5 Sternen4/5 (7)

- Broadbandits: Inside the $750 Billion Telecom HeistVon EverandBroadbandits: Inside the $750 Billion Telecom HeistBewertung: 2.5 von 5 Sternen2.5/5 (4)

- Three Revolutions: Steering Automated, Shared, and Electric Vehicles to a Better FutureVon EverandThree Revolutions: Steering Automated, Shared, and Electric Vehicles to a Better FutureNoch keine Bewertungen

- Our Day to End Poverty: 24 Ways You Can Make a DifferenceVon EverandOur Day to End Poverty: 24 Ways You Can Make a DifferenceBewertung: 3 von 5 Sternen3/5 (1)

- Leap 4.0. African Perspectives on the Fourth Industrial Revolution: African Perspectives on the Fourth Industrial RevolutionVon EverandLeap 4.0. African Perspectives on the Fourth Industrial Revolution: African Perspectives on the Fourth Industrial RevolutionNoch keine Bewertungen

- The Small-Mart Revolution: How Local Businesses Are Beating the Global CompetitionVon EverandThe Small-Mart Revolution: How Local Businesses Are Beating the Global CompetitionBewertung: 4 von 5 Sternen4/5 (1)

- The Next Level: Breakthrough Performance Anchored by FaithVon EverandThe Next Level: Breakthrough Performance Anchored by FaithNoch keine Bewertungen

- Trading Down: Africa, Value Chains, And The Global EconomyVon EverandTrading Down: Africa, Value Chains, And The Global EconomyNoch keine Bewertungen

- Service Science, Management, and Engineering:: Theory and ApplicationsVon EverandService Science, Management, and Engineering:: Theory and ApplicationsNoch keine Bewertungen

- Flowcasting | See Your Money Future Clearly Today | Change It Now for a Better Tomorrow | The Must-Have Money Management, Planning, Budgeting, Mapping Tool and Practical Skill to Succeed Financially.Von EverandFlowcasting | See Your Money Future Clearly Today | Change It Now for a Better Tomorrow | The Must-Have Money Management, Planning, Budgeting, Mapping Tool and Practical Skill to Succeed Financially.Noch keine Bewertungen

- The Orange Code: How ING Direct Succeeded by Being a Rebel with a CauseVon EverandThe Orange Code: How ING Direct Succeeded by Being a Rebel with a CauseBewertung: 2 von 5 Sternen2/5 (1)

- Groupthink Versus High-Quality Decision Making in International RelationsVon EverandGroupthink Versus High-Quality Decision Making in International RelationsNoch keine Bewertungen

- Monthly Subscription Business Model A Complete Guide - 2020 EditionVon EverandMonthly Subscription Business Model A Complete Guide - 2020 EditionNoch keine Bewertungen

- Sprawl Costs: Economic Impacts of Unchecked DevelopmentVon EverandSprawl Costs: Economic Impacts of Unchecked DevelopmentBewertung: 3.5 von 5 Sternen3.5/5 (1)

- What Can We Do?: Practical Ways Your Youth Ministry Can Have a Global ConscienceVon EverandWhat Can We Do?: Practical Ways Your Youth Ministry Can Have a Global ConscienceBewertung: 0.5 von 5 Sternen0.5/5 (1)

- Software Product Management: Finding the Right Balance for YourProduct Inc.Von EverandSoftware Product Management: Finding the Right Balance for YourProduct Inc.Noch keine Bewertungen

- The Technologized Investor: Innovation through ReorientationVon EverandThe Technologized Investor: Innovation through ReorientationNoch keine Bewertungen

- Preparing For The Future Of Work, Education, EconomyVon EverandPreparing For The Future Of Work, Education, EconomyNoch keine Bewertungen

- Workforce development A Clear and Concise ReferenceVon EverandWorkforce development A Clear and Concise ReferenceNoch keine Bewertungen

- Leading for the Long Term: European Real Estate Executives on Leadership and ManagementVon EverandLeading for the Long Term: European Real Estate Executives on Leadership and ManagementNoch keine Bewertungen

- Adventure Finance: How to Create a Funding Journey That Blends Profit and PurposeVon EverandAdventure Finance: How to Create a Funding Journey That Blends Profit and PurposeNoch keine Bewertungen

- Solution Nation: One Nation is Disproportionately Responding to the World's Most Intractable ProblemsVon EverandSolution Nation: One Nation is Disproportionately Responding to the World's Most Intractable ProblemsNoch keine Bewertungen

- A Rising Tide: Financing Strategies for Women-Owned FirmsVon EverandA Rising Tide: Financing Strategies for Women-Owned FirmsNoch keine Bewertungen

- The Business Solution to Poverty: Designing Products and Services for Three Billion New CustomersVon EverandThe Business Solution to Poverty: Designing Products and Services for Three Billion New CustomersNoch keine Bewertungen

- Living Diversity – Shaping Society: The Opportunities and Challenges Posed by Cultural Difference in GermanyVon EverandLiving Diversity – Shaping Society: The Opportunities and Challenges Posed by Cultural Difference in GermanyNoch keine Bewertungen

- The Invention of Enterprise: Entrepreneurship from Ancient Mesopotamia to Modern TimesVon EverandThe Invention of Enterprise: Entrepreneurship from Ancient Mesopotamia to Modern TimesNoch keine Bewertungen

- Open Data Now: The Secret to Hot Startups, Smart Investing, Savvy Marketing, and Fast InnovationVon EverandOpen Data Now: The Secret to Hot Startups, Smart Investing, Savvy Marketing, and Fast InnovationBewertung: 3 von 5 Sternen3/5 (4)

- Building Wealth through Venture Capital: A Practical Guide for Investors and the Entrepreneurs They FundVon EverandBuilding Wealth through Venture Capital: A Practical Guide for Investors and the Entrepreneurs They FundNoch keine Bewertungen

- Planet VC: How the globalization of venture capital is driving the next wave of innovationVon EverandPlanet VC: How the globalization of venture capital is driving the next wave of innovationNoch keine Bewertungen

- Subscription Models A Complete Guide - 2019 EditionVon EverandSubscription Models A Complete Guide - 2019 EditionNoch keine Bewertungen

- Transnational Land Grabs and Restitution in an Age of the (De-)Militarised New Scramble for Africa: A Pan African Socio-Legal: A Pan African Socio-Legal PerspectiveVon EverandTransnational Land Grabs and Restitution in an Age of the (De-)Militarised New Scramble for Africa: A Pan African Socio-Legal: A Pan African Socio-Legal PerspectiveNoch keine Bewertungen

- Decision Intelligence A Complete Guide - 2020 EditionVon EverandDecision Intelligence A Complete Guide - 2020 EditionNoch keine Bewertungen

- Business Chemistry: PioneerDokument2 SeitenBusiness Chemistry: PioneerngrckrNoch keine Bewertungen

- Testing For NormalityDokument12 SeitenTesting For NormalityRavikanth ReddyNoch keine Bewertungen

- Ferguson's Formula: by Anita Elberse & Sir Alex Ferguson Harvard Business Review October 2013Dokument7 SeitenFerguson's Formula: by Anita Elberse & Sir Alex Ferguson Harvard Business Review October 2013Ravikanth ReddyNoch keine Bewertungen

- OutliersDokument7 SeitenOutliersRavikanth ReddyNoch keine Bewertungen

- Presentation On Unit 2Dokument13 SeitenPresentation On Unit 2Ravikanth ReddyNoch keine Bewertungen

- The Art of Giving and Receiving AdviceDokument7 SeitenThe Art of Giving and Receiving AdviceRavikanth ReddyNoch keine Bewertungen

- Chapter 12 Network DesignDokument10 SeitenChapter 12 Network DesignRavikanth ReddyNoch keine Bewertungen

- Covid Presentation: Darshan Reddy Vadamala Class: VA Roll No. 11Dokument9 SeitenCovid Presentation: Darshan Reddy Vadamala Class: VA Roll No. 11Ravikanth ReddyNoch keine Bewertungen

- Making Exit Interviews CountDokument15 SeitenMaking Exit Interviews CountRavikanth ReddyNoch keine Bewertungen

- Where Financial Reporting Still Falls ShortDokument8 SeitenWhere Financial Reporting Still Falls ShortRavikanth ReddyNoch keine Bewertungen

- Chapter 11 Global Supply ChainsDokument11 SeitenChapter 11 Global Supply ChainsRavikanth ReddyNoch keine Bewertungen

- Addiction For Growth RetailDokument25 SeitenAddiction For Growth RetailRavikanth ReddyNoch keine Bewertungen

- The Truth About BlockchainDokument9 SeitenThe Truth About BlockchainRavikanth ReddyNoch keine Bewertungen

- How The Growth Outliers Do ItDokument7 SeitenHow The Growth Outliers Do ItRavikanth ReddyNoch keine Bewertungen

- Gold Import DataDokument3 SeitenGold Import DataRavikanth ReddyNoch keine Bewertungen

- Where Financial Reporting Still Falls ShortDokument8 SeitenWhere Financial Reporting Still Falls ShortRavikanth ReddyNoch keine Bewertungen

- Right Technolgy, Wrong TimeDokument11 SeitenRight Technolgy, Wrong TimeRavikanth ReddyNoch keine Bewertungen

- We Are Like That OnlyDokument1 SeiteWe Are Like That OnlyRavikanth ReddyNoch keine Bewertungen

- The Impact of Celebrity Endorsement AdveDokument92 SeitenThe Impact of Celebrity Endorsement AdveRavikanth ReddyNoch keine Bewertungen

- SCHEDULE For Second PhaseDokument1 SeiteSCHEDULE For Second PhaseRavikanth ReddyNoch keine Bewertungen

- Darshan AssignmentDokument5 SeitenDarshan AssignmentRavikanth ReddyNoch keine Bewertungen

- CB5E45903BDokument1 SeiteCB5E45903Bkrish tcrNoch keine Bewertungen

- The Electricity Development of Small Power Projects Rules 2020 GN 491Dokument85 SeitenThe Electricity Development of Small Power Projects Rules 2020 GN 491Matojo CosattaNoch keine Bewertungen

- Entrep Q2 SLM Lesson-1Dokument12 SeitenEntrep Q2 SLM Lesson-1akiqt68Noch keine Bewertungen

- Allocation and Apportionment and Job and Batch Costing Worked Example Question 2Dokument2 SeitenAllocation and Apportionment and Job and Batch Costing Worked Example Question 2Roshan RamkhalawonNoch keine Bewertungen

- 2019 ZBDokument5 Seiten2019 ZBChandani FernandoNoch keine Bewertungen

- Role of DFHI in Money MarketDokument13 SeitenRole of DFHI in Money Marketmanishg_17100% (1)

- AKD - Good Day Service CompanyDokument9 SeitenAKD - Good Day Service CompanyPuspita SariNoch keine Bewertungen

- Meaning of WTO: WTO - World Trade OrganisationDokument13 SeitenMeaning of WTO: WTO - World Trade OrganisationMehak joshiNoch keine Bewertungen

- Assure9 - Teerth Technospace PDFDokument17 SeitenAssure9 - Teerth Technospace PDFneoavi7Noch keine Bewertungen

- Consent Form-IDFC Buy Back - Tranche 2 - 2010-11Dokument1 SeiteConsent Form-IDFC Buy Back - Tranche 2 - 2010-11tkchauhan1Noch keine Bewertungen

- Masterlist - Course - Offerings - 2024 (As at 18 July 2023)Dokument3 SeitenMasterlist - Course - Offerings - 2024 (As at 18 July 2023)limyihang17Noch keine Bewertungen

- Central Bank of The PhilippinesDokument5 SeitenCentral Bank of The PhilippinesBERNALDEZ NESCEL JOYNoch keine Bewertungen

- ACCOUNTING 3B Homework 3Dokument3 SeitenACCOUNTING 3B Homework 3Jasmin Escaño100% (1)

- Individual-Asm3 Pham-Chung ss181258Dokument3 SeitenIndividual-Asm3 Pham-Chung ss181258hoantkss181354Noch keine Bewertungen

- BBA-305 Cost & Management AccountingDokument57 SeitenBBA-305 Cost & Management Accountingstarkol.c2023112971Noch keine Bewertungen

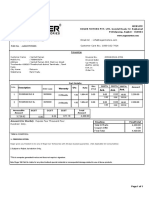

- As Per Request 30 Days: QuotationDokument2 SeitenAs Per Request 30 Days: QuotationAdmin SAF PrintersNoch keine Bewertungen

- Credit Denial, Request For InformationDokument2 SeitenCredit Denial, Request For InformationAzmy67% (3)

- Executive Summery: Page - 1Dokument7 SeitenExecutive Summery: Page - 1Ahsan Habib JimonNoch keine Bewertungen

- TUTORIAL SOLUTIONS (Week 4A)Dokument8 SeitenTUTORIAL SOLUTIONS (Week 4A)Peter100% (1)

- PFF108 LoyaltyCardPlusApplicationForm V06Dokument2 SeitenPFF108 LoyaltyCardPlusApplicationForm V06Aiza BananNoch keine Bewertungen

- Topic 1 - Introduction of Production and Operation ManagementDokument16 SeitenTopic 1 - Introduction of Production and Operation ManagementTanisha SarafNoch keine Bewertungen

- Zeeshan Updated ResumeDokument4 SeitenZeeshan Updated ResumeannajarushaNoch keine Bewertungen

- Assets Liabilities and EquityDokument2 SeitenAssets Liabilities and EquityArian Amurao50% (2)

- Ing, Q'Ty, Price:: Say: Us Dollars Two Thousand Three Hundred Seventhy One OnlyDokument1 SeiteIng, Q'Ty, Price:: Say: Us Dollars Two Thousand Three Hundred Seventhy One OnlyNi Komang Ayu Cahya Puja DewiNoch keine Bewertungen

- Book 1Dokument6 SeitenBook 1Naveen BishtNoch keine Bewertungen

- Fundamentals of Taxation 2017 Edition 10Th Edition Cruz Solutions Manual Full Chapter PDFDokument47 SeitenFundamentals of Taxation 2017 Edition 10Th Edition Cruz Solutions Manual Full Chapter PDFmarushiapatrina100% (13)

- JIT QuestionnaireDokument3 SeitenJIT QuestionnaireMARIA VERNADETTE SHARISSE LEGASPINoch keine Bewertungen

- A Seminar Report On Management of SupplyDokument25 SeitenA Seminar Report On Management of SupplyRijana ShresthaNoch keine Bewertungen

- ESPI Report 77 - NEWSPACE ASIA - Final - ProofDokument130 SeitenESPI Report 77 - NEWSPACE ASIA - Final - Proofharwani3Noch keine Bewertungen

- Promissory Note Annex ADokument2 SeitenPromissory Note Annex ACarol Ledesma Yap-PelaezNoch keine Bewertungen