Das könnte Ihnen auch gefallen

- Gen. Principles of TaxationDokument22 SeitenGen. Principles of TaxationPageduesca RouelNoch keine Bewertungen

- General Principles of Taxation: Tax 111 - Income Taxation Ferdinand C. Importado Cpa, MbaDokument22 SeitenGeneral Principles of Taxation: Tax 111 - Income Taxation Ferdinand C. Importado Cpa, Mbaangelo_maranan100% (1)

- Topic-1-An Overview of TaxationDokument29 SeitenTopic-1-An Overview of TaxationJaved AnwarNoch keine Bewertungen

- Topic-1-An Overview of TaxationDokument29 SeitenTopic-1-An Overview of TaxationJaved AnwarNoch keine Bewertungen

- What Is 'Taxation': Estate Taxes TaxesDokument2 SeitenWhat Is 'Taxation': Estate Taxes TaxesRandy DonatoNoch keine Bewertungen

- Income Taxation 1Dokument86 SeitenIncome Taxation 1guerradhonaelizaNoch keine Bewertungen

- Chapter 1 Introduction To TaxationDokument21 SeitenChapter 1 Introduction To TaxationErica FlorentinoNoch keine Bewertungen

- Principles of TaxationDokument51 SeitenPrinciples of TaxationAlvigrace PuguonNoch keine Bewertungen

- Taxation: Basic Concepts and PrinciplesDokument47 SeitenTaxation: Basic Concepts and PrinciplesMaybelleNoch keine Bewertungen

- Lesson 14 ABM161 Taxation For FinalsDokument41 SeitenLesson 14 ABM161 Taxation For FinalsNorhaliza D. SaripNoch keine Bewertungen

- Lecture-1-An Overview of TaxationDokument14 SeitenLecture-1-An Overview of TaxationJaved AnwarNoch keine Bewertungen

- Module 3 General Principles of TaxationDokument80 SeitenModule 3 General Principles of TaxationFlameNoch keine Bewertungen

- BA122 SummaryDokument6 SeitenBA122 SummaryJaiavave LinogonNoch keine Bewertungen

- Unit-I Taxation by Prof. Anbalagan ChinniahDokument23 SeitenUnit-I Taxation by Prof. Anbalagan ChinniahProf. Dr. Anbalagan ChinniahNoch keine Bewertungen

- CLWTAXN General Principles of Taxation Part OneDokument46 SeitenCLWTAXN General Principles of Taxation Part Oneclassic swagNoch keine Bewertungen

- Acfrogc9mb7nlbmkbcfuonpkva Vyrnoeit6djnpfc7lg6tcqzyu5ol816zlfbcl1raopr4fsadz2whfjxvv9nnopz-Lpheunvkzhneewx05ytz Fube13x36w Uybxnqntbje9wv-VkaanvllqmDokument48 SeitenAcfrogc9mb7nlbmkbcfuonpkva Vyrnoeit6djnpfc7lg6tcqzyu5ol816zlfbcl1raopr4fsadz2whfjxvv9nnopz-Lpheunvkzhneewx05ytz Fube13x36w Uybxnqntbje9wv-VkaanvllqmCrystal MaeNoch keine Bewertungen

- Topic 3 Canons of TaxationDokument20 SeitenTopic 3 Canons of TaxationJaved AnwarNoch keine Bewertungen

- Part I. Chapter 1 Fundamental PrinciplesDokument39 SeitenPart I. Chapter 1 Fundamental PrinciplesCatherine GomezNoch keine Bewertungen

- Quick Review On General Principles of TaxationDokument15 SeitenQuick Review On General Principles of TaxationJamesNoch keine Bewertungen

- Government Without Any Expectation of Direct Return in Benefit ". Ability To Pay. Taxed in The Same Way Without Any DiscriminationDokument42 SeitenGovernment Without Any Expectation of Direct Return in Benefit ". Ability To Pay. Taxed in The Same Way Without Any DiscriminationyebegashetNoch keine Bewertungen

- Introduction: Taxation: Anika Rafah Lecturer North South UniversityDokument15 SeitenIntroduction: Taxation: Anika Rafah Lecturer North South UniversityJarÎnAnJumChôwdhuryNoch keine Bewertungen

- Taxation Chapter 1.1 - DDokument13 SeitenTaxation Chapter 1.1 - DLelouch LevyNoch keine Bewertungen

- Income Taxation CHAPTER 1Dokument31 SeitenIncome Taxation CHAPTER 1Armalyn CangqueNoch keine Bewertungen

- Taxation in The Philippine SDokument22 SeitenTaxation in The Philippine SBJ Ambat100% (1)

- ACC2054 Malaysian Taxation System (Mar 2013) Lecture 1Dokument13 SeitenACC2054 Malaysian Taxation System (Mar 2013) Lecture 1Selva Bavani SelwaduraiNoch keine Bewertungen

- Day 3 Lecture SlidesDokument25 SeitenDay 3 Lecture SlidesyebegashetNoch keine Bewertungen

- 1 Microsoft PowerPoint PresentationDokument22 Seiten1 Microsoft PowerPoint PresentationHASNAT SABIRNoch keine Bewertungen

- ACC717 Topic 1.TAXATIONDokument29 SeitenACC717 Topic 1.TAXATIONJason MaelumaNoch keine Bewertungen

- Introduction To Taxation: (Taxes, Tax Laws and Tax Administration) by Daryl T. Evardone, CPADokument35 SeitenIntroduction To Taxation: (Taxes, Tax Laws and Tax Administration) by Daryl T. Evardone, CPAKyla Marie HubieraNoch keine Bewertungen

- General Principles On Taxation-2015Dokument40 SeitenGeneral Principles On Taxation-2015Henry M. Macatuno Jr.Noch keine Bewertungen

- Taxation General PrinciplesDokument28 SeitenTaxation General PrinciplesIzaNoch keine Bewertungen

- Topic 1-Income Taxation With ExplanationDokument50 SeitenTopic 1-Income Taxation With ExplanationJewel ClairNoch keine Bewertungen

- TaxationDokument18 SeitenTaxationMatthew MadriagaNoch keine Bewertungen

- Week1-Local TaxationDokument20 SeitenWeek1-Local TaxationShanique WilliamsNoch keine Bewertungen

- Sources of Revenues of Local Government Units Sources of Revenues of Local Government UnitsDokument73 SeitenSources of Revenues of Local Government Units Sources of Revenues of Local Government Unitsaige mascodNoch keine Bewertungen

- 3 Chapter03Dokument79 Seiten3 Chapter03Kalkidan ZerihunNoch keine Bewertungen

- Lecture Notes - PEconomics IIDokument112 SeitenLecture Notes - PEconomics IIAmelia BaileyNoch keine Bewertungen

- Taxation PDFDokument55 SeitenTaxation PDFFatimaNoch keine Bewertungen

- Lecture 2 - Taxation and Public SpendingDokument34 SeitenLecture 2 - Taxation and Public SpendingAmelia BaileyNoch keine Bewertungen

- Lec 9 Fiscal Policy TaxationDokument36 SeitenLec 9 Fiscal Policy Taxationdua tanveerNoch keine Bewertungen

- Taxation LawDokument106 SeitenTaxation Lawjohnanthony201Noch keine Bewertungen

- Taxation: General PrinciplesDokument30 SeitenTaxation: General PrinciplesJao FloresNoch keine Bewertungen

- Tax Planning and Management TaxDokument5 SeitenTax Planning and Management TaxHarsha HarshaNoch keine Bewertungen

- Chapter - Two: Meaning and Characteristics of TaxationDokument61 SeitenChapter - Two: Meaning and Characteristics of TaxationYoseph KassaNoch keine Bewertungen

- LEAP Acc110 Income Taxation CREATE Module 1 and 2Dokument12 SeitenLEAP Acc110 Income Taxation CREATE Module 1 and 2Ella Blanca BuyaNoch keine Bewertungen

- General Principles of TaxationDokument26 SeitenGeneral Principles of TaxationjoetapsNoch keine Bewertungen

- Bintaxa ReadingsDokument9 SeitenBintaxa ReadingsAlex GonzalesNoch keine Bewertungen

- Taxation TheoryDokument32 SeitenTaxation TheoryKaycia HyltonNoch keine Bewertungen

- Theory and Basis of TaxationDokument8 SeitenTheory and Basis of TaxationGreggy BoyNoch keine Bewertungen

- Taxation LawsDokument15 SeitenTaxation LawsVikas RockNoch keine Bewertungen

- Chapter Three: General Overview of TaxationDokument68 SeitenChapter Three: General Overview of TaxationWagner AdugnaNoch keine Bewertungen

- MEC 52 Notes Chapters 1 To 3Dokument10 SeitenMEC 52 Notes Chapters 1 To 3Princess Niña Layne SususcoNoch keine Bewertungen

- Public Finance CH 2Dokument30 SeitenPublic Finance CH 2kussia toramaNoch keine Bewertungen

- Chapter One: Introduction To TaxationDokument46 SeitenChapter One: Introduction To Taxationembiale ayaluNoch keine Bewertungen

- General Principles - Concept, Nature, and CharacteristicsDokument17 SeitenGeneral Principles - Concept, Nature, and CharacteristicsRico AbbiegailNoch keine Bewertungen

- IntroductionDokument30 SeitenIntroductionSeifu BekeleNoch keine Bewertungen

- Fundamental S of Taxati OnDokument14 SeitenFundamental S of Taxati OnMyka FranciscoNoch keine Bewertungen

- RPH M4 Lesson 4 Canvas NotesDokument2 SeitenRPH M4 Lesson 4 Canvas NotesJELA MAE RIOSANoch keine Bewertungen

- General Principles of TaxationDokument50 SeitenGeneral Principles of TaxationJessa PerdigonNoch keine Bewertungen

- Basics About Sales, Use, and Other Transactional Taxes: Overview of Transactional Taxes for Consideration When Striving Toward the Maximization of Tax Compliance and Minimization of Tax Costs.Von EverandBasics About Sales, Use, and Other Transactional Taxes: Overview of Transactional Taxes for Consideration When Striving Toward the Maximization of Tax Compliance and Minimization of Tax Costs.Noch keine Bewertungen

- TAX - 601 - Individuals - Abapo, Mary Jhudiel G.Dokument53 SeitenTAX - 601 - Individuals - Abapo, Mary Jhudiel G.Mohammad100% (1)

- Tabulation Guidelines 1Dokument4 SeitenTabulation Guidelines 1MohammadNoch keine Bewertungen

- TAX 1801 Basic Principles - Hadji Usop, Norhanisah B PDFDokument26 SeitenTAX 1801 Basic Principles - Hadji Usop, Norhanisah B PDFMohammadNoch keine Bewertungen

- 5 Form MembershipDokument1 Seite5 Form MembershipMohammadNoch keine Bewertungen

- Tabulation Guidelines 1Dokument4 SeitenTabulation Guidelines 1MohammadNoch keine Bewertungen

- Pacalna - ApplicationDokument3 SeitenPacalna - ApplicationMohammadNoch keine Bewertungen

- OrMan Chapter 5Dokument36 SeitenOrMan Chapter 5MohammadNoch keine Bewertungen

- CHAPTER 4 - Revenues and Other ReceiptsDokument26 SeitenCHAPTER 4 - Revenues and Other ReceiptsMohammadNoch keine Bewertungen

- Extemporaneous SpeechDokument2 SeitenExtemporaneous SpeechMohammadNoch keine Bewertungen

- Banga Executive Summary 2018 PDFDokument5 SeitenBanga Executive Summary 2018 PDFMohammadNoch keine Bewertungen

- System Theory 1Dokument9 SeitenSystem Theory 1MohammadNoch keine Bewertungen

- CHAPTER 5 - DisbursementDokument25 SeitenCHAPTER 5 - DisbursementMohammadNoch keine Bewertungen

- Act102 Assessment2Dokument4 SeitenAct102 Assessment2MohammadNoch keine Bewertungen

- Partnership Formation - SolutionsDokument5 SeitenPartnership Formation - SolutionsMohammadNoch keine Bewertungen

- MoneyDokument23 SeitenMoneyMohammadNoch keine Bewertungen

- Chapter 3 - The Government Accounting ProcessDokument14 SeitenChapter 3 - The Government Accounting ProcessMohammadNoch keine Bewertungen

- NAME: - SECTION: - : THIRD QUARTER - Learning ModuleDokument4 SeitenNAME: - SECTION: - : THIRD QUARTER - Learning ModuleMohammadNoch keine Bewertungen

- Rule-Based Reasoning Relies On The Use of Syllogisms, or Arguments Based On Formal Logic. ADokument1 SeiteRule-Based Reasoning Relies On The Use of Syllogisms, or Arguments Based On Formal Logic. AMohammadNoch keine Bewertungen

- GenBio2 3Q Module1Dokument8 SeitenGenBio2 3Q Module1MohammadNoch keine Bewertungen

- Preliminary Exam in Cost Accounting and ControlDokument5 SeitenPreliminary Exam in Cost Accounting and ControlMohammadNoch keine Bewertungen

- D. All of The Above: A. Progressive TaxDokument6 SeitenD. All of The Above: A. Progressive TaxMohammadNoch keine Bewertungen

- Partnership Operations (Solutions)Dokument4 SeitenPartnership Operations (Solutions)MohammadNoch keine Bewertungen

- Filipina ("Philippine National March"), Is The: FilipinasDokument1 SeiteFilipina ("Philippine National March"), Is The: FilipinasMohammadNoch keine Bewertungen

- Income Tax On IndividualsDokument25 SeitenIncome Tax On IndividualsMohammadNoch keine Bewertungen

- History of The United StatesDokument5 SeitenHistory of The United StatesMohammadNoch keine Bewertungen

- PCL CasesDokument19 SeitenPCL CasesMohammadNoch keine Bewertungen

- Public Corporation CasesDokument41 SeitenPublic Corporation CasesMohammadNoch keine Bewertungen

- Four-Fold Test Economic Reality Test Two-Tiered Test (Or Multi-Factor Test)Dokument18 SeitenFour-Fold Test Economic Reality Test Two-Tiered Test (Or Multi-Factor Test)MohammadNoch keine Bewertungen

- Multiple Choice THEORY: Choose The Letter of The Correct AnswerDokument4 SeitenMultiple Choice THEORY: Choose The Letter of The Correct AnswerMohammadNoch keine Bewertungen

- What Is Transportation Engineering? Divided Into Four PartsDokument8 SeitenWhat Is Transportation Engineering? Divided Into Four PartsMohammadNoch keine Bewertungen

- Sworn Statement For Tax Clearance SampleDokument1 SeiteSworn Statement For Tax Clearance SampleRachel ChanNoch keine Bewertungen

- Advance Invoice: Bumax AbDokument2 SeitenAdvance Invoice: Bumax AbBruno FaveroNoch keine Bewertungen

- 0432 Merkblatt Zur Anmeldepflicht Von Barmitteln - Englisch - (2012) Seite - 1 - Von 3Dokument3 Seiten0432 Merkblatt Zur Anmeldepflicht Von Barmitteln - Englisch - (2012) Seite - 1 - Von 3Эльзар МаликовNoch keine Bewertungen

- Platinum CatalogueDokument17 SeitenPlatinum CataloguePSC.CLAIMS1Noch keine Bewertungen

- PMHPANYD23020003Dokument2 SeitenPMHPANYD23020003ashishNoch keine Bewertungen

- Agreeya Solutions (India) Private Limited: Earnings DeductionsDokument1 SeiteAgreeya Solutions (India) Private Limited: Earnings DeductionsGirnar studioNoch keine Bewertungen

- DBM Compensation Policy Guidelines No. 98-1 (Page 1 of 2)Dokument1 SeiteDBM Compensation Policy Guidelines No. 98-1 (Page 1 of 2)Rej Francisco100% (1)

- AKUPREPSLPWDokument1 SeiteAKUPREPSLPWuzrabaig111Noch keine Bewertungen

- NPV Calculation of Euro DisneylandDokument5 SeitenNPV Calculation of Euro DisneylandRama SubramanianNoch keine Bewertungen

- Sample Deed of Sale House and Lot OneDokument3 SeitenSample Deed of Sale House and Lot Oneapbuera72% (47)

- Masotta Marcelo Bruno 11 de Semptiembre 530 1653 Buenos Aires ArgentinienDokument1 SeiteMasotta Marcelo Bruno 11 de Semptiembre 530 1653 Buenos Aires ArgentinienAntonela MasottaNoch keine Bewertungen

- Income From BusinessDokument14 SeitenIncome From BusinessPreeti ShresthaNoch keine Bewertungen

- Service Invoice For October 2020Dokument1 SeiteService Invoice For October 2020YasirTajNoch keine Bewertungen

- Suture Al Wali 13-1Dokument1 SeiteSuture Al Wali 13-1Arsal Ghulam MustafaNoch keine Bewertungen

- Disbur Form Series 100-500, 800 & 801Dokument12 SeitenDisbur Form Series 100-500, 800 & 801Geno GottschallNoch keine Bewertungen

- 3 Key Features of The GICC Protocol - American ExpressDokument232 Seiten3 Key Features of The GICC Protocol - American Expressvanitha gunasekaranNoch keine Bewertungen

- 20 - 22 September 2007. Chennai, India.: The 6th EditionDokument10 Seiten20 - 22 September 2007. Chennai, India.: The 6th EditionkavenindiaNoch keine Bewertungen

- Nashik CorrectDokument8 SeitenNashik Correctrompal decorationNoch keine Bewertungen

- Estmt - 2024 02 22Dokument10 SeitenEstmt - 2024 02 22jpneebNoch keine Bewertungen

- 캐나다 CLC 토론토 CLC - reg - formDokument2 Seiten캐나다 CLC 토론토 CLC - reg - formJoins 세계유학Noch keine Bewertungen

- TO: Atty. Stephen Yu FROM: Maria Ludica B. Oja DATE: January 13, 2017 Subject: Transfer Pricing Transfer Pricing DefinedDokument4 SeitenTO: Atty. Stephen Yu FROM: Maria Ludica B. Oja DATE: January 13, 2017 Subject: Transfer Pricing Transfer Pricing DefinedLudica OjaNoch keine Bewertungen

- Auchi PolyDokument1 SeiteAuchi PolyESECHIE CEPHASNoch keine Bewertungen

- Accommodation at Vivekananda Kendra Kanyakumari - Vivekananda Kendra HyderabadDokument7 SeitenAccommodation at Vivekananda Kendra Kanyakumari - Vivekananda Kendra HyderabadPrabhat JainNoch keine Bewertungen

- Corporate Income TaxationDokument3 SeitenCorporate Income TaxationKezNoch keine Bewertungen

- 2 PDFDokument97 Seiten2 PDFaamir shaikhNoch keine Bewertungen

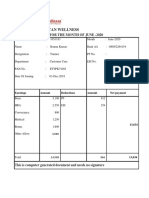

- Hindustan Wellness: Pay Slip For The Month of June - 2020Dokument3 SeitenHindustan Wellness: Pay Slip For The Month of June - 2020ManishNoch keine Bewertungen

- CIR v. Aichi ForgingDokument1 SeiteCIR v. Aichi ForgingVanya Klarika NuqueNoch keine Bewertungen

- WA0000 UnlockedDokument24 SeitenWA0000 UnlockedwordscriptNoch keine Bewertungen

- Od 226081369724248000Dokument1 SeiteOd 226081369724248000Chirag ChauhanNoch keine Bewertungen

- Tax 1 NotesDokument13 SeitenTax 1 NotesCamille Antoinette BarizoNoch keine Bewertungen