Das könnte Ihnen auch gefallen

- Fiscal Decentralization Reform in Cambodia: Progress over the Past Decade and OpportunitiesVon EverandFiscal Decentralization Reform in Cambodia: Progress over the Past Decade and OpportunitiesNoch keine Bewertungen

- Sesssion 5 17-Oct-2020Dokument44 SeitenSesssion 5 17-Oct-2020Uzma UzmaNoch keine Bewertungen

- Maximizing Tax Credits Presentation - January 19, 2022Dokument13 SeitenMaximizing Tax Credits Presentation - January 19, 2022WVXU NewsNoch keine Bewertungen

- Corinthian Newsletter (Feb 2010)Dokument1 SeiteCorinthian Newsletter (Feb 2010)austin1467Noch keine Bewertungen

- MMB - ABIX RecommendationDokument1 SeiteMMB - ABIX RecommendationLogic Gate CapitalNoch keine Bewertungen

- Affordable Housing & Housing FinanceDokument11 SeitenAffordable Housing & Housing FinanceUmang PanchalNoch keine Bewertungen

- L&T Finance Holdings - GeojitDokument4 SeitenL&T Finance Holdings - GeojitdarshanmadeNoch keine Bewertungen

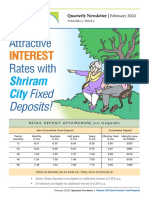

- Attractive Rates With: InterestDokument4 SeitenAttractive Rates With: Interestdharam singhNoch keine Bewertungen

- LiquiLoans - Monthly Portfolio Factsheet - As On 30th April 2023Dokument2 SeitenLiquiLoans - Monthly Portfolio Factsheet - As On 30th April 2023Raghuraman SelvamaniNoch keine Bewertungen

- Colliers Manila Q3 2022 Residential v2Dokument4 SeitenColliers Manila Q3 2022 Residential v2bhandari_raviNoch keine Bewertungen

- Understanding Affordable Housing Finance 102Dokument21 SeitenUnderstanding Affordable Housing Finance 102Cesar YocNoch keine Bewertungen

- HDFC May24 19Dokument49 SeitenHDFC May24 19jatinNoch keine Bewertungen

- Buffalo Comptroller Fund Balance PresentationDokument9 SeitenBuffalo Comptroller Fund Balance PresentationGeoff KellyNoch keine Bewertungen

- INSIDE THE Membership: Fiscal Year 2018 Statistical Highlights From The OFN MembershipDokument2 SeitenINSIDE THE Membership: Fiscal Year 2018 Statistical Highlights From The OFN MembershipAng KianboonNoch keine Bewertungen

- Rating Rationale CRISILDokument8 SeitenRating Rationale CRISILhareshNoch keine Bewertungen

- 2022 IndexofEconomicFreedom-QatarDokument2 Seiten2022 IndexofEconomicFreedom-QatarUmar Shaheen ANoch keine Bewertungen

- Sanchay Public Deposit FormDokument6 SeitenSanchay Public Deposit Formmanoj barokaNoch keine Bewertungen

- Development EcoDokument3 SeitenDevelopment EcoMadhurendra SinghNoch keine Bewertungen

- 2015 Jan Update On BDC SDokument9 Seiten2015 Jan Update On BDC SSSNoch keine Bewertungen

- Chapter 12 10 03 2017Dokument11 SeitenChapter 12 10 03 2017jncbrazilNoch keine Bewertungen

- City Union ResearchDokument38 SeitenCity Union ResearchamitNoch keine Bewertungen

- Asset Reconstruction Companies Asset Reconstruction CompaniesDokument24 SeitenAsset Reconstruction Companies Asset Reconstruction CompaniesShreyansh RavalNoch keine Bewertungen

- Sbi Corporate Bond FundDokument21 SeitenSbi Corporate Bond FundGourab BhattacharjeeNoch keine Bewertungen

- Equitas Small Finance Bank Company UpdateDokument10 SeitenEquitas Small Finance Bank Company Updatefinal bossuNoch keine Bewertungen

- HDFC Nov02 18 PDFDokument49 SeitenHDFC Nov02 18 PDFMamta WaghelaNoch keine Bewertungen

- Chapter-4 RETAIL LENDING SCHEMES PDFDokument64 SeitenChapter-4 RETAIL LENDING SCHEMES PDFNanda KishoreNoch keine Bewertungen

- Home First Finance Company India LTD.: SubscribeDokument7 SeitenHome First Finance Company India LTD.: SubscribeVanshajNoch keine Bewertungen

- RecDokument28 SeitenRecChirag ShahNoch keine Bewertungen

- Fine Tuning Estimates, Maintain BUY: Share DataDokument4 SeitenFine Tuning Estimates, Maintain BUY: Share DataJajahinaNoch keine Bewertungen

- MB20202 Corporate Finance Unit V Study MaterialsDokument33 SeitenMB20202 Corporate Finance Unit V Study MaterialsSarath kumar CNoch keine Bewertungen

- Downgrading Estimates On Higher Provisions Maintain BUY: Bank of The Philippine IslandsDokument8 SeitenDowngrading Estimates On Higher Provisions Maintain BUY: Bank of The Philippine IslandsJNoch keine Bewertungen

- 040221-FINAL P3D-DFs DEC 2020 DTD 04FEB2020Dokument12 Seiten040221-FINAL P3D-DFs DEC 2020 DTD 04FEB2020Neradabilli EswarNoch keine Bewertungen

- Digital Consumer Lending - August 2019Dokument22 SeitenDigital Consumer Lending - August 2019Radha Madhuri100% (1)

- Coopbank Annual Report EnglishDokument120 SeitenCoopbank Annual Report Englishabayneshkeno99Noch keine Bewertungen

- Morning 15oct20.15 10 2020 - 01 39 12Dokument8 SeitenMorning 15oct20.15 10 2020 - 01 39 12fathur abrarNoch keine Bewertungen

- ValuEngine Weekly Newsletter September 24, 2010Dokument7 SeitenValuEngine Weekly Newsletter September 24, 2010ValuEngine.comNoch keine Bewertungen

- Capital Adequacy Presentation 1Dokument16 SeitenCapital Adequacy Presentation 1Nafiz Imran DiptoNoch keine Bewertungen

- Zacks Small-Cap Research: Corecivic, IncDokument8 SeitenZacks Small-Cap Research: Corecivic, IncKarim LahrichiNoch keine Bewertungen

- CRB FinalsDokument3 SeitenCRB FinalsPavitra BhagavatulaNoch keine Bewertungen

- RealPoint CMBS Methodology DisclosureDokument19 SeitenRealPoint CMBS Methodology DisclosureCarneadesNoch keine Bewertungen

- Can Fin Homes - IC Oct, 2017Dokument11 SeitenCan Fin Homes - IC Oct, 2017milandeepNoch keine Bewertungen

- Lic Housing Finance - : Proxy To Play The Real Estate RecoveryDokument4 SeitenLic Housing Finance - : Proxy To Play The Real Estate Recoverysaipavan999Noch keine Bewertungen

- Subh NiveshDokument3 SeitenSubh NiveshhrplanetsparkindoreNoch keine Bewertungen

- Muthoot FinDokument12 SeitenMuthoot FinMahesh Karande (KOEL)Noch keine Bewertungen

- 1cr17mba61 ProjectDokument19 Seiten1cr17mba61 ProjectPraveen Kumar100% (2)

- Capitec Bank - Valuation Looks Steep But Growth Outlook Is The Differentiating Factor - FinalDokument54 SeitenCapitec Bank - Valuation Looks Steep But Growth Outlook Is The Differentiating Factor - FinalMukarangaNoch keine Bewertungen

- New Year Report 2021 HDFC SecuritiesDokument25 SeitenNew Year Report 2021 HDFC SecuritiesSriram RanganathanNoch keine Bewertungen

- Investment Appraisal: Pacific Grove Spice CompanyDokument9 SeitenInvestment Appraisal: Pacific Grove Spice CompanyPrabir PujariNoch keine Bewertungen

- FY 2021 Carryover FundsDokument8 SeitenFY 2021 Carryover FundsWVXU NewsNoch keine Bewertungen

- Housing and Urban Development Corporation LTD: IPO ReviewDokument16 SeitenHousing and Urban Development Corporation LTD: IPO Reviewsai kiran mallepallyNoch keine Bewertungen

- CGD Annual Budget 2018 19Dokument185 SeitenCGD Annual Budget 2018 19Kould BNoch keine Bewertungen

- Final Presentation 30.8.2019 FM's ConferenceDokument33 SeitenFinal Presentation 30.8.2019 FM's Conferencepranathi.862539Noch keine Bewertungen

- ValueResearchFundcard FranklinIndiaUltraShortBondFund SuperInstitutionalPlan DirectPlan 2017oct11Dokument4 SeitenValueResearchFundcard FranklinIndiaUltraShortBondFund SuperInstitutionalPlan DirectPlan 2017oct11jamsheer.aaNoch keine Bewertungen

- Efsl-7028011153 NCD Oct23Dokument1 SeiteEfsl-7028011153 NCD Oct23chandraprakash sharmaNoch keine Bewertungen

- FY21 Budget Presentation To CouncilDokument25 SeitenFY21 Budget Presentation To CouncilNewsChannel 9 StaffNoch keine Bewertungen

- Rating Rationale CampusDokument6 SeitenRating Rationale CampusRavi BabuNoch keine Bewertungen

- 072420-Commercial Mortgage Market Monitor June 2020Dokument58 Seiten072420-Commercial Mortgage Market Monitor June 2020KyleNoch keine Bewertungen

- IDirect NCC ConvictionIdeaDokument8 SeitenIDirect NCC ConvictionIdeaVivek GuptaNoch keine Bewertungen

- Group No. 2 (CF)Dokument15 SeitenGroup No. 2 (CF)Dhrupal TripathiNoch keine Bewertungen

- BofA - The Next Default Cycle Research Report - HY-51472Dokument17 SeitenBofA - The Next Default Cycle Research Report - HY-51472ManeeshNoch keine Bewertungen

- Training Basic Sea SurvivalDokument6 SeitenTraining Basic Sea Survivalrico septyanNoch keine Bewertungen

- (Muhammad Ashraf & Muqeem Ul Islam) : Media Activism and Its Impacts On The Psychology of Pakistani Society'Dokument30 Seiten(Muhammad Ashraf & Muqeem Ul Islam) : Media Activism and Its Impacts On The Psychology of Pakistani Society'naweedahmedNoch keine Bewertungen

- Press ReleaseBolsa Chica BacteriaDokument2 SeitenPress ReleaseBolsa Chica Bacteriasurfdad67% (3)

- 8 Sherwill Vs Sitio Sto NinoDokument7 Seiten8 Sherwill Vs Sitio Sto NinoJonathan Vargas NograNoch keine Bewertungen

- 2018 Batch Credit HistoryDokument6 Seiten2018 Batch Credit HistoryReshma DanielNoch keine Bewertungen

- Escrow Agreement, Trust Und (NY State Dept of Law)Dokument6 SeitenEscrow Agreement, Trust Und (NY State Dept of Law)Jay GiardinaNoch keine Bewertungen

- 8milam ItcDokument1 Seite8milam Itcatishi88Noch keine Bewertungen

- Lec 32714 yDokument42 SeitenLec 32714 yPakHoFungNoch keine Bewertungen

- HR Audit ChecklistDokument4 SeitenHR Audit Checklistpielzapa50% (2)

- Arnault Vs BalagtasDokument7 SeitenArnault Vs BalagtasKrishiena MerillesNoch keine Bewertungen

- PPSA Reviewer PDFDokument15 SeitenPPSA Reviewer PDFKobe Lawrence VeneracionNoch keine Bewertungen

- Module 12: WLAN Concepts: Instructor MaterialsDokument56 SeitenModule 12: WLAN Concepts: Instructor Materialsjorigoni2013100% (1)

- Succession Case Compilation Page 2 of 9Dokument122 SeitenSuccession Case Compilation Page 2 of 9mccm92Noch keine Bewertungen

- Book of Mormon: Scripture Stories Coloring BookDokument22 SeitenBook of Mormon: Scripture Stories Coloring BookJEJESILZANoch keine Bewertungen

- Instant DiscussionsDokument97 SeitenInstant DiscussionsFlávia Machado100% (1)

- Chapter 4 Consumer ChoiceDokument38 SeitenChapter 4 Consumer ChoiceThăng Nguyễn BáNoch keine Bewertungen

- Econ 1Bb3: Introductory Macroeconomics Sections C01, C02 Mcmaster University Fall, 2015Dokument6 SeitenEcon 1Bb3: Introductory Macroeconomics Sections C01, C02 Mcmaster University Fall, 2015Labeeb HossainNoch keine Bewertungen

- VC Arun Prasad: Manager - Marketing (International Business)Dokument4 SeitenVC Arun Prasad: Manager - Marketing (International Business)rameshshNoch keine Bewertungen

- FPP1x - Slides Introduction To FPP PDFDokument10 SeitenFPP1x - Slides Introduction To FPP PDFEugenio HerreraNoch keine Bewertungen

- ResearchDokument8 SeitenResearchMitchele Piamonte MamalesNoch keine Bewertungen

- CAN Vs COULDDokument5 SeitenCAN Vs COULDE'lena EremenkoNoch keine Bewertungen

- Tendernotice - 1 (4) 638043623175233354Dokument5 SeitenTendernotice - 1 (4) 638043623175233354Ar Shubham KumarNoch keine Bewertungen

- Child Marriage - Addressing The Challenges and Obstacles in The Po PDFDokument36 SeitenChild Marriage - Addressing The Challenges and Obstacles in The Po PDFvibhayNoch keine Bewertungen

- PDF Document 2Dokument11 SeitenPDF Document 2rizzacasipong413Noch keine Bewertungen

- Topic 1 Database ConceptsDokument62 SeitenTopic 1 Database ConceptsNowlghtNoch keine Bewertungen

- Hist 708 Syllabus RevisedDokument11 SeitenHist 708 Syllabus Revisedapi-370320558Noch keine Bewertungen

- The Imperial Mughal Tomb of Jahangir His PDFDokument7 SeitenThe Imperial Mughal Tomb of Jahangir His PDFNida AtifNoch keine Bewertungen

- The Elephant by Slawomir MrozekDokument4 SeitenThe Elephant by Slawomir Mrozeklaguman Gurung100% (6)

- Redbook Vol2part1Dokument92 SeitenRedbook Vol2part1ChadNoch keine Bewertungen

- RQM Best PracticesDokument52 SeitenRQM Best PracticesOlalekan FagbemiroNoch keine Bewertungen