Das könnte Ihnen auch gefallen

- BVCA Model Term Sheet For A Series A Round - Sept 2015Dokument15 SeitenBVCA Model Term Sheet For A Series A Round - Sept 2015GabrielaNoch keine Bewertungen

- Problems On Confidence IntervalDokument6 SeitenProblems On Confidence Intervalrangoli maheshwariNoch keine Bewertungen

- Topic 7 - Cost-Volume-Profit Analysis (Student Version)Dokument28 SeitenTopic 7 - Cost-Volume-Profit Analysis (Student Version)Nur afiqahNoch keine Bewertungen

- Pre-Test Entreprenuership Grade-12 Choose The Best AnswerDokument5 SeitenPre-Test Entreprenuership Grade-12 Choose The Best AnswerMark Gil GuillermoNoch keine Bewertungen

- Aurora Textile Company (SPREADSHEET) F-1536X - FCVDokument15 SeitenAurora Textile Company (SPREADSHEET) F-1536X - FCVPaco ColínNoch keine Bewertungen

- JP Morgan Chase - DeckDokument9 SeitenJP Morgan Chase - DeckRahul Girish KumarNoch keine Bewertungen

- Cir v. Menguito DigestDokument3 SeitenCir v. Menguito Digestkathrynmaydeveza100% (1)

- Management Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageVon EverandManagement Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageBewertung: 5 von 5 Sternen5/5 (1)

- Chapter 21 Merger and AcquisitionDokument2 SeitenChapter 21 Merger and AcquisitionLemeryNoch keine Bewertungen

- Supply Chain Finance at Procter & Gamble - 6713-XLS-ENGDokument37 SeitenSupply Chain Finance at Procter & Gamble - 6713-XLS-ENGKunal Mehta100% (2)

- Cost-Volume-Profit Analysis: A Managerial Planning Tool: Kelompok 2: Alifia Maya Savira Gamma Yuni NurvistaDokument21 SeitenCost-Volume-Profit Analysis: A Managerial Planning Tool: Kelompok 2: Alifia Maya Savira Gamma Yuni Nurvistavira0% (1)

- CVP AnalysisDokument21 SeitenCVP AnalysisDaksh AnejaNoch keine Bewertungen

- CVP AnalysisDokument29 SeitenCVP Analysishukumsingh01juneNoch keine Bewertungen

- Cost-Volume-Profit AnalysisDokument24 SeitenCost-Volume-Profit AnalysisIbrahim ElsayedNoch keine Bewertungen

- Cost-Volume-Profit AnalysisDokument56 SeitenCost-Volume-Profit AnalysisAgatNoch keine Bewertungen

- CVP AnalysisDokument28 SeitenCVP AnalysisSurender SinghNoch keine Bewertungen

- Cost Behaviour & Decision Making - HodDokument65 SeitenCost Behaviour & Decision Making - Hodsrimant100% (2)

- Fundamental: Managerial Accounting ConceptsDokument17 SeitenFundamental: Managerial Accounting ConceptsRosh OtojanovNoch keine Bewertungen

- Chapter-9: Cost-Volume-Profit Analysis (CVP)Dokument54 SeitenChapter-9: Cost-Volume-Profit Analysis (CVP)selamawitNoch keine Bewertungen

- Cost Volume ProvitDokument57 SeitenCost Volume ProvitannisaNoch keine Bewertungen

- Chapter 8 CVP AnalysisDokument25 SeitenChapter 8 CVP AnalysisCyrus John LopezNoch keine Bewertungen

- CVP AnalysisDokument40 SeitenCVP Analysissbjafri0Noch keine Bewertungen

- Chapter 2 CVP AnalysisDokument56 SeitenChapter 2 CVP AnalysisnathalieroseNoch keine Bewertungen

- CVP Analysis - PPT (Autosaved)Dokument33 SeitenCVP Analysis - PPT (Autosaved)Anonymous gDxeGLYNoch keine Bewertungen

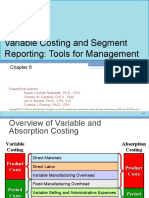

- Variable Costing and Segment Reporting: Tools For ManagementDokument20 SeitenVariable Costing and Segment Reporting: Tools For ManagementAbed Al-Rahman SalehNoch keine Bewertungen

- AccountingDokument9 SeitenAccountingaarti saxenaNoch keine Bewertungen

- Hilton Chapter 7 NotesDokument27 SeitenHilton Chapter 7 Notestoughguy9Noch keine Bewertungen

- Chapter CVP AnalysisDokument24 SeitenChapter CVP Analysisabshir haybeNoch keine Bewertungen

- Cost-Volume-Profit Analysis A Managerial Planning ToolDokument15 SeitenCost-Volume-Profit Analysis A Managerial Planning ToolanomsawitriNoch keine Bewertungen

- Lect # 10a CVPDokument44 SeitenLect # 10a CVPAimen KhanNoch keine Bewertungen

- CMA Part 2 Financial Decision Making: Study Unit 8 - CVP Analysis and Marginal AnalysisDokument85 SeitenCMA Part 2 Financial Decision Making: Study Unit 8 - CVP Analysis and Marginal AnalysisNEERAJ GUPTANoch keine Bewertungen

- CVP1 MarkupsDokument15 SeitenCVP1 MarkupsWaleed J.Noch keine Bewertungen

- Arginal OstingDokument69 SeitenArginal Ostingmoses jcNoch keine Bewertungen

- Tutorial Chapter 12 Cost Behaviour and Measurement of CostsDokument54 SeitenTutorial Chapter 12 Cost Behaviour and Measurement of CostsNaKib Nahri0% (1)

- CVP Analysis: PG D M2 0 21-23 RelevantreadingsDokument21 SeitenCVP Analysis: PG D M2 0 21-23 RelevantreadingsAthi SivaNoch keine Bewertungen

- Session Objectives:: Methods of Costing?Dokument15 SeitenSession Objectives:: Methods of Costing?Sachin YadavNoch keine Bewertungen

- Break-Even Point and Cost-Volume-Profit Analysis: QuestionsDokument34 SeitenBreak-Even Point and Cost-Volume-Profit Analysis: QuestionsGuinevereNoch keine Bewertungen

- Information For Decision MakingDokument33 SeitenInformation For Decision Makingwambualucas74Noch keine Bewertungen

- M10 CVP RelationshipDokument72 SeitenM10 CVP Relationship3ID04Viviani RaraNoch keine Bewertungen

- Lecture CVPDokument58 SeitenLecture CVPKashif RaheemNoch keine Bewertungen

- 10-CVP AnalysisDokument77 Seiten10-CVP AnalysissurangauorNoch keine Bewertungen

- Managerial Accounting Managerial AccountingDokument30 SeitenManagerial Accounting Managerial Accountingpvsk17072005Noch keine Bewertungen

- 006 Camist Ch04 Amndd Hs PP 79-102 Branded BW RP SecDokument25 Seiten006 Camist Ch04 Amndd Hs PP 79-102 Branded BW RP SecMd Salahuddin HowladerNoch keine Bewertungen

- Kinney8e PPT Ch09Dokument36 SeitenKinney8e PPT Ch09Ashraf ZamanNoch keine Bewertungen

- Document From VandanaDokument39 SeitenDocument From VandanaVandana SharmaNoch keine Bewertungen

- MA & CA-Merginal & Absorption Costing PDFDokument8 SeitenMA & CA-Merginal & Absorption Costing PDFRashfi RussellNoch keine Bewertungen

- 7 - CPV Coûts Variables en AnglaisDokument56 Seiten7 - CPV Coûts Variables en AnglaislolaNoch keine Bewertungen

- Future: Classification of Costs For Decision Making and PlanningDokument30 SeitenFuture: Classification of Costs For Decision Making and PlanningSarvar PathanNoch keine Bewertungen

- Cost Volume Profit AnalysisDokument63 SeitenCost Volume Profit AnalysisJunaid KhalidNoch keine Bewertungen

- Module 4Dokument42 SeitenModule 4Eshael FathimaNoch keine Bewertungen

- Variable Costing and Segment Reporting: Tools For ManagementDokument20 SeitenVariable Costing and Segment Reporting: Tools For ManagementFarhan RabbehNoch keine Bewertungen

- Marginal CostingDokument80 SeitenMarginal CostingParamjit Sharma96% (25)

- Cost Volume Profit AnalysisDokument25 SeitenCost Volume Profit AnalysisAmit DeyNoch keine Bewertungen

- CHP 14. Marginal Costing - CAPRANAVDokument28 SeitenCHP 14. Marginal Costing - CAPRANAVAYUSH RAJNoch keine Bewertungen

- Lesson 4 HND in Business Unit 5 Management AccountingDokument32 SeitenLesson 4 HND in Business Unit 5 Management AccountingShan Wikoon LLB LLM100% (3)

- Marginal Costing and Cost-Volume-Profit (CVP) Analysis: Hammad Javed Vohra, FCCADokument25 SeitenMarginal Costing and Cost-Volume-Profit (CVP) Analysis: Hammad Javed Vohra, FCCAUrooj MustafaNoch keine Bewertungen

- Sony Xperia Z - Assemble Your Device - EE HelpDokument21 SeitenSony Xperia Z - Assemble Your Device - EE HelpsugambordoloiNoch keine Bewertungen

- Abraham Assignment 1Dokument5 SeitenAbraham Assignment 1SKY StationeryNoch keine Bewertungen

- Variable Costing-A Tool For Management MFHDokument40 SeitenVariable Costing-A Tool For Management MFHBadhan FirdousNoch keine Bewertungen

- CVP SummaryDokument4 SeitenCVP Summaryandilemaa30Noch keine Bewertungen

- Cost Volume Profit (CVP) Analysis-2Dokument47 SeitenCost Volume Profit (CVP) Analysis-2Mohamed El MjounahNoch keine Bewertungen

- CVP RelationshipDokument14 SeitenCVP RelationshipSarith SagarNoch keine Bewertungen

- 18.marginal Absorption NewDokument17 Seiten18.marginal Absorption NewMuhammad EjazNoch keine Bewertungen

- Fina and Mana Accounting Chapter FourDokument77 SeitenFina and Mana Accounting Chapter FourAklilu TadesseNoch keine Bewertungen

- Chapter Five 111Dokument76 SeitenChapter Five 111Ras DawitNoch keine Bewertungen

- Profitability Analysis FrameworkpdfDokument10 SeitenProfitability Analysis FrameworkpdfObalowu Bolaji YusufNoch keine Bewertungen

- Business & Finance Chapter-7 Part-02 PDFDokument12 SeitenBusiness & Finance Chapter-7 Part-02 PDFRafidul IslamNoch keine Bewertungen

- 02 Profit PlanningDokument32 Seiten02 Profit PlanningJelliane de la CruzNoch keine Bewertungen

- Care - Fit PlanDokument9 SeitenCare - Fit Planrangoli maheshwariNoch keine Bewertungen

- Cash Flow StatementDokument16 SeitenCash Flow Statementrangoli maheshwariNoch keine Bewertungen

- Financial Analysis - IMIDokument9 SeitenFinancial Analysis - IMIrangoli maheshwariNoch keine Bewertungen

- Swot AnalysisDokument6 SeitenSwot Analysisrangoli maheshwariNoch keine Bewertungen

- Introduction To AccountingDokument39 SeitenIntroduction To Accountingrangoli maheshwariNoch keine Bewertungen

- ESOPs - IMIDokument13 SeitenESOPs - IMIrangoli maheshwariNoch keine Bewertungen

- ME ET HRM 19 Oct 10:00 IMI ExamDokument8 SeitenME ET HRM 19 Oct 10:00 IMI Examrangoli maheshwariNoch keine Bewertungen

- Percent ChangeDokument3 SeitenPercent Changerangoli maheshwariNoch keine Bewertungen

- Sl. No. Roll No. Employee Code Name of The StudentsDokument4 SeitenSl. No. Roll No. Employee Code Name of The Studentsrangoli maheshwariNoch keine Bewertungen

- Elasticity PDFDokument8 SeitenElasticity PDFrangoli maheshwariNoch keine Bewertungen

- Shareholders' Equity: - Amount Raised by Co. As Equity SharesDokument2 SeitenShareholders' Equity: - Amount Raised by Co. As Equity Sharesrangoli maheshwariNoch keine Bewertungen

- Practice Set 1 - SolutionsDokument3 SeitenPractice Set 1 - Solutionsrangoli maheshwariNoch keine Bewertungen

- About The Ambulance Quality Indicators (AQI) : SourceDokument44 SeitenAbout The Ambulance Quality Indicators (AQI) : Sourcerangoli maheshwariNoch keine Bewertungen

- Purchase Amount Discount % 0 0 Purchase Amount 600 100 2 Discount % 4 200 3 500 4 1000 5Dokument7 SeitenPurchase Amount Discount % 0 0 Purchase Amount 600 100 2 Discount % 4 200 3 500 4 1000 5rangoli maheshwariNoch keine Bewertungen

- Table 8. Estimated Revenue by Product and Class of Customer For Employer Firms: 2013 Through 2018Dokument10 SeitenTable 8. Estimated Revenue by Product and Class of Customer For Employer Firms: 2013 Through 2018rangoli maheshwariNoch keine Bewertungen

- Real EstateDokument24 SeitenReal Estaterangoli maheshwariNoch keine Bewertungen

- S.No Name Income IT Net IncomeDokument4 SeitenS.No Name Income IT Net Incomerangoli maheshwariNoch keine Bewertungen

- Ambulance Services: Median Response Times To Red Calls (Minutes and Seconds), October 2015 OnwardsDokument13 SeitenAmbulance Services: Median Response Times To Red Calls (Minutes and Seconds), October 2015 Onwardsrangoli maheshwariNoch keine Bewertungen

- Solution of Practice QuestionsDokument4 SeitenSolution of Practice Questionsrangoli maheshwariNoch keine Bewertungen

- Regression ND CorrelationDokument10 SeitenRegression ND Correlationrangoli maheshwariNoch keine Bewertungen

- Ambulance Services: Median Response Times To Red Calls (Minutes and Seconds), October 2015 OnwardsDokument22 SeitenAmbulance Services: Median Response Times To Red Calls (Minutes and Seconds), October 2015 Onwardsrangoli maheshwariNoch keine Bewertungen

- Employees With The: $18.1 Billion in 2019Dokument3 SeitenEmployees With The: $18.1 Billion in 2019rangoli maheshwariNoch keine Bewertungen

- Sampling Distributions Solved QuestionsDokument4 SeitenSampling Distributions Solved Questionsrangoli maheshwariNoch keine Bewertungen

- Productivity Analysis of Steel IndustryDokument9 SeitenProductivity Analysis of Steel IndustryDr-Abhijit SinhaNoch keine Bewertungen

- Credit FrameworkDokument10 SeitenCredit Frameworkzubair1951Noch keine Bewertungen

- PPI Provisional BST 2018-19Dokument6 SeitenPPI Provisional BST 2018-19accounts ppintNoch keine Bewertungen

- Why Do Banks Disappear?: A History of Bank Failures and Acquisitions in Trinidad, 1836-1992Dokument26 SeitenWhy Do Banks Disappear?: A History of Bank Failures and Acquisitions in Trinidad, 1836-1992Sauvik ChakrabortyNoch keine Bewertungen

- Form 29B - MAT Report Under Sec 115JDokument4 SeitenForm 29B - MAT Report Under Sec 115JChethan VenkateshNoch keine Bewertungen

- ACA Principles of Tax Expenses NotesDokument3 SeitenACA Principles of Tax Expenses Noteswguate0% (1)

- PFRS 3 - Business Combination, PAS 27 - Consolidated and Separate Financial StatementsDokument5 SeitenPFRS 3 - Business Combination, PAS 27 - Consolidated and Separate Financial Statementsd.pagkatoytoyNoch keine Bewertungen

- Propsed BooksDokument8 SeitenPropsed BooksOmer AwanNoch keine Bewertungen

- MercedesDokument138 SeitenMercedesMihaela DavidoaiaNoch keine Bewertungen

- Government Accounting: (Unified Account Code Structure)Dokument13 SeitenGovernment Accounting: (Unified Account Code Structure)Mariella AngobNoch keine Bewertungen

- Fiscal Policy PROJECTDokument11 SeitenFiscal Policy PROJECTompiyushsingh75% (8)

- Chapter 18 International Capital BudgetingDokument26 SeitenChapter 18 International Capital BudgetingBharat NayyarNoch keine Bewertungen

- Summary Regulation CPA NotesDokument2 SeitenSummary Regulation CPA Notesjklein2588100% (1)

- HLB Ijaaz Tabussum & Company by Mehar PDFDokument59 SeitenHLB Ijaaz Tabussum & Company by Mehar PDFRaja Rashid0% (1)

- PNC INFRATECH - ASM ProjectDokument11 SeitenPNC INFRATECH - ASM ProjectAbhijeet kohatNoch keine Bewertungen

- Critical Evaluation of Baumol ModelDokument4 SeitenCritical Evaluation of Baumol ModelWaleedSami100% (1)

- Kalu BPDokument28 SeitenKalu BPmarketingkaluproductionNoch keine Bewertungen

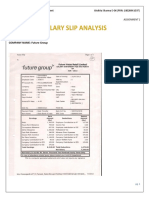

- Sector: Retail COMPANY NAME: Future GroupDokument3 SeitenSector: Retail COMPANY NAME: Future GroupAkshita SharmaNoch keine Bewertungen

- Flexible Budgeting Lecture: Fixed/Static BudgetsDokument4 SeitenFlexible Budgeting Lecture: Fixed/Static BudgetsSeana GeddesNoch keine Bewertungen

- Financial Accounting Ifrs Edition 2nd Edition Weygandt Test BankDokument26 SeitenFinancial Accounting Ifrs Edition 2nd Edition Weygandt Test BankDannyJohnsonobtk100% (48)

- ACCT 2019 Lecture Notes: Week 1: Introduction To Management AccountingDokument16 SeitenACCT 2019 Lecture Notes: Week 1: Introduction To Management AccountingRishabNoch keine Bewertungen

- Bank Performance Analysis - Anushka Gupta (Kotak Mahindra Bank)Dokument13 SeitenBank Performance Analysis - Anushka Gupta (Kotak Mahindra Bank)Surbhî GuptaNoch keine Bewertungen