Das könnte Ihnen auch gefallen

- Value Chain Management Capability A Complete Guide - 2020 EditionVon EverandValue Chain Management Capability A Complete Guide - 2020 EditionNoch keine Bewertungen

- Corporate Financial Analysis with Microsoft ExcelVon EverandCorporate Financial Analysis with Microsoft ExcelBewertung: 5 von 5 Sternen5/5 (1)

- Strategic Make or Buy Decision PDFDokument8 SeitenStrategic Make or Buy Decision PDFisnainarNoch keine Bewertungen

- DEFINITION of 'Make-Or-Buy Decision'Dokument11 SeitenDEFINITION of 'Make-Or-Buy Decision'Sandra MagnoNoch keine Bewertungen

- Notes VarianceDokument37 SeitenNotes Variancezms240Noch keine Bewertungen

- Capacity Planning FinalDokument59 SeitenCapacity Planning FinalSechelle SmithNoch keine Bewertungen

- BullWhip EffectDokument17 SeitenBullWhip EffectSaurabh Krishna SinghNoch keine Bewertungen

- Total Cost AnalysisDokument10 SeitenTotal Cost Analysisayane_sendoNoch keine Bewertungen

- Corporate Strategies - StabilityDokument85 SeitenCorporate Strategies - StabilityShivalisabharwal100% (2)

- Relevant Costs For Decision MakingDokument76 SeitenRelevant Costs For Decision Makingrachim040% (1)

- What Is Make-Or-Buy Decision?: Sa VeDokument9 SeitenWhat Is Make-Or-Buy Decision?: Sa VepriyankabgNoch keine Bewertungen

- Intro of Supply Chain Management Lecture 1Dokument20 SeitenIntro of Supply Chain Management Lecture 1Syeda SidraNoch keine Bewertungen

- Financial PlanningDokument25 SeitenFinancial Planningmaryloumarylou0% (1)

- Management Decision and ControlDokument30 SeitenManagement Decision and ControlAnuj KaulNoch keine Bewertungen

- Short-Run Decision Making and CVP AnalysisDokument43 SeitenShort-Run Decision Making and CVP AnalysisHy Tang100% (1)

- Bull Whip EffectDokument5 SeitenBull Whip EffectNandhini RamanathanNoch keine Bewertungen

- Cycle and Full Physical Counting Process - DraftDokument39 SeitenCycle and Full Physical Counting Process - DraftNitaiChand DasNoch keine Bewertungen

- Flow Chart & SipocDokument3 SeitenFlow Chart & SipocHarish Mordani100% (1)

- Budgeting Case Study Kraft PDFDokument2 SeitenBudgeting Case Study Kraft PDFpoojahj100% (1)

- Make or Buy DecisionDokument6 SeitenMake or Buy DecisionKinjalMehtaNoch keine Bewertungen

- Supply Chain and Logistics ManagementDokument76 SeitenSupply Chain and Logistics ManagementVishal Ranjan100% (5)

- Make or Buy DecisionDokument20 SeitenMake or Buy DecisionNitin Agarwal100% (1)

- 8 Performance Measurement Along Supply ChainDokument20 Seiten8 Performance Measurement Along Supply ChainAlena JosephNoch keine Bewertungen

- Make or Buy Research MaterialsDokument22 SeitenMake or Buy Research MaterialsDr Nagaraju VeldeNoch keine Bewertungen

- Chapter 3 - Cost Volume and Cost Volume Profit AnalysisDokument65 SeitenChapter 3 - Cost Volume and Cost Volume Profit AnalysisGabai AsaiNoch keine Bewertungen

- Four Elements of Supply Chain ManagementDokument3 SeitenFour Elements of Supply Chain ManagementSaikumar Sela0% (2)

- Marginal CostingDokument31 SeitenMarginal Costingdivya dharmarajan50% (4)

- Basic Cost Management ConceptsDokument15 SeitenBasic Cost Management ConceptsKatCaldwell100% (1)

- 5.0 Order-Winners and Qualifiers 2019 - 2020 PDFDokument72 Seiten5.0 Order-Winners and Qualifiers 2019 - 2020 PDFAizul FaizNoch keine Bewertungen

- The Nature and Scope of Cost & Management AccountingDokument17 SeitenThe Nature and Scope of Cost & Management Accountingfreshkidjay100% (5)

- Difference Between Job Costing and Operating CostingDokument1 SeiteDifference Between Job Costing and Operating Costingshraddhamal100% (2)

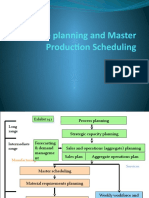

- Aggregate Planning and Master Production SchedulingDokument17 SeitenAggregate Planning and Master Production SchedulingAshwani Singh100% (1)

- Infosys Spend AnalysisDokument10 SeitenInfosys Spend AnalysisVikram Pratap SinghNoch keine Bewertungen

- Goods and Service DesignDokument3 SeitenGoods and Service DesignNayab NoumanNoch keine Bewertungen

- Diversification in The Context of Growth StrategiesDokument10 SeitenDiversification in The Context of Growth StrategieskavenNoch keine Bewertungen

- CHP 13 - Pricing Decisions, Target Costing, Product Life-Cycle Costing (With Answers)Dokument64 SeitenCHP 13 - Pricing Decisions, Target Costing, Product Life-Cycle Costing (With Answers)kenchong715Noch keine Bewertungen

- Strategic Cost ManagementDokument24 SeitenStrategic Cost Managementsai500Noch keine Bewertungen

- Forecasting Techniques: Production and Operations in ManagementDokument71 SeitenForecasting Techniques: Production and Operations in Managementsiddhartha chpeuriNoch keine Bewertungen

- Global SourcingDokument50 SeitenGlobal SourcingJason Chen100% (1)

- Chap 009Dokument69 SeitenChap 009Brey Callao0% (1)

- Collier and Evans Operations Management Chapter 7Dokument37 SeitenCollier and Evans Operations Management Chapter 7Omar100% (1)

- Managerial Accounting STANDARDDokument37 SeitenManagerial Accounting STANDARDCyn SyjucoNoch keine Bewertungen

- The Internal Environment:: Resources, Capabilities, and Core CompetenciesDokument17 SeitenThe Internal Environment:: Resources, Capabilities, and Core CompetenciesshivaniNoch keine Bewertungen

- Facility Layout NotesDokument6 SeitenFacility Layout NotesOckouri BarnesNoch keine Bewertungen

- Slm-Strategic Financial Management - 0 PDFDokument137 SeitenSlm-Strategic Financial Management - 0 PDFdadapeer h mNoch keine Bewertungen

- Aggregate PlanningDokument14 SeitenAggregate Planningshoaib_ulhaqNoch keine Bewertungen

- Definition and Objectives of BookkeepingDokument6 SeitenDefinition and Objectives of BookkeepingmlumeNoch keine Bewertungen

- Make or Buy DecisionDokument34 SeitenMake or Buy DecisionHalimah Hamzah75% (4)

- Decision-Making Using Marginal Costing-IDokument11 SeitenDecision-Making Using Marginal Costing-Iapi-27014089100% (3)

- What Is Push and Pull Strategy in Supply Chain ManagementDokument4 SeitenWhat Is Push and Pull Strategy in Supply Chain Managementnivedita vermaNoch keine Bewertungen

- Chap013 Relevant Costs For Decision MakingDokument18 SeitenChap013 Relevant Costs For Decision MakingMalak Kinaan100% (2)

- Demand Planning & ForecastingDokument34 SeitenDemand Planning & ForecastingDebashishDolonNoch keine Bewertungen

- Chapter 02 International Logistics 1Dokument41 SeitenChapter 02 International Logistics 1Marcia PattersonNoch keine Bewertungen

- TLG SolutionsDokument22 SeitenTLG SolutionsDV Villan71% (7)

- Cost of ProductionDokument11 SeitenCost of Productionsajid93100% (2)

- How To Prepare A Cash Flow StatementDokument8 SeitenHow To Prepare A Cash Flow Statementk4kazim100% (8)

- Absorption and Variable Costing Income Statement: Reporter: Sharmaine Laye M. PascualDokument20 SeitenAbsorption and Variable Costing Income Statement: Reporter: Sharmaine Laye M. PascualPatrick LanceNoch keine Bewertungen

- Short Run Decision AnalysisDokument31 SeitenShort Run Decision AnalysisMedhaSaha100% (1)

- 7-Eleven Ashraf AssignmentDokument6 Seiten7-Eleven Ashraf AssignmentLaila RashedNoch keine Bewertungen

- CHP 10 - SourcingDokument16 SeitenCHP 10 - SourcingStacy MitchellNoch keine Bewertungen

- DriveCompatibility WikiDokument1 SeiteDriveCompatibility Wikishida67Noch keine Bewertungen

- Sean DeCraneDokument59 SeitenSean DeCraneMujeeb Ur Rehman KhalilNoch keine Bewertungen

- StartupDokument2 SeitenStartupRoobendhiran SethuramanNoch keine Bewertungen

- B06 HydroProfiler-M eDokument2 SeitenB06 HydroProfiler-M eJamjamNoch keine Bewertungen

- General Concepts and Historical Antecedents of Science and TechnologyDokument20 SeitenGeneral Concepts and Historical Antecedents of Science and TechnologyZarina PajarillagaNoch keine Bewertungen

- Aeg DC 2000 enDokument2 SeitenAeg DC 2000 enmauriceauNoch keine Bewertungen

- Abhishek Aggarwal SEO Specialist Updated CV - 1 3Dokument3 SeitenAbhishek Aggarwal SEO Specialist Updated CV - 1 3dilsonenterprises2022Noch keine Bewertungen

- Power Decoupling Method For Single Stage Current Fed Flyback Micro InverterDokument41 SeitenPower Decoupling Method For Single Stage Current Fed Flyback Micro InverterXavier ANoch keine Bewertungen

- Codigo Cummins c-FMI-PID-SID-1Dokument35 SeitenCodigo Cummins c-FMI-PID-SID-1Claudivan FreitasNoch keine Bewertungen

- Vietnam Digital Behaviors and Trends 2020 - GWIDokument7 SeitenVietnam Digital Behaviors and Trends 2020 - GWITRAN LE LAM HOANGNoch keine Bewertungen

- Commercializing Process TechnologiesDokument11 SeitenCommercializing Process TechnologiesBramJanssen76Noch keine Bewertungen

- Asphalt and Asphalt Mixtures PPT2023Dokument53 SeitenAsphalt and Asphalt Mixtures PPT2023Brian ReyesNoch keine Bewertungen

- Aluminium ProfileDokument23 SeitenAluminium ProfileRobert CedeñoNoch keine Bewertungen

- What Is The Difference Between 0.2 and 0.2S Class CTDokument5 SeitenWhat Is The Difference Between 0.2 and 0.2S Class CTshaik abdulaleemNoch keine Bewertungen

- CV NguyenLamTruong EngNew PDFDokument1 SeiteCV NguyenLamTruong EngNew PDFhoa leNoch keine Bewertungen

- Airbus Supplier Approval List September 2014Dokument57 SeitenAirbus Supplier Approval List September 2014adip1971890Noch keine Bewertungen

- Technology in The Construction IndustryDokument5 SeitenTechnology in The Construction IndustryGiancarlo GonzagaNoch keine Bewertungen

- Bluetooth Low Energy Device: Using The MT8852B To Test A Controlled Through A Proprietary InterfaceDokument7 SeitenBluetooth Low Energy Device: Using The MT8852B To Test A Controlled Through A Proprietary InterfaceAlberto SaldivarNoch keine Bewertungen

- StdlinearcrossDokument50 SeitenStdlinearcrossKostas KitharidisNoch keine Bewertungen

- PC57 12 91 PDFDokument2 SeitenPC57 12 91 PDFAlexander Cortez EspinozaNoch keine Bewertungen

- Omron G8P 114P FD US DC12 DatasheetDokument6 SeitenOmron G8P 114P FD US DC12 DatasheetCorretaje ResidencialNoch keine Bewertungen

- PalcoControl CP en PDFDokument7 SeitenPalcoControl CP en PDFsulthan ariffNoch keine Bewertungen

- How To Build Your Own Blog With Next - Js and MDXDokument5 SeitenHow To Build Your Own Blog With Next - Js and MDXVinh Quang NguyễnNoch keine Bewertungen

- WPS, PQR, WPQDokument2 SeitenWPS, PQR, WPQESL100% (1)

- MasterFormat - Wikipedia, The Free EncyclopediaDokument3 SeitenMasterFormat - Wikipedia, The Free EncyclopediaMartin SabahNoch keine Bewertungen

- A3-PageWide F2F Deck 2 28 17 final-ENDokument129 SeitenA3-PageWide F2F Deck 2 28 17 final-ENkadirNoch keine Bewertungen

- Hype Cycle For The Telecommu 260996Dokument102 SeitenHype Cycle For The Telecommu 260996Enrique de la RosaNoch keine Bewertungen

- Downloaded From Manuals Search Engine: NOKIA 6820Dokument121 SeitenDownloaded From Manuals Search Engine: NOKIA 6820okamiotokoNoch keine Bewertungen

- Chapter 01Dokument62 SeitenChapter 01Rap JaviniarNoch keine Bewertungen

- TNS Earthing System A Useful GuideDokument5 SeitenTNS Earthing System A Useful GuideVirgilioNoch keine Bewertungen