Das könnte Ihnen auch gefallen

- The Great Recession: The burst of the property bubble and the excesses of speculationVon EverandThe Great Recession: The burst of the property bubble and the excesses of speculationNoch keine Bewertungen

- Subprime FinalDokument34 SeitenSubprime Finalapi-3712367Noch keine Bewertungen

- Investing in Fixed Income Securities: Understanding the Bond MarketVon EverandInvesting in Fixed Income Securities: Understanding the Bond MarketNoch keine Bewertungen

- Krassimir Petrov - Intto To Credit Default SwapsDokument13 SeitenKrassimir Petrov - Intto To Credit Default SwapsAntonio Luis SantosNoch keine Bewertungen

- Subprime Crisis: Sandipan Nandi Shamik Roy Uttiya DasDokument61 SeitenSubprime Crisis: Sandipan Nandi Shamik Roy Uttiya DasUttiya DasNoch keine Bewertungen

- Risk Management Failures During The Financial Crisis: November 2011Dokument27 SeitenRisk Management Failures During The Financial Crisis: November 2011Khushi ShahNoch keine Bewertungen

- SecuritizationDokument34 SeitenSecuritizationsanil mehtaNoch keine Bewertungen

- Sub-Prime Loans ExplainedDokument16 SeitenSub-Prime Loans ExplainedDavneet KaurNoch keine Bewertungen

- Financial System, Money and Prices ExplainedDokument9 SeitenFinancial System, Money and Prices ExplainedljayoungNoch keine Bewertungen

- Our Team Agenda Securitization CDS CDO LiquidityDokument81 SeitenOur Team Agenda Securitization CDS CDO Liquidityshwetata986Noch keine Bewertungen

- Financial Crises Causes and EffectsDokument6 SeitenFinancial Crises Causes and EffectsSorah YoriNoch keine Bewertungen

- Ultimate Guide To Debt & Leveraged Finance - Wall Street PrepDokument18 SeitenUltimate Guide To Debt & Leveraged Finance - Wall Street PrepPearson SunigaNoch keine Bewertungen

- The Investment Function in BankingDokument20 SeitenThe Investment Function in BankingJahidul IslamNoch keine Bewertungen

- A Tale of Two Hedge FundsDokument18 SeitenA Tale of Two Hedge Fundsshreyansh12067% (3)

- A Tale of Two Hedge FundsDokument17 SeitenA Tale of Two Hedge FundsS Sarkar100% (1)

- Sub-Prime Crisis and Its AftermathDokument24 SeitenSub-Prime Crisis and Its AftermathasifanisNoch keine Bewertungen

- Topic 10 Commercial Bank OperationsDokument23 SeitenTopic 10 Commercial Bank OperationsKelly Chan Yun JieNoch keine Bewertungen

- What Is The Main Function of Financial Markets?: Tutorial 1 Overview of Financial System Part 1. Questions For ReviewDokument16 SeitenWhat Is The Main Function of Financial Markets?: Tutorial 1 Overview of Financial System Part 1. Questions For ReviewViem AnhNoch keine Bewertungen

- What Are Money Markets?: They Provide A Means For Lenders and Borrowers To Satisfy Their Short-Term Financial NeedsDokument2 SeitenWhat Are Money Markets?: They Provide A Means For Lenders and Borrowers To Satisfy Their Short-Term Financial NeedsAbhishek GavandeNoch keine Bewertungen

- Inside Job documentary summary and key questionsDokument6 SeitenInside Job documentary summary and key questionsJill SanghrajkaNoch keine Bewertungen

- The Current Turmoil Cause and EffectDokument32 SeitenThe Current Turmoil Cause and Effectyerramr7218Noch keine Bewertungen

- ProjectDokument7 SeitenProjectmalik waseemNoch keine Bewertungen

- Module 7 Managing The Securities Portfolio: Short Term InstrumentsDokument10 SeitenModule 7 Managing The Securities Portfolio: Short Term InstrumentsAnna-Clara MansolahtiNoch keine Bewertungen

- Mortgage Credit CrisisDokument5 SeitenMortgage Credit Crisisasfand yar waliNoch keine Bewertungen

- Sub PrimeDokument7 SeitenSub PrimeAtul SuranaNoch keine Bewertungen

- How Destruction Happened?: FICO Score S of Below 620. Because TheseDokument5 SeitenHow Destruction Happened?: FICO Score S of Below 620. Because ThesePramod KhandelwalNoch keine Bewertungen

- Notes On Basel IIIDokument11 SeitenNotes On Basel IIIprat05Noch keine Bewertungen

- FRM Part 1 R7Dokument2 SeitenFRM Part 1 R7Tony NasrNoch keine Bewertungen

- Why Study Financial Markets? Financial Markets, Such As Bond and Stock Markets, Are Crucial in Our EconomyDokument27 SeitenWhy Study Financial Markets? Financial Markets, Such As Bond and Stock Markets, Are Crucial in Our EconomyShaheena SanaNoch keine Bewertungen

- Finance Assignment 2: Financial Crisis of 2008: Housing Market in USADokument2 SeitenFinance Assignment 2: Financial Crisis of 2008: Housing Market in USADipankar BasumataryNoch keine Bewertungen

- Tutorial 1 QuestionsDokument8 SeitenTutorial 1 QuestionsHuế HoàngNoch keine Bewertungen

- Why Perpetual Bonds' Are Rocking Credit Markets - QuickTake - BloombergDokument4 SeitenWhy Perpetual Bonds' Are Rocking Credit Markets - QuickTake - BloombergLow chee weiNoch keine Bewertungen

- ING Trups DiagramDokument5 SeitenING Trups DiagramhungrymonsterNoch keine Bewertungen

- Submission Number: 1 Group Number: 34 Group Members: Non-Contributing Member (X)Dokument5 SeitenSubmission Number: 1 Group Number: 34 Group Members: Non-Contributing Member (X)Darshna JhaNoch keine Bewertungen

- Chapter Two Sources of FinanceDokument12 SeitenChapter Two Sources of Financekuttan1000100% (1)

- Sub Prime Overview For Samir 1 Final 97-2003 FormatDokument10 SeitenSub Prime Overview For Samir 1 Final 97-2003 FormatAliasgar SuratwalaNoch keine Bewertungen

- Financial Crises: Past, Present and Future: James J. Angel, PHD, Cfa Georgetown University Mcdonough School of BusinessDokument39 SeitenFinancial Crises: Past, Present and Future: James J. Angel, PHD, Cfa Georgetown University Mcdonough School of BusinessnitikanNoch keine Bewertungen

- Securitizacion Primer (Scotia Capital)Dokument14 SeitenSecuritizacion Primer (Scotia Capital)gastonriosNoch keine Bewertungen

- Group 6: by - Garvit Agarwal Gyan Prakash Karan Gupta Ravikumar Soni Sahil SinglaDokument21 SeitenGroup 6: by - Garvit Agarwal Gyan Prakash Karan Gupta Ravikumar Soni Sahil SinglaSahil SinglaNoch keine Bewertungen

- Financial Markets OverviewDokument25 SeitenFinancial Markets OverviewTACN-4TC-19ACN Nguyen Thu HienNoch keine Bewertungen

- Fear of Fire Sales and The Credit FreezeDokument35 SeitenFear of Fire Sales and The Credit Freezesxyang97Noch keine Bewertungen

- Bonds: (Pakistan) (00923013791119)Dokument31 SeitenBonds: (Pakistan) (00923013791119)chelsea1989Noch keine Bewertungen

- Bond, Stock and Mortgage MarketsDokument16 SeitenBond, Stock and Mortgage MarketsFaisal NaqviNoch keine Bewertungen

- Crisis FinancieraDokument4 SeitenCrisis Financierahawk91Noch keine Bewertungen

- Assignment# 1: Name: Muhammad Ali Adil Malik REG #: SP16-BAF-015 Instructor: Dr. Sabeen KhanDokument5 SeitenAssignment# 1: Name: Muhammad Ali Adil Malik REG #: SP16-BAF-015 Instructor: Dr. Sabeen KhanAli MalikNoch keine Bewertungen

- US Subprime Crisis (In Layman Terms)Dokument4 SeitenUS Subprime Crisis (In Layman Terms)Vipul GuptaNoch keine Bewertungen

- Home Assignment - JUNK BOND Subject: Corporate FinanceDokument3 SeitenHome Assignment - JUNK BOND Subject: Corporate FinanceAsad Mazhar100% (1)

- Financial Imst &mark Unit - 2Dokument57 SeitenFinancial Imst &mark Unit - 2KalkayeNoch keine Bewertungen

- Money MarketDokument32 SeitenMoney MarketHabyarimana ProjecteNoch keine Bewertungen

- Depository Institutions: Activities and Characteristics: Instructor: Mahwish KhokharDokument36 SeitenDepository Institutions: Activities and Characteristics: Instructor: Mahwish KhokharAbdur RehmanNoch keine Bewertungen

- International Finance FinalDokument27 SeitenInternational Finance FinalRishabh RaiNoch keine Bewertungen

- Topic 5 Money MarketsDokument21 SeitenTopic 5 Money MarketsKelly Chan Yun JieNoch keine Bewertungen

- Chapter 1: Roles of Financial Markets and InstitutionsDokument36 SeitenChapter 1: Roles of Financial Markets and InstitutionsDương Nguyễn TùngNoch keine Bewertungen

- Short Answer QuestionsDokument8 SeitenShort Answer QuestionsBách PhạmNoch keine Bewertungen

- How MBS, CDOs and CDS Contributed to the 2008 Housing CrisisDokument5 SeitenHow MBS, CDOs and CDS Contributed to the 2008 Housing CrisisАлександр НефедовNoch keine Bewertungen

- Financial Innovation in The Mortgage MarketsDokument4 SeitenFinancial Innovation in The Mortgage MarketsRonald Samuel GozaliNoch keine Bewertungen

- Money Market vs. Capital Market: What Is Money Markets?Dokument4 SeitenMoney Market vs. Capital Market: What Is Money Markets?Ash imoNoch keine Bewertungen

- The Role of CDOs in Subprime CrisisDokument6 SeitenThe Role of CDOs in Subprime CrisisKunal BhodiaNoch keine Bewertungen

- Lecture Notes IDokument26 SeitenLecture Notes IdfbeNoch keine Bewertungen

- U. S. Loan Syndications: Chris Droussiotis Spring 2010Dokument37 SeitenU. S. Loan Syndications: Chris Droussiotis Spring 2010Ash_ish_vNoch keine Bewertungen

- 8086 Cpu ArchitectureDokument9 Seiten8086 Cpu Architectureapi-371236783% (6)

- L & TDokument9 SeitenL & Tapi-3712367Noch keine Bewertungen

- Policybrief Nov05Dokument6 SeitenPolicybrief Nov05api-3712367Noch keine Bewertungen

- Manging Foreign ExchnageDokument6 SeitenManging Foreign Exchnageapi-3712367Noch keine Bewertungen

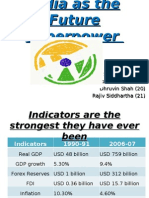

- India As SuperpowerDokument21 SeitenIndia As Superpowerapi-3712367Noch keine Bewertungen

- Macroeconomics AssignmentsDokument15 SeitenMacroeconomics Assignmentsapi-3712367Noch keine Bewertungen

- Anti-Inflationary Policy in IndiaDokument14 SeitenAnti-Inflationary Policy in Indiaapi-3712367Noch keine Bewertungen

- WEight Training ScheduleDokument2 SeitenWEight Training Scheduleapi-3712367100% (1)

- Fiscal Deficit 2003 FormatDokument19 SeitenFiscal Deficit 2003 Formatapi-3712367Noch keine Bewertungen

- Manging Foreign ExchnageDokument6 SeitenManging Foreign Exchnageapi-3712367Noch keine Bewertungen

- 72903Dokument11 Seiten72903api-3712367Noch keine Bewertungen

- Report OnDokument9 SeitenReport Onapi-3712367Noch keine Bewertungen

- Just in TimeDokument3 SeitenJust in Timeapi-3712367Noch keine Bewertungen

- Macro Economics OutlineDokument2 SeitenMacro Economics Outlineapi-3712367100% (1)

- FFRChange HistoryDokument1 SeiteFFRChange Historyapi-3712367Noch keine Bewertungen

- Foreign Exchange Management Policy in IndiaDokument6 SeitenForeign Exchange Management Policy in Indiaapi-371236767% (3)

- Fema CDokument5 SeitenFema Capi-3712367Noch keine Bewertungen

- FOREX Management Versus SingaporeDokument3 SeitenFOREX Management Versus Singaporeapi-3712367Noch keine Bewertungen

- D&B Economy Observer November 07Dokument3 SeitenD&B Economy Observer November 07api-3712367Noch keine Bewertungen

- US Subprime 070817Dokument6 SeitenUS Subprime 070817api-3712367Noch keine Bewertungen

- Sebi TocDokument33 SeitenSebi Tocapi-3712367Noch keine Bewertungen

- BSC & Knowledge ManagementDokument3 SeitenBSC & Knowledge Managementapi-3712367100% (1)

- Subprime Toxic Debt - Bloomberg July07Dokument10 SeitenSubprime Toxic Debt - Bloomberg July07api-3712367Noch keine Bewertungen

- Global Economics - IndiaDokument2 SeitenGlobal Economics - Indiaapi-3712367Noch keine Bewertungen

- Balanced ScorecardDokument13 SeitenBalanced Scorecardapi-3712367Noch keine Bewertungen

- SubPrime Mortgage MarketDokument6 SeitenSubPrime Mortgage Marketapi-3712367Noch keine Bewertungen

- Balanced Scorecard Elearning - PresentationDokument39 SeitenBalanced Scorecard Elearning - Presentationapi-3712367Noch keine Bewertungen

- Balanced Scorecard 02Dokument7 SeitenBalanced Scorecard 02api-3712367100% (2)