Das könnte Ihnen auch gefallen

- Managerial Economics & Business StrategyDokument23 SeitenManagerial Economics & Business StrategySuryadyDarsonoNoch keine Bewertungen

- Cost of CapitalDokument37 SeitenCost of Capitalrajthakre81Noch keine Bewertungen

- Mergers and AcquisitionsDokument39 SeitenMergers and Acquisitions202110782Noch keine Bewertungen

- Wa0005Dokument16 SeitenWa0005Timothy Manyungwa IsraelNoch keine Bewertungen

- Goals, Values and Performance: OutlineDokument15 SeitenGoals, Values and Performance: OutlineNarayanan SubramanianNoch keine Bewertungen

- MBA 290 Strategic AnalysisDokument110 SeitenMBA 290 Strategic AnalysisLynette TangNoch keine Bewertungen

- Effects of Dividends On Common Stock Prices: The Nepalese EvidenceDokument33 SeitenEffects of Dividends On Common Stock Prices: The Nepalese EvidenceShreeja DhungelNoch keine Bewertungen

- Lesson 09 Dividend PolicyDokument35 SeitenLesson 09 Dividend PolicyTomy BoscoNoch keine Bewertungen

- FMDokument45 SeitenFMSaumya GoelNoch keine Bewertungen

- Relative ValuationDokument29 SeitenRelative ValuationCheTanBonDardeNoch keine Bewertungen

- Mergers and AcquistionsDokument29 SeitenMergers and AcquistionsAli HussainNoch keine Bewertungen

- Goals, Values and PerformanceDokument13 SeitenGoals, Values and PerformanceNarayanan SubramanianNoch keine Bewertungen

- Risk and Return: Roslina BT AmeerudinDokument58 SeitenRisk and Return: Roslina BT AmeerudinRenese LeeNoch keine Bewertungen

- The Fundamentals of Managerial Economics: Dr. Abdullah M. Al-AnsiDokument30 SeitenThe Fundamentals of Managerial Economics: Dr. Abdullah M. Al-AnsiEbrar AnsiNoch keine Bewertungen

- Advanced Strategic ManagementDokument110 SeitenAdvanced Strategic ManagementDr Rushen SinghNoch keine Bewertungen

- ProductDokument12 SeitenProductHassanNoch keine Bewertungen

- MBA 290-Strategic AnalysisDokument110 SeitenMBA 290-Strategic AnalysisAbhishek SoniNoch keine Bewertungen

- Ch11-Valuation of SecuritiesDokument94 SeitenCh11-Valuation of SecuritiesRaiHan AbeDinNoch keine Bewertungen

- Scott 7e 2015 Chapter 05 The Value Relevance of Accounting InformationDokument26 SeitenScott 7e 2015 Chapter 05 The Value Relevance of Accounting InformationWiday Wijaksana100% (1)

- Lec 4Dokument19 SeitenLec 4WEI JUN CHONGNoch keine Bewertungen

- ValuationDokument41 SeitenValuationjpc jpcNoch keine Bewertungen

- Mba 290-Strategic AnalysisDokument110 SeitenMba 290-Strategic Analysisabdelkadera257Noch keine Bewertungen

- Chapter One: Introduction To Managerial EconomicsDokument36 SeitenChapter One: Introduction To Managerial Economicsmaria rafiqNoch keine Bewertungen

- Part 4 - Strategy and M and A Fall 2021Dokument31 SeitenPart 4 - Strategy and M and A Fall 2021Đức HuyNoch keine Bewertungen

- Lordina - Mergers and Corporate ControlDokument57 SeitenLordina - Mergers and Corporate ControlDolly AdwoaNoch keine Bewertungen

- Objective of A FirmDokument35 SeitenObjective of A FirmShibin PaulNoch keine Bewertungen

- Nature and Scope of Managerial EconomicsDokument26 SeitenNature and Scope of Managerial EconomicsPawan KumarNoch keine Bewertungen

- FM2 Project1 Sec01 Grp7Dokument8 SeitenFM2 Project1 Sec01 Grp7Vineet KhandelwalNoch keine Bewertungen

- Chapter 01 Introduction To M and ADokument28 SeitenChapter 01 Introduction To M and ASattagouda M PatilNoch keine Bewertungen

- Mergers and Acquisitions PDFDokument65 SeitenMergers and Acquisitions PDFAhmad QuNoch keine Bewertungen

- Economics For Managers: Session 1 The Fundamentals of Managerial EconomicsDokument24 SeitenEconomics For Managers: Session 1 The Fundamentals of Managerial EconomicsVipulNoch keine Bewertungen

- Equity Valuation ModelsDokument58 SeitenEquity Valuation ModelsSarang GuptaNoch keine Bewertungen

- Chapter 2 - Tutorial Solutions - 2023Dokument20 SeitenChapter 2 - Tutorial Solutions - 2023Jared HerberNoch keine Bewertungen

- GulfDokument17 SeitenGulfmastermind_2848154Noch keine Bewertungen

- Nike Case AnalysisDokument9 SeitenNike Case AnalysisUyen Thao Dang96% (54)

- Mark Plan and Examiner'S Commentary: Total Marks: General CommentsDokument11 SeitenMark Plan and Examiner'S Commentary: Total Marks: General CommentsPAul De BorjaNoch keine Bewertungen

- 2015 Chapter 05-Ppt Scot Bab 5Dokument26 Seiten2015 Chapter 05-Ppt Scot Bab 5AGANoch keine Bewertungen

- Mark Scheme (Results) Summer 2019Dokument18 SeitenMark Scheme (Results) Summer 2019Hadeel DossaNoch keine Bewertungen

- Investment Analysis and Portfolio Management: Frank K. Reilly & Keith C. BrownDokument122 SeitenInvestment Analysis and Portfolio Management: Frank K. Reilly & Keith C. BrownWhy you want to knowNoch keine Bewertungen

- Relative ValuationDokument29 SeitenRelative ValuationOnal RautNoch keine Bewertungen

- BP Dividend Valuation FinancingDokument31 SeitenBP Dividend Valuation FinancingTowhidul IslamNoch keine Bewertungen

- Investment Analysis and Portfolio Management: Lecture Presentation SoftwareDokument118 SeitenInvestment Analysis and Portfolio Management: Lecture Presentation SoftwarekegnataNoch keine Bewertungen

- Advanced Final Management Final ExamDokument9 SeitenAdvanced Final Management Final Examgatete samNoch keine Bewertungen

- Mergers & Acquisitions: M&A SynergyDokument21 SeitenMergers & Acquisitions: M&A SynergyNông Đức MinhNoch keine Bewertungen

- Finance For Non-Finance PeopleDokument41 SeitenFinance For Non-Finance Peopleayman.elnajjar8916100% (3)

- Mergers and AcquisitionsDokument41 SeitenMergers and Acquisitionskrishna priyaNoch keine Bewertungen

- Review Session 01 MA Concept Review Section2Dokument20 SeitenReview Session 01 MA Concept Review Section2misalNoch keine Bewertungen

- An Overview of Financial ManagementDokument46 SeitenAn Overview of Financial ManagementKiran IfciNoch keine Bewertungen

- Pricing Decisions: By: DR Shahinaz AbdellatifDokument30 SeitenPricing Decisions: By: DR Shahinaz AbdellatifEman EmyNoch keine Bewertungen

- Mergers and Acquisitions: TodayDokument29 SeitenMergers and Acquisitions: TodayKrisna AdiputeraNoch keine Bewertungen

- Sesi01 Dasar Ekonomi ManajerialDokument26 SeitenSesi01 Dasar Ekonomi ManajerialjuwelismailNoch keine Bewertungen

- BM Summer 14 MSDokument10 SeitenBM Summer 14 MSrohinNoch keine Bewertungen

- D23 FM Examiner's ReportDokument20 SeitenD23 FM Examiner's ReportEshal KhanNoch keine Bewertungen

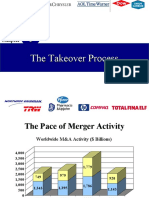

- The Takeover ProcessDokument12 SeitenThe Takeover ProcessNiken PermataNoch keine Bewertungen

- 01 FM&I Chap 7 Part 2 Stock MKTDokument89 Seiten01 FM&I Chap 7 Part 2 Stock MKTHoàng Lan AnhNoch keine Bewertungen

- Overview of PortfolioDokument22 SeitenOverview of PortfolioLindsay DavisNoch keine Bewertungen

- The Key to Higher Profits: Pricing PowerVon EverandThe Key to Higher Profits: Pricing PowerBewertung: 5 von 5 Sternen5/5 (1)

- Applied Corporate Finance. What is a Company worth?Von EverandApplied Corporate Finance. What is a Company worth?Bewertung: 3 von 5 Sternen3/5 (2)

- 5850 Ec225 06 Class ScheduleDokument1 Seite5850 Ec225 06 Class Scheduleapi-3699305Noch keine Bewertungen

- 6123 TitlesDokument1 Seite6123 Titlesapi-3699305Noch keine Bewertungen

- 5938 ExeccompepwpaperDokument35 Seiten5938 Execcompepwpaperapi-3699305Noch keine Bewertungen

- 5691 EC225CourseOutline06-07Dokument2 Seiten5691 EC225CourseOutline06-07api-3699305Noch keine Bewertungen

- 5688 AshishnarainparticipationDokument27 Seiten5688 Ashishnarainparticipationapi-3699305Noch keine Bewertungen

- 5691 EC225CourseOutline06-07Dokument2 Seiten5691 EC225CourseOutline06-07api-3699305Noch keine Bewertungen

- 5687 MaitreyidaspaperoncasteDokument18 Seiten5687 Maitreyidaspaperoncasteapi-3699305Noch keine Bewertungen

- Lecture 5 IIMC M & ADokument23 SeitenLecture 5 IIMC M & Aapi-3699305Noch keine Bewertungen

- 6767 Merger Intro Lecture1Dokument32 Seiten6767 Merger Intro Lecture1api-3699305Noch keine Bewertungen

- 5686 LabourarticleDokument27 Seiten5686 Labourarticleapi-3699305Noch keine Bewertungen

- 6767 Merger Intro Lecture1Dokument32 Seiten6767 Merger Intro Lecture1api-3699305Noch keine Bewertungen

- 6769 - Merger Lect 3Dokument21 Seiten6769 - Merger Lect 3api-3699305Noch keine Bewertungen

- 5681 teachertruancyBASUDokument16 Seiten5681 teachertruancyBASUapi-3699305Noch keine Bewertungen

- 5685 Helpingorhurtingworkersahmad&pagespaperDokument54 Seiten5685 Helpingorhurtingworkersahmad&pagespaperapi-3699305Noch keine Bewertungen

- Merger Tactics Lecture2Dokument18 SeitenMerger Tactics Lecture2api-3699305Noch keine Bewertungen

- Large ShareholderDokument4 SeitenLarge Shareholderapi-3699305Noch keine Bewertungen

- Lecture 4 Iimc M&aDokument18 SeitenLecture 4 Iimc M&aapi-3699305Noch keine Bewertungen

- 6771 - Lecture 4 Iimc M&aDokument18 Seiten6771 - Lecture 4 Iimc M&aapi-3699305Noch keine Bewertungen

- 6886 Valuation 2Dokument25 Seiten6886 Valuation 2api-3699305100% (1)

- 6560 LectureDokument36 Seiten6560 Lectureapi-3699305100% (1)

- 6769 - Merger Lect 3Dokument21 Seiten6769 - Merger Lect 3api-3699305Noch keine Bewertungen

- 6885 Valuation 1Dokument24 Seiten6885 Valuation 1api-3699305Noch keine Bewertungen

- 6766 Merger Course06 BriefDokument2 Seiten6766 Merger Course06 Briefapi-3699305100% (1)

- 6516 TechnicalDokument33 Seiten6516 Technicalapi-3699305Noch keine Bewertungen

- 6473 LectureDokument13 Seiten6473 Lectureapi-3699305Noch keine Bewertungen

- IAPMDokument4 SeitenIAPMapi-3699305Noch keine Bewertungen

- A Smarter Computer To Pick Stocks: Microsoft Nasdaq Bill GatesDokument5 SeitenA Smarter Computer To Pick Stocks: Microsoft Nasdaq Bill Gatesapi-3699305Noch keine Bewertungen

- 6536 LectureDokument16 Seiten6536 Lectureapi-3699305100% (1)

- 6475 LectureDokument6 Seiten6475 Lectureapi-3699305Noch keine Bewertungen

- Comparative Study of Rural & Urban Consumer BehaviorDokument65 SeitenComparative Study of Rural & Urban Consumer BehaviorPrachi More0% (1)

- MLRO - Questions of Strategy in Indian RevolutionDokument29 SeitenMLRO - Questions of Strategy in Indian RevolutionBrian GarciaNoch keine Bewertungen

- Praneeth AppointmentDokument2 SeitenPraneeth AppointmentashaswamyNoch keine Bewertungen

- LLB Banking NotesDokument14 SeitenLLB Banking Notesjagankilari80% (5)

- MoaDokument5 SeitenMoaRaghvirNoch keine Bewertungen

- Introduction To Business Case Study Report About SainsburysDokument13 SeitenIntroduction To Business Case Study Report About Sainsburysahsan_ch786100% (1)

- Hershey v. LBB ImportsDokument50 SeitenHershey v. LBB ImportsMark JaffeNoch keine Bewertungen

- Audit of Expenditure CycleDokument3 SeitenAudit of Expenditure CycleFreddie RevillozaNoch keine Bewertungen

- Nationwide IULDokument20 SeitenNationwide IULdjdazedNoch keine Bewertungen

- NAKAMURA LACQUER COMPANY 1 VerticleDokument10 SeitenNAKAMURA LACQUER COMPANY 1 Verticlevinay tembhurneNoch keine Bewertungen

- Benchmarking: Strategies For Product DevelopmentDokument27 SeitenBenchmarking: Strategies For Product DevelopmentVinoth RajaNoch keine Bewertungen

- Chinese Accounting VocabDokument3 SeitenChinese Accounting Vocabzsuzsaprivate7365100% (1)

- Heidi RoizenDokument2 SeitenHeidi RoizenAthena ChowdhuryNoch keine Bewertungen

- Retail Strategic Planning and Operations ManagementDokument33 SeitenRetail Strategic Planning and Operations ManagementYash JashNoch keine Bewertungen

- A WorldDokument22 SeitenA Worldahmed100% (1)

- Fog ComputingDokument301 SeitenFog Computingorhema oluga100% (2)

- EC1301 Semester 1 Tutorial 2 Short Answer QuestionsDokument2 SeitenEC1301 Semester 1 Tutorial 2 Short Answer QuestionsShuMuKongNoch keine Bewertungen

- O&M PresentationDokument30 SeitenO&M Presentationdivyeshbalar100% (1)

- Keng Hua Paper Products Co. Inc. v. Court of AppealsDokument2 SeitenKeng Hua Paper Products Co. Inc. v. Court of Appealsyamaleihs100% (2)

- Harbor Research - Machine To Machine (M2M) & Smart Systems Market ForecastDokument13 SeitenHarbor Research - Machine To Machine (M2M) & Smart Systems Market ForecastharborresearchNoch keine Bewertungen

- Portfolio October To December 2011Dokument89 SeitenPortfolio October To December 2011rishad30Noch keine Bewertungen

- PhilAm LIFE vs. Secretary of Finance Case DigestDokument2 SeitenPhilAm LIFE vs. Secretary of Finance Case DigestDenn Reed Tuvera Jr.Noch keine Bewertungen

- Dabur StrategiesDokument4 SeitenDabur StrategiesNeha GillNoch keine Bewertungen

- DBA Weights-PowerShares ETFsDokument7 SeitenDBA Weights-PowerShares ETFsfredtag4393Noch keine Bewertungen

- Sales and Operations PlanningDokument17 SeitenSales and Operations PlanningcharlesNoch keine Bewertungen

- University of Bahrain College of Business Administration MKT268: Personal SellingDokument4 SeitenUniversity of Bahrain College of Business Administration MKT268: Personal Sellinghawra alkhawajaNoch keine Bewertungen

- Limited Liability Partnership 01111Dokument20 SeitenLimited Liability Partnership 01111Akhil khannaNoch keine Bewertungen

- Swot Analysis R&D: NPD Stages and ExplanationDokument3 SeitenSwot Analysis R&D: NPD Stages and ExplanationHarshdeep BhatiaNoch keine Bewertungen

- Safa Edited4Dokument17 SeitenSafa Edited4Stoic_SpartanNoch keine Bewertungen

- Step For Winding Up LLPDokument3 SeitenStep For Winding Up LLPCHUAN YONG TANNoch keine Bewertungen