Das könnte Ihnen auch gefallen

- Lubricants Some Straws in The Wind RSP GroupDokument20 SeitenLubricants Some Straws in The Wind RSP GroupChethaka Lankara SilvaNoch keine Bewertungen

- PSO Supply Chain ManagementDokument33 SeitenPSO Supply Chain Managementengr_asad36433% (3)

- Soujanya Castrol 1PB11MBA31Dokument22 SeitenSoujanya Castrol 1PB11MBA31soujanya_nagarajaNoch keine Bewertungen

- Ford PresentationDokument37 SeitenFord PresentationRasik Sawant100% (4)

- FlowServe CorporationDokument10 SeitenFlowServe CorporationraghavaneieNoch keine Bewertungen

- Future Outlook Indian Lub MarketDokument20 SeitenFuture Outlook Indian Lub MarketPrabhu AgrawalNoch keine Bewertungen

- Sinopec Case Study AnalysisDokument23 SeitenSinopec Case Study AnalysisAlok Jain100% (1)

- Sales Distribution Issues Indian Automotive LubricantsDokument8 SeitenSales Distribution Issues Indian Automotive Lubricantsbasaavan6274Noch keine Bewertungen

- Hascol Petroluem Limited: Submitted By: Zarmeena Gauhar Arooj Atiya Nosherwan ShafiqDokument6 SeitenHascol Petroluem Limited: Submitted By: Zarmeena Gauhar Arooj Atiya Nosherwan ShafiqZarmeenaGauharNoch keine Bewertungen

- Refining Margin Supplement OMRAUG 12SEP2012Dokument30 SeitenRefining Margin Supplement OMRAUG 12SEP2012Won JangNoch keine Bewertungen

- PSODokument21 SeitenPSOAsad Mazhar100% (1)

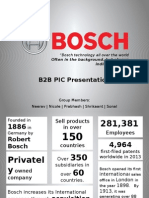

- B2B PIC Presentation: Often in The Background, But Always Indispensable."Dokument28 SeitenB2B PIC Presentation: Often in The Background, But Always Indispensable."KiaraSinghNoch keine Bewertungen

- Table of Contents:: Page NoDokument42 SeitenTable of Contents:: Page NoCh Arslan Bashir67% (3)

- BPCL Nit TrichyDokument34 SeitenBPCL Nit TrichyPradeep LionelNoch keine Bewertungen

- SWOT Analysis For Various IndustriesDokument21 SeitenSWOT Analysis For Various Industriesomkoted0% (1)

- Channel Conflict-Lubricant Markets-Petroleum IndustryDokument12 SeitenChannel Conflict-Lubricant Markets-Petroleum IndustryNikhil100% (1)

- E10 - Target Latin America, Middle East and Europe MarketsDokument9 SeitenE10 - Target Latin America, Middle East and Europe MarketsKush234Noch keine Bewertungen

- RIL - RPL MergerDokument13 SeitenRIL - RPL Mergermoduputhur7418Noch keine Bewertungen

- Case Study of Allwyn Nissan Limited and its Critical Success FactorsDokument58 SeitenCase Study of Allwyn Nissan Limited and its Critical Success FactorsJayesh VasavaNoch keine Bewertungen

- Ford PresentationDokument47 SeitenFord PresentationDIEGONoch keine Bewertungen

- Marico LTD.: ME Final Project PresentationDokument28 SeitenMarico LTD.: ME Final Project PresentationSaumitra AmbegaokarNoch keine Bewertungen

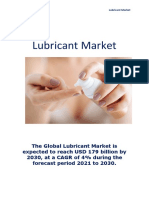

- Lubricant MarketDokument5 SeitenLubricant MarketsonaliwaghmareNoch keine Bewertungen

- Business Opportunities in The Emerging Lubricant Markets of South Asia, The Middle East, and Northern Africa, 2005-2015Dokument11 SeitenBusiness Opportunities in The Emerging Lubricant Markets of South Asia, The Middle East, and Northern Africa, 2005-2015Vishan SharmaNoch keine Bewertungen

- BASF PetrochemicalsDokument36 SeitenBASF PetrochemicalsAndrzej SzymańskiNoch keine Bewertungen

- Porter 5 Force FinalDokument35 SeitenPorter 5 Force FinalAbinash BiswalNoch keine Bewertungen

- Marketing PlanDokument8 SeitenMarketing PlanALOK THAKUR100% (9)

- Business EnvironmentDokument16 SeitenBusiness Environmentshakun_bansal7117Noch keine Bewertungen

- PSO PresentationDokument28 SeitenPSO PresentationRubina LakhaniNoch keine Bewertungen

- Future of POL RetailingDokument18 SeitenFuture of POL RetailingSuresh MalodiaNoch keine Bewertungen

- IOCL ReportDokument16 SeitenIOCL Reportmannu.abhimanyu309893% (14)

- BPCL Organization StructureDokument34 SeitenBPCL Organization StructureAroop Sanyal50% (10)

- Automotive Lubricants: Supply Chain ManagementDokument6 SeitenAutomotive Lubricants: Supply Chain ManagementMvb TradersNoch keine Bewertungen

- Petro Retailing BusinessDokument117 SeitenPetro Retailing BusinessPavan Kumar ChNoch keine Bewertungen

- Oil and Gas Sector NewDokument24 SeitenOil and Gas Sector NewApoorva PuranikNoch keine Bewertungen

- Supply Chain Process of HPCLDokument27 SeitenSupply Chain Process of HPCLAvinaba HazraNoch keine Bewertungen

- Automobile Sector Research ReportDokument15 SeitenAutomobile Sector Research ReportHitesh Thapar50% (2)

- Research and Analysis Project Toyota Indus Motors: Presented By: Murtaza GhaziDokument17 SeitenResearch and Analysis Project Toyota Indus Motors: Presented By: Murtaza Ghaziscrewyou098Noch keine Bewertungen

- A Project Report On On Indian Oil Out Lets and Bazzar Traders On Servo Lubricants at IOCLDokument58 SeitenA Project Report On On Indian Oil Out Lets and Bazzar Traders On Servo Lubricants at IOCLBabasab Patil (Karrisatte)Noch keine Bewertungen

- Jaguar Land Rover Industry AnalysisDokument16 SeitenJaguar Land Rover Industry AnalysisJacqueline StephenNoch keine Bewertungen

- Oil and Gas IndustryDokument50 SeitenOil and Gas IndustryFaig KarimliNoch keine Bewertungen

- Mba Finance Projet 23456789101112Dokument58 SeitenMba Finance Projet 23456789101112aryabhatmathsNoch keine Bewertungen

- Tiger AlloysDokument14 SeitenTiger AlloysharrylpuNoch keine Bewertungen

- Oil and GasDokument79 SeitenOil and GasSonali KadamNoch keine Bewertungen

- Strategic Marketing Assignment (Term-Vi) : Company Name: Indian Oil Corporation Limited (Iocl) Vertical: Servo LubricantsDokument8 SeitenStrategic Marketing Assignment (Term-Vi) : Company Name: Indian Oil Corporation Limited (Iocl) Vertical: Servo LubricantsAnik Chakraborty100% (1)

- Introduction to India's Oil and Gas IndustryDokument15 SeitenIntroduction to India's Oil and Gas IndustryMeena HarryNoch keine Bewertungen

- International Strategies: Current Scenario and Growth OptionsDokument22 SeitenInternational Strategies: Current Scenario and Growth OptionsVivek SinhaNoch keine Bewertungen

- Global Turbine Oil MarketDokument13 SeitenGlobal Turbine Oil MarketSanjay MatthewsNoch keine Bewertungen

- Lubricant Market Globe Vs IndiaDokument19 SeitenLubricant Market Globe Vs IndiaSandeep Walke100% (1)

- Overview of Energy Scenario WRT India: USA China Russian... Japan India Germany CanadaDokument7 SeitenOverview of Energy Scenario WRT India: USA China Russian... Japan India Germany CanadaAnirban PahariNoch keine Bewertungen

- 3 - Syntetic Pocket GuideDokument9 Seiten3 - Syntetic Pocket GuideRay Cepeda MenaNoch keine Bewertungen

- Petrol Saver-BBA-MBA Project ReportDokument52 SeitenPetrol Saver-BBA-MBA Project ReportpRiNcE DuDhAtRaNoch keine Bewertungen

- BMW SM CSDokument74 SeitenBMW SM CSWei Xun Chin100% (4)

- Indian Lube Industry: Key Players, Market Share & GrowthDokument14 SeitenIndian Lube Industry: Key Players, Market Share & GrowthSuresh MalodiaNoch keine Bewertungen

- Aftab - Husain Challenges of The Oil Refining Sector in PakistanDokument31 SeitenAftab - Husain Challenges of The Oil Refining Sector in PakistanMustafaNoch keine Bewertungen

- Edible Oil Industry Analysis: Key Trends, Players and OutlookDokument213 SeitenEdible Oil Industry Analysis: Key Trends, Players and OutlookRicha Bandra100% (1)

- Oil Well, Refinery Machinery & Equipment Wholesale Revenues World Summary: Market Values & Financials by CountryVon EverandOil Well, Refinery Machinery & Equipment Wholesale Revenues World Summary: Market Values & Financials by CountryNoch keine Bewertungen

- Petroleum Bulk Stations & Terminals Revenues World Summary: Market Values & Financials by CountryVon EverandPetroleum Bulk Stations & Terminals Revenues World Summary: Market Values & Financials by CountryNoch keine Bewertungen

- Chemicals & Allied Products Miscellaneous Wholesale Lines World Summary: Market Values & Financials by CountryVon EverandChemicals & Allied Products Miscellaneous Wholesale Lines World Summary: Market Values & Financials by CountryNoch keine Bewertungen

- Lubrication Tactics for Industries Made Simple, 8th Discipline of World Class Maintenance Management: 1, #6Von EverandLubrication Tactics for Industries Made Simple, 8th Discipline of World Class Maintenance Management: 1, #6Bewertung: 5 von 5 Sternen5/5 (1)

- Carburettors, Fuel Injection & Parts (Car OE & Aftermarket) World Summary: Market Values & Financials by CountryVon EverandCarburettors, Fuel Injection & Parts (Car OE & Aftermarket) World Summary: Market Values & Financials by CountryNoch keine Bewertungen

- Cheena Gas Service tax invoice for LPG cylinder refillDokument2 SeitenCheena Gas Service tax invoice for LPG cylinder refillEkta RaiNoch keine Bewertungen

- LPG Cooling and Re LiquefactionDokument2 SeitenLPG Cooling and Re Liquefactionawi610% (1)

- Design and Operation of LPG ShipsDokument476 SeitenDesign and Operation of LPG Shipsashwani chandraNoch keine Bewertungen

- Scope of Work 0Dokument87 SeitenScope of Work 0Emamoke100% (2)

- Standard Codes Followed in LPG IndustriesDokument41 SeitenStandard Codes Followed in LPG Industriesaarunsnair100% (2)

- PIP Accepted IdeasDokument9 SeitenPIP Accepted IdeasSuresh RamakrishnanNoch keine Bewertungen

- GP080 120VXDokument814 SeitenGP080 120VXSilvio0% (1)

- ARL Career DevelopmentDokument10 SeitenARL Career DevelopmentimranNoch keine Bewertungen

- Afe All PDFDokument10 SeitenAfe All PDFjigar patelNoch keine Bewertungen

- Studyguide BobtailDokument23 SeitenStudyguide BobtailVitor GS100% (1)

- API MPMS CatalogoDokument24 SeitenAPI MPMS CatalogoLionelinskiNoch keine Bewertungen

- Handling and Storage of Flammable Materials PDFDokument20 SeitenHandling and Storage of Flammable Materials PDFSheikh AzizNoch keine Bewertungen

- Welcome: One Day Seminar OnDokument47 SeitenWelcome: One Day Seminar Onshindesv2000Noch keine Bewertungen

- Operating Manual For LPG Recovery Unit No. 05/55: Persian Gulf Star Oil Company REF - No.: 3034-PR-MAN-AA020 (A0)Dokument105 SeitenOperating Manual For LPG Recovery Unit No. 05/55: Persian Gulf Star Oil Company REF - No.: 3034-PR-MAN-AA020 (A0)Behnam Ramouzeh100% (1)

- LPG cylinder manifold system components and accessoriesDokument12 SeitenLPG cylinder manifold system components and accessoriesShaaban Noaman100% (1)

- MQ 2 PDFDokument2 SeitenMQ 2 PDFSanjana SinghNoch keine Bewertungen

- Victrix-24-TT-2ErP - 1039151 - 003Dokument48 SeitenVictrix-24-TT-2ErP - 1039151 - 003Admin TestNoch keine Bewertungen

- Rrs-Group-Company-Profile PT - Raja Rafa SamudraDokument36 SeitenRrs-Group-Company-Profile PT - Raja Rafa SamudraYathi SyahriNoch keine Bewertungen

- Protect Environment Through Recycling & Planting TreesDokument2 SeitenProtect Environment Through Recycling & Planting TreesGeorge Anderson Loza FloresNoch keine Bewertungen

- LPG Applications - Pumps and PlantsDokument28 SeitenLPG Applications - Pumps and PlantsChristian Vargas100% (2)

- African Gas Pipeline Project ESIA SummaryDokument28 SeitenAfrican Gas Pipeline Project ESIA SummaryodeinatusNoch keine Bewertungen

- Blackmer LPG Equipment Training ManualDokument74 SeitenBlackmer LPG Equipment Training ManualEjaz Ahmed Rana100% (2)

- Project Report (Generalview) For Manufacturing High Pressure Rubber HosesDokument7 SeitenProject Report (Generalview) For Manufacturing High Pressure Rubber HosessarvgyataNoch keine Bewertungen

- RX 33 BrochureDokument6 SeitenRX 33 BrochureJuan Adres VelazquezNoch keine Bewertungen

- Dip Fire Safety ManagementDokument23 SeitenDip Fire Safety ManagementBabu PauloseNoch keine Bewertungen

- Launching of Bio Gas in GujranwalaDokument24 SeitenLaunching of Bio Gas in GujranwalaZaukNoch keine Bewertungen

- Introduction To The Industry: Indian Oil Corporation Limited, or Indianoil, Is An Indian StateDokument4 SeitenIntroduction To The Industry: Indian Oil Corporation Limited, or Indianoil, Is An Indian StateAbhishek GuptaNoch keine Bewertungen

- STD 150 PDFDokument27 SeitenSTD 150 PDFnavjot singhNoch keine Bewertungen

- Lectures Notes in Combustion FinalDokument66 SeitenLectures Notes in Combustion FinalMahmoud Abdelghafar ElhussienyNoch keine Bewertungen

- Case Study On HPCL Rasoi GharDokument1 SeiteCase Study On HPCL Rasoi Ghartarundua86Noch keine Bewertungen