Das könnte Ihnen auch gefallen

- DerivativesDokument65 SeitenDerivativesShreyas DongreNoch keine Bewertungen

- Forward Rate AgreementsDokument3 SeitenForward Rate AgreementssahilgeraNoch keine Bewertungen

- Lock in Interest Rates with FRAsDokument4 SeitenLock in Interest Rates with FRAsSangram PandaNoch keine Bewertungen

- What is a Forward Rate Agreement (FRADokument2 SeitenWhat is a Forward Rate Agreement (FRAmuzzamil123Noch keine Bewertungen

- Interest Rate SwapsDokument6 SeitenInterest Rate SwapsKanchan ChawlaNoch keine Bewertungen

- Forward Rate AgreementsDokument3 SeitenForward Rate AgreementsNaga Mani MeruguNoch keine Bewertungen

- Interest Rate FuturesDokument103 SeitenInterest Rate FuturesSumit SinghNoch keine Bewertungen

- Interest Rate DerivativesDokument9 SeitenInterest Rate DerivativesPrasad Nayak100% (1)

- 2 Forward Rate AgreementDokument8 Seiten2 Forward Rate AgreementRicha Gupta100% (1)

- Forward Rate Agreement HedgingDokument11 SeitenForward Rate Agreement HedgingmanaskaushikNoch keine Bewertungen

- ACI Forward Rate Agreements (FRAs) CourseDokument12 SeitenACI Forward Rate Agreements (FRAs) CourseJovan SsenkandwaNoch keine Bewertungen

- Forward Rate Agreement CalculationDokument4 SeitenForward Rate Agreement Calculationjustinmark99Noch keine Bewertungen

- Forward Rate AgreementsDokument2 SeitenForward Rate Agreementsajain22Noch keine Bewertungen

- Valuation of A Forward Rate Agreement (Pp. 95-96) : Example: You Agree To Borrow $100 From September 1Dokument5 SeitenValuation of A Forward Rate Agreement (Pp. 95-96) : Example: You Agree To Borrow $100 From September 1Reza Al SaadNoch keine Bewertungen

- Swapd and FRAsDokument53 SeitenSwapd and FRAsSCCEGNoch keine Bewertungen

- Forward Rate Agreements: Learning CurveDokument9 SeitenForward Rate Agreements: Learning CurveLu DanqingNoch keine Bewertungen

- FRADokument4 SeitenFRASeema SrivastavaNoch keine Bewertungen

- General Knowledge Today - 113Dokument2 SeitenGeneral Knowledge Today - 113niranjan_meharNoch keine Bewertungen

- Session 6.3-Forward Rate Agreements LectureDokument6 SeitenSession 6.3-Forward Rate Agreements LectureQamber AliNoch keine Bewertungen

- Introduction to Interest Rate SwapsDokument14 SeitenIntroduction to Interest Rate SwapsFelix RemeteaNoch keine Bewertungen

- CH 18Dokument131 SeitenCH 18Desai SarvidaNoch keine Bewertungen

- Chap 18Dokument110 SeitenChap 18Desai SarvidaNoch keine Bewertungen

- Forward-Forward Contract and Forward Rate Agreement.Dokument6 SeitenForward-Forward Contract and Forward Rate Agreement.tinotendacarltonNoch keine Bewertungen

- Chapter 5: Interest Rate Risks: Lecturer: Amadeus GABRIEL La Rochelle Business SchoolDokument25 SeitenChapter 5: Interest Rate Risks: Lecturer: Amadeus GABRIEL La Rochelle Business SchoolJuana BoresNoch keine Bewertungen

- Forward Rate AgreementsDokument6 SeitenForward Rate AgreementsAmul ShresthaNoch keine Bewertungen

- Valuation of A Forward Rate Agreement PDFDokument5 SeitenValuation of A Forward Rate Agreement PDFdjtaz13Noch keine Bewertungen

- International Financial Management PgapteDokument30 SeitenInternational Financial Management Pgapterameshmba100% (1)

- Managing Fixed-Income Positions With OTC DerivativesDokument86 SeitenManaging Fixed-Income Positions With OTC DerivativestniravNoch keine Bewertungen

- Financial Engineering and PlanningDokument17 SeitenFinancial Engineering and PlanningSavius AllyNoch keine Bewertungen

- Forward Rate Agreements: Session 3 - Derivatives & Risk MGTDokument15 SeitenForward Rate Agreements: Session 3 - Derivatives & Risk MGTMayankSharmaNoch keine Bewertungen

- Interest Rate DerivativesDokument58 SeitenInterest Rate DerivativesIndia Forex100% (2)

- M Waqas BBFE-17-48 Assignment #3Dokument4 SeitenM Waqas BBFE-17-48 Assignment #3Muhammad WaQaSNoch keine Bewertungen

- Derivatives in ALMDokument53 SeitenDerivatives in ALMSam SinhaNoch keine Bewertungen

- Fixed Income & Interest Rate DerivativesDokument64 SeitenFixed Income & Interest Rate DerivativeskarthikNoch keine Bewertungen

- Chapter 10 - Forward and Futures Contracts ExamplesDokument65 SeitenChapter 10 - Forward and Futures Contracts ExamplesLeon MushiNoch keine Bewertungen

- Forward Rate Agreement (FRA)Dokument3 SeitenForward Rate Agreement (FRA)Shriyanshi JaitlyNoch keine Bewertungen

- Uni Flex 120922Dokument12 SeitenUni Flex 120922wilsonNoch keine Bewertungen

- Swaps and Interest Rate DerivativesDokument20 SeitenSwaps and Interest Rate DerivativesShankar VenkatramanNoch keine Bewertungen

- Swap Derivatives: Forward Swaps and SwaptionsDokument74 SeitenSwap Derivatives: Forward Swaps and Swaptionsvineet_bmNoch keine Bewertungen

- Chapter 8: Swaps ExplainedDokument23 SeitenChapter 8: Swaps ExplainedChau NguyenNoch keine Bewertungen

- F3 Chapter 10Dokument22 SeitenF3 Chapter 10Ali ShahnawazNoch keine Bewertungen

- TM Interest Rate SwapDokument16 SeitenTM Interest Rate SwapTran ManhNoch keine Bewertungen

- II. Interest RatesDokument15 SeitenII. Interest RatesDaniel Salas LeonNoch keine Bewertungen

- EFB344 Lecture07, FRAs and SwapsDokument35 SeitenEFB344 Lecture07, FRAs and SwapsTibet LoveNoch keine Bewertungen

- (Lehman Brothers, Tuckman) Interest Rate Parity, Money Market Baisis Swaps, and Cross-Currency Basis SwapsDokument14 Seiten(Lehman Brothers, Tuckman) Interest Rate Parity, Money Market Baisis Swaps, and Cross-Currency Basis SwapsJonathan Ching100% (1)

- Derivatives - Betting: Chapter Break UpDokument34 SeitenDerivatives - Betting: Chapter Break UpJatinkatrodiyaNoch keine Bewertungen

- HW NongradedDokument4 SeitenHW NongradedAnDy YiMNoch keine Bewertungen

- CH 14Dokument31 SeitenCH 14mohamedhusseindableNoch keine Bewertungen

- Risk Management of SwapsDokument32 SeitenRisk Management of SwapsNilesh PanchalNoch keine Bewertungen

- Examining a two-year bill facility case studyDokument29 SeitenExamining a two-year bill facility case studyThorNoch keine Bewertungen

- Bonds ValuationsDokument57 SeitenBonds ValuationsarmailgmNoch keine Bewertungen

- Name of The Teacher: Gayathri Ravikumar Department: Commerce PG. Subject/Paper Class Year Date Class Time Unit Topic Interest Rate SwapsDokument5 SeitenName of The Teacher: Gayathri Ravikumar Department: Commerce PG. Subject/Paper Class Year Date Class Time Unit Topic Interest Rate SwapsGayu RkNoch keine Bewertungen

- Currency Derivative1Dokument47 SeitenCurrency Derivative1IubianNoch keine Bewertungen

- Interest Rate RiskDokument33 SeitenInterest Rate RiskirfanhaidersewagNoch keine Bewertungen

- TVM Seminar 3 NotesDokument34 SeitenTVM Seminar 3 Notes朱艺璇Noch keine Bewertungen

- Test Your Knowledge: 2.2.4.2 Pricing of SwaptionsDokument11 SeitenTest Your Knowledge: 2.2.4.2 Pricing of SwaptionsRITZ BROWNNoch keine Bewertungen

- AFM 2: Interest Rate Swaps: S Krishnamoorthy:, Cell:9821461488Dokument24 SeitenAFM 2: Interest Rate Swaps: S Krishnamoorthy:, Cell:9821461488Johar MenezesNoch keine Bewertungen

- Switching to MCLR LoansDokument7 SeitenSwitching to MCLR LoansPRAJA rajyamNoch keine Bewertungen

- 5 Simple Interest and DiscountDokument69 Seiten5 Simple Interest and DiscountJUSTIN HECTOR BRENT SAJULGANoch keine Bewertungen

- Discriminant Analysis For Risk Classification and PredictionDokument23 SeitenDiscriminant Analysis For Risk Classification and PredictionSumit SharmaNoch keine Bewertungen

- Engineering course timetable for week 3Dokument1 SeiteEngineering course timetable for week 3Nisa BoodooNoch keine Bewertungen

- Ch4: Havaldar and CavaleDokument27 SeitenCh4: Havaldar and CavaleShubha Brota Raha75% (4)

- Sales ForcastingDokument28 SeitenSales Forcastingkr_dandekarNoch keine Bewertungen

- The Persuasive Role of Incidental Similarity - 30 AugDokument53 SeitenThe Persuasive Role of Incidental Similarity - 30 AugSumit SharmaNoch keine Bewertungen

- PRJT 1Dokument18 SeitenPRJT 1Sumit SharmaNoch keine Bewertungen

- WTO Provisions and Implications For IndiaDokument19 SeitenWTO Provisions and Implications For IndiaSumit SharmaNoch keine Bewertungen

- Financial Analysis and Risk Profile of DLF LtdDokument31 SeitenFinancial Analysis and Risk Profile of DLF LtdSumit SharmaNoch keine Bewertungen

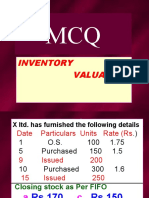

- MCQ Inventory Valuation LBSIMDokument49 SeitenMCQ Inventory Valuation LBSIMSumit SharmaNoch keine Bewertungen

- Registration of Mortgages and Charges FinalDokument34 SeitenRegistration of Mortgages and Charges FinalEisha MahamNoch keine Bewertungen

- Contrato de Arrendamiento en InglesDokument4 SeitenContrato de Arrendamiento en InglesJaneth Camacho100% (5)

- Aggregation Policy SummaryDokument5 SeitenAggregation Policy SummaryjosephmeawadNoch keine Bewertungen

- Study+school+slides Market Risk ManagementDokument64 SeitenStudy+school+slides Market Risk ManagementEbenezerNoch keine Bewertungen

- Non-Complete Affidavit of UndertakingDokument2 SeitenNon-Complete Affidavit of UndertakingMENIEZA AVILESNoch keine Bewertungen

- 0201 0521Dokument3 Seiten0201 0521Whimsical WillowNoch keine Bewertungen

- Stone Panels Inc Bankruptcy FilingDokument4 SeitenStone Panels Inc Bankruptcy FilingespanolalNoch keine Bewertungen

- Letter of CreditDokument10 SeitenLetter of Creditmukesh12345678Noch keine Bewertungen

- SRS Liquidation Meeting AgendaDokument4 SeitenSRS Liquidation Meeting AgendaManoj100% (1)

- Test Your Knowledge: 2.2.4.2 Pricing of SwaptionsDokument11 SeitenTest Your Knowledge: 2.2.4.2 Pricing of SwaptionsRITZ BROWNNoch keine Bewertungen

- Contracts Practice Exercise A - Issa HawatmehDokument4 SeitenContracts Practice Exercise A - Issa HawatmehIssa HawatmehNoch keine Bewertungen

- PCU BUS LAW AND REGULATIONS ONLINE QUIZDokument2 SeitenPCU BUS LAW AND REGULATIONS ONLINE QUIZPerdito John VinNoch keine Bewertungen

- 2 Ibc 2016Dokument8 Seiten2 Ibc 2016Jinal SanghviNoch keine Bewertungen

- Law of Agency (Continue..)Dokument15 SeitenLaw of Agency (Continue..)hazeeNoch keine Bewertungen

- FRIA HandoutDokument30 SeitenFRIA HandoutSofia Brondial100% (1)

- Confirmation of Enrolment: Customer Number For Work Provider UseDokument1 SeiteConfirmation of Enrolment: Customer Number For Work Provider Useallan endoNoch keine Bewertungen

- Filipinas Port Services, Inc., V. Victoriano S. GoDokument3 SeitenFilipinas Port Services, Inc., V. Victoriano S. GoVicco G . PiodosNoch keine Bewertungen

- "Pasublat Pwesto" Agreement: ST NDDokument3 Seiten"Pasublat Pwesto" Agreement: ST NDCordilleraBasicSectors TransportCooperativeNoch keine Bewertungen

- NIL ReviewerDokument37 SeitenNIL ReviewerAngela Marie Acielo AlmalbisNoch keine Bewertungen

- HDFC Life Sanchay benefits for 27 year oldDokument2 SeitenHDFC Life Sanchay benefits for 27 year oldKiran NNoch keine Bewertungen

- Quiz - Partnership Law Nov 7 2020Dokument4 SeitenQuiz - Partnership Law Nov 7 2020eunicemaraNoch keine Bewertungen

- Rehabilitation and Insolvency Act summaryDokument31 SeitenRehabilitation and Insolvency Act summarySheryl OgocNoch keine Bewertungen

- The Agreement On Debt AssignmentDokument9 SeitenThe Agreement On Debt Assignment賴慶瑋Noch keine Bewertungen

- Sale of Goods Act, 1930 Key ProvisionsDokument47 SeitenSale of Goods Act, 1930 Key ProvisionssuhasiniNoch keine Bewertungen

- L-NU AA-23-02-01-18 Midterm Exam ReviewDokument4 SeitenL-NU AA-23-02-01-18 Midterm Exam ReviewAmie Jane MirandaNoch keine Bewertungen

- Tradovate Arbitration AgreementDokument2 SeitenTradovate Arbitration AgreementAbdelazeem GawadNoch keine Bewertungen

- Article 1825 1827Dokument13 SeitenArticle 1825 1827Clesea LopezNoch keine Bewertungen

- Negotiable Instruments Law Course OutlineDokument9 SeitenNegotiable Instruments Law Course OutlineChris Dianne Miniano SanchezNoch keine Bewertungen

- NOTES - Securities and Regulation Code (SRC)Dokument6 SeitenNOTES - Securities and Regulation Code (SRC)JUAN MIGUEL GUZMANNoch keine Bewertungen

- International Trading Corporation vs. Threshold Pacific CorporationDokument15 SeitenInternational Trading Corporation vs. Threshold Pacific CorporationQueenVictoriaAshleyPrietoNoch keine Bewertungen