Das könnte Ihnen auch gefallen

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (119)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (399)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (587)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2219)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (890)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Blstone 2Dokument508 SeitenBlstone 2Kasper AchtonNoch keine Bewertungen

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (73)

- Types of EntrepreneursDokument32 SeitenTypes of EntrepreneursabbsheyNoch keine Bewertungen

- April PayslipDokument1 SeiteApril PayslipDev CharanNoch keine Bewertungen

- Waterfall Model Case StudyDokument6 SeitenWaterfall Model Case StudyAkor Murthy50% (2)

- Data Warehousing Fundamentals Paulraj PonniahDokument518 SeitenData Warehousing Fundamentals Paulraj Ponniahgetraja2175% (4)

- Managerial EconomicsDokument16 SeitenManagerial EconomicsHarshitPalNoch keine Bewertungen

- PNB VS ChuaDokument1 SeitePNB VS Chuacareyssa Mae IpilNoch keine Bewertungen

- TCC Midc Company ListDokument4 SeitenTCC Midc Company ListAbhishek SinghNoch keine Bewertungen

- Accounting and Finance For ManagersDokument322 SeitenAccounting and Finance For ManagersNagesh Jorrigala83% (6)

- Financial Analysis of A Small BusinessDokument9 SeitenFinancial Analysis of A Small BusinessAkor MurthyNoch keine Bewertungen

- Investor Perception Survey on Mutual Fund SelectionDokument26 SeitenInvestor Perception Survey on Mutual Fund SelectionAkor MurthyNoch keine Bewertungen

- About IndiaDokument38 SeitenAbout IndiaAkor MurthyNoch keine Bewertungen

- Message of Dr. Abdul Kalam For Each IndianDokument11 SeitenMessage of Dr. Abdul Kalam For Each IndianRaja RavivarmanNoch keine Bewertungen

- About IndiaDokument38 SeitenAbout IndiaAkor MurthyNoch keine Bewertungen

- Sales and Purchases 2021-22Dokument15 SeitenSales and Purchases 2021-22Vamsi ShettyNoch keine Bewertungen

- Exercises: Set B: Standard CustomDokument4 SeitenExercises: Set B: Standard CustomMalik HamidNoch keine Bewertungen

- Survey highlights deficits facing India's minority districtsDokument75 SeitenSurvey highlights deficits facing India's minority districtsAnonymous yCpjZF1rFNoch keine Bewertungen

- Pre Test of Bahasa Inggris 21 - 9 - 2020Dokument5 SeitenPre Test of Bahasa Inggris 21 - 9 - 2020magdalena sriNoch keine Bewertungen

- Marx Alienated LaborDokument5 SeitenMarx Alienated LaborDanielle BenderNoch keine Bewertungen

- 20 Recent IELTS Graph Samples With AnswersDokument14 Seiten20 Recent IELTS Graph Samples With AnswersRizwan BashirNoch keine Bewertungen

- Account Statement For Account Number 4063008700000556: Branch DetailsDokument9 SeitenAccount Statement For Account Number 4063008700000556: Branch Detailsmanju maheshNoch keine Bewertungen

- K&N Case Group - 3Dokument41 SeitenK&N Case Group - 3priya_pritika6561100% (1)

- Az Trading UsdjpyDokument35 SeitenAz Trading UsdjpyMario Gonzalez CarreñoNoch keine Bewertungen

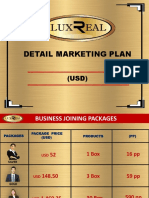

- Luxreal Detail Marketing Plan (2019) UsdDokument32 SeitenLuxreal Detail Marketing Plan (2019) UsdTawanda Tirivangani100% (2)

- More Unanswered QuestionsDokument8 SeitenMore Unanswered QuestionspermaculturistNoch keine Bewertungen

- Economics of The Printing PressDokument39 SeitenEconomics of The Printing PressNancy Xie100% (1)

- Ethio-Views Online News PaperDokument1 SeiteEthio-Views Online News PaperBelayneh zelelewNoch keine Bewertungen

- Sustainability Template August2012Dokument25 SeitenSustainability Template August2012amitjain310Noch keine Bewertungen

- Iskandar Malaysia's Vision, Growth and Promotional PoliciesDokument29 SeitenIskandar Malaysia's Vision, Growth and Promotional PoliciesJiaChyi PungNoch keine Bewertungen

- Macroeconomic Analysis of USA: GDP, Inflation & UnemploymentDokument2 SeitenMacroeconomic Analysis of USA: GDP, Inflation & UnemploymentVISHAL GOYALNoch keine Bewertungen

- Exchange Arithmetic - Problems PDFDokument13 SeitenExchange Arithmetic - Problems PDFNipul BafnaNoch keine Bewertungen

- Phoenix Pallasio Lucknow Presentation 04-09-2019Dokument41 SeitenPhoenix Pallasio Lucknow Presentation 04-09-2019T PatelNoch keine Bewertungen

- Immelt's Reinvention of GEDokument5 SeitenImmelt's Reinvention of GEbodhi_bg100% (1)

- Finance 1Dokument12 SeitenFinance 1Mary Ann AntenorNoch keine Bewertungen

- 19th Century Changes: Economic Changes Cultural Changes Political Changes Social ChangesDokument1 Seite19th Century Changes: Economic Changes Cultural Changes Political Changes Social ChangesShina P ReyesNoch keine Bewertungen

- Bep NowDokument25 SeitenBep NowDenny KurniawanNoch keine Bewertungen

- IBT-REVIEWERDokument10 SeitenIBT-REVIEWERBrenda CastilloNoch keine Bewertungen

- Infosys Aptitude Questions and Answers With ExplanationDokument5 SeitenInfosys Aptitude Questions and Answers With ExplanationVirrru NarendraNoch keine Bewertungen