Das könnte Ihnen auch gefallen

- Chap 004Dokument45 SeitenChap 004Yuti XianNoch keine Bewertungen

- Chapter 5 - Accounting For Merchandising OperationsDokument42 SeitenChapter 5 - Accounting For Merchandising OperationsmaziahesaNoch keine Bewertungen

- Reporting and Analyzing Inventories: © The Mcgraw-Hill Companies, Inc., 2010 Mcgraw-Hill/IrwinDokument61 SeitenReporting and Analyzing Inventories: © The Mcgraw-Hill Companies, Inc., 2010 Mcgraw-Hill/IrwinYvonne Teo Yee VoonNoch keine Bewertungen

- Importance of AccountingDokument52 SeitenImportance of AccountingLalithaNoch keine Bewertungen

- Chap 006 NotesDokument69 SeitenChap 006 Notesflower104Noch keine Bewertungen

- Ch05-Accounting PrincipleDokument9 SeitenCh05-Accounting PrincipleEthanAhamed100% (2)

- Taller Cinco Acco 111Dokument41 SeitenTaller Cinco Acco 111api-274120622Noch keine Bewertungen

- Computerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionVon EverandComputerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionNoch keine Bewertungen

- Ch06 12edDokument52 SeitenCh06 12edAhmed Mahmoud AbouzaidNoch keine Bewertungen

- Incomplete RecordsDokument13 SeitenIncomplete RecordsSylvan Muzumbwe MakondoNoch keine Bewertungen

- Periodic Methods of AccountingDokument40 SeitenPeriodic Methods of AccountingKiasatina Amalia MustafaNoch keine Bewertungen

- Chapter 4,5,6 QuizzesDokument22 SeitenChapter 4,5,6 QuizzesAnonymous aPQWrwo3iiNoch keine Bewertungen

- A Presentation On: Accounting For Merchandising OperationDokument26 SeitenA Presentation On: Accounting For Merchandising OperationKayesCjNoch keine Bewertungen

- Lecture 6 Accounting For Inventory (I)Dokument33 SeitenLecture 6 Accounting For Inventory (I)chestervale1Noch keine Bewertungen

- WRD 27e SG Solutions CH 06Dokument22 SeitenWRD 27e SG Solutions CH 06Ellii YouTube channelNoch keine Bewertungen

- Reporting and Interpreting Sales Revenue, Receivables, and CashDokument53 SeitenReporting and Interpreting Sales Revenue, Receivables, and CashEbenezer Amoah-KyeiNoch keine Bewertungen

- Chapter 5 Inventory AccountingDokument57 SeitenChapter 5 Inventory Accountinghosie.oqbe100% (1)

- Chapter 3Dokument31 SeitenChapter 3EricKHLeawNoch keine Bewertungen

- ACCT Midterm 2Dokument26 SeitenACCT Midterm 2Gene'sNoch keine Bewertungen

- 11 Edition: Mcgraw-Hill/IrwinDokument52 Seiten11 Edition: Mcgraw-Hill/IrwinfaisalNoch keine Bewertungen

- Accounting For Merchandising OperationsDokument31 SeitenAccounting For Merchandising OperationsBülent Kılıç100% (1)

- Bis Second Term Sheet 1Dokument11 SeitenBis Second Term Sheet 1magdy kamelNoch keine Bewertungen

- Acc. QuestionsDokument5 SeitenAcc. QuestionsFaryal MughalNoch keine Bewertungen

- FUNDAMENTALS OF ACCOUNTANCY BUSINESS AND MANAGEMENT PPP 1Dokument185 SeitenFUNDAMENTALS OF ACCOUNTANCY BUSINESS AND MANAGEMENT PPP 1Janelle Dela Cruz100% (1)

- 02 Accounting For A Merchandising BusinessDokument54 Seiten02 Accounting For A Merchandising BusinessApril SasamNoch keine Bewertungen

- Nature of Merchandising BusinessDokument12 SeitenNature of Merchandising BusinessJessica ManahanNoch keine Bewertungen

- Cost of Goods SoldDokument23 SeitenCost of Goods SoldCrizylen Mae Pepito LahoylahoyNoch keine Bewertungen

- Merchadising MOCK QUIZDokument5 SeitenMerchadising MOCK QUIZCarl Dhaniel Garcia SalenNoch keine Bewertungen

- Accounting For Merchandising ActivitiesDokument45 SeitenAccounting For Merchandising ActivitiessaadashfaqNoch keine Bewertungen

- Module 9 Accounting For A Merchandiser Dec 2021 (20231122130953)Dokument34 SeitenModule 9 Accounting For A Merchandiser Dec 2021 (20231122130953)Antonette LaurioNoch keine Bewertungen

- Chapter 9 Profit Planning PDFDokument86 SeitenChapter 9 Profit Planning PDFAisyahlathifawahyudiNoch keine Bewertungen

- Accounting For Merchandising BusinessesDokument73 SeitenAccounting For Merchandising BusinessesYustamar Ramatsuy100% (1)

- Chapter 13Dokument59 SeitenChapter 13Asad AbbasNoch keine Bewertungen

- Accounting Cycle of A Merchandising BusinessDokument25 SeitenAccounting Cycle of A Merchandising BusinessMichelle Vinoray Pascual100% (2)

- Accounting For MerchandisingDokument45 SeitenAccounting For MerchandisingJane OfendaNoch keine Bewertungen

- Entrep Week4 Q2Dokument28 SeitenEntrep Week4 Q2Aisa CrisologoNoch keine Bewertungen

- Reporting and Analyzing Receivables: © The Mcgraw-Hill Companies, Inc., 2010 Mcgraw-Hill/IrwinDokument52 SeitenReporting and Analyzing Receivables: © The Mcgraw-Hill Companies, Inc., 2010 Mcgraw-Hill/IrwinYvonne Teo Yee VoonNoch keine Bewertungen

- Chapter 5Dokument14 SeitenChapter 5RB100% (3)

- InventoriesDokument47 SeitenInventoriesMarjorie NepomucenoNoch keine Bewertungen

- CombinepdfDokument226 SeitenCombinepdfjed rolluque decena100% (1)

- Chapter-5: Accounting For Merchandising OperationsDokument39 SeitenChapter-5: Accounting For Merchandising OperationsNoel Buenafe JrNoch keine Bewertungen

- Chapter 4 5 6Dokument4 SeitenChapter 4 5 6nguyen2190Noch keine Bewertungen

- Accounting For Merchandising Business ACG 2021 Module 5Dokument45 SeitenAccounting For Merchandising Business ACG 2021 Module 5Janine Joy Orpilla50% (2)

- Accounting 211 Chapter 5Dokument46 SeitenAccounting 211 Chapter 5Darwin QuintosNoch keine Bewertungen

- Lecture Notes Chapters 1-4Dokument28 SeitenLecture Notes Chapters 1-4BlueFireOblivionNoch keine Bewertungen

- Accounting ChapterDokument13 SeitenAccounting ChapterMamaru SewalemNoch keine Bewertungen

- Cash Discounts & Trade Discounts I. DrillDokument3 SeitenCash Discounts & Trade Discounts I. DrillArny MaynigoNoch keine Bewertungen

- Accounting Online Test With AnswersDokument10 SeitenAccounting Online Test With AnswersAuroraNoch keine Bewertungen

- ACTG 101-101a Topic 4 Processing Transactions of A Merchandising BusinessDokument67 SeitenACTG 101-101a Topic 4 Processing Transactions of A Merchandising BusinessEdmar Lerin100% (1)

- Intro To Financial Analysis AssignmentDokument4 SeitenIntro To Financial Analysis AssignmentAshar AlamNoch keine Bewertungen

- Accounting Textbook Solutions - 19Dokument19 SeitenAccounting Textbook Solutions - 19acc-expertNoch keine Bewertungen

- Chapter 7Dokument26 SeitenChapter 7EricKHLeawNoch keine Bewertungen

- 10 Bbfa1103 T6Dokument31 Seiten10 Bbfa1103 T6djaljdNoch keine Bewertungen

- 2010-06-23 203304 Financialaccounting 2Dokument6 Seiten2010-06-23 203304 Financialaccounting 2pi!Noch keine Bewertungen

- Acctg 11-1 Gbs For Week 11Dokument5 SeitenAcctg 11-1 Gbs For Week 11Ynna Gesite0% (1)

- Module 05-06-07 ProblemsDokument14 SeitenModule 05-06-07 ProblemsmaxzNoch keine Bewertungen

- Acct Lesson 9Dokument9 SeitenAcct Lesson 9Gracielle EspirituNoch keine Bewertungen

- Amazon Business: A Comprehensive Guide for B2B ProcurementVon EverandAmazon Business: A Comprehensive Guide for B2B ProcurementNoch keine Bewertungen

- Soalan Test Mid Term BiologyDokument4 SeitenSoalan Test Mid Term Biologybatraz79Noch keine Bewertungen

- What Current Is Flowing If 0.67 C of Charge Pass A Point in 0.30s?Dokument4 SeitenWhat Current Is Flowing If 0.67 C of Charge Pass A Point in 0.30s?batraz79Noch keine Bewertungen

- Business Comm Ppb3043 Ri Sem2 Year 2013 - 2014Dokument15 SeitenBusiness Comm Ppb3043 Ri Sem2 Year 2013 - 2014batraz79Noch keine Bewertungen

- Work Schedule Preliminaries: Sub StructureDokument4 SeitenWork Schedule Preliminaries: Sub Structurebatraz79Noch keine Bewertungen

- Upgrade Electrolytic Capacitors To Rubycon BrandDokument6 SeitenUpgrade Electrolytic Capacitors To Rubycon Brandbatraz79Noch keine Bewertungen

- 20150227080233Chp 1 Electric Charge and Electric FieldDokument37 Seiten20150227080233Chp 1 Electric Charge and Electric Fieldbatraz79Noch keine Bewertungen

- Common Ions ListingDokument2 SeitenCommon Ions Listingbatraz79Noch keine Bewertungen

- 20150316140353TUTORIAL 4 (Topik 5&6)Dokument4 Seiten20150316140353TUTORIAL 4 (Topik 5&6)batraz79Noch keine Bewertungen

- 20150316140314tutorial 2 (Topik 3)Dokument1 Seite20150316140314tutorial 2 (Topik 3)batraz79Noch keine Bewertungen

- Chapter 5Dokument25 SeitenChapter 5batraz79Noch keine Bewertungen

- The Production Cycle: Accounting Information Systems, 9/e, Romney/SteinbartDokument48 SeitenThe Production Cycle: Accounting Information Systems, 9/e, Romney/Steinbartbatraz79Noch keine Bewertungen

- 20150227080251Chp 4 MagnetismDokument30 Seiten20150227080251Chp 4 Magnetismbatraz79Noch keine Bewertungen

- Review of LiteratureDokument12 SeitenReview of Literaturebatraz79Noch keine Bewertungen

- The Basics of Educational ResearchDokument13 SeitenThe Basics of Educational Researchbatraz79Noch keine Bewertungen

- Tutorial 6 (Chapter 9 and 10)Dokument3 SeitenTutorial 6 (Chapter 9 and 10)batraz79Noch keine Bewertungen

- Module 4: The Human Resource Management Cycle: Accounting Information Systems: Essential Concepts and ApplicationsDokument20 SeitenModule 4: The Human Resource Management Cycle: Accounting Information Systems: Essential Concepts and Applicationsbatraz79Noch keine Bewertungen

- 20150218130206kuliah6 IntrumentDokument44 Seiten20150218130206kuliah6 Intrumentbatraz79Noch keine Bewertungen

- 20141008131049chapter 7cDokument52 Seiten20141008131049chapter 7cbatraz79Noch keine Bewertungen

- 20150218130208kuliah7 ValidrelibleDokument43 Seiten20150218130208kuliah7 Validreliblebatraz79Noch keine Bewertungen

- Business Communication Foundations: Student Slides CH 1 - 1Dokument14 SeitenBusiness Communication Foundations: Student Slides CH 1 - 1batraz79Noch keine Bewertungen

- Hapter 15: Pearson Education, IncDokument36 SeitenHapter 15: Pearson Education, Incbatraz79Noch keine Bewertungen

- Topic 7 Prokaryotes and VirusesDokument50 SeitenTopic 7 Prokaryotes and Virusesbatraz79Noch keine Bewertungen

- 20150227080211Chp 5 InductionDokument17 Seiten20150227080211Chp 5 Inductionbatraz79Noch keine Bewertungen

- Sickle Cell enDokument9 SeitenSickle Cell enbatraz79Noch keine Bewertungen

- Premiums and WarrantiesDokument17 SeitenPremiums and WarrantiesKaye Choraine NadumaNoch keine Bewertungen

- Assignment 1558529720 SmsDokument43 SeitenAssignment 1558529720 SmsSmit JariwalaNoch keine Bewertungen

- BUS13401n14099 10 09Dokument2 SeitenBUS13401n14099 10 09jc199707Noch keine Bewertungen

- The Capital Expenditure Decisions Have The Following FeaturesDokument3 SeitenThe Capital Expenditure Decisions Have The Following FeaturesYosephine KurniatyNoch keine Bewertungen

- FIN 254 (SEC: 19) Assignment: Project: Ratio AnalysisDokument42 SeitenFIN 254 (SEC: 19) Assignment: Project: Ratio AnalysisMuntasir Sizan100% (1)

- Computerised Accounting With MYOB 2Dokument126 SeitenComputerised Accounting With MYOB 2AzwirNoch keine Bewertungen

- Madaraka Ltd. Statement of Comprehensive Income For The Year Ended 31 March 2020 KES'000' KES'000'Dokument17 SeitenMadaraka Ltd. Statement of Comprehensive Income For The Year Ended 31 March 2020 KES'000' KES'000'Maryjoy KilonzoNoch keine Bewertungen

- REXEL SA - Research Report - FinalDokument6 SeitenREXEL SA - Research Report - FinalGlen BorgNoch keine Bewertungen

- Central Plaza: Project Report For Development ofDokument18 SeitenCentral Plaza: Project Report For Development ofHemant BalodiNoch keine Bewertungen

- Sample Tax ComputationEXDokument2 SeitenSample Tax ComputationEXAngelica RubiosNoch keine Bewertungen

- Can You Capitalize It As PPE or Not - IfRSboxDokument63 SeitenCan You Capitalize It As PPE or Not - IfRSboxMarkie GrabilloNoch keine Bewertungen

- Accounting MS1 2022Dokument18 SeitenAccounting MS1 2022Faaz SheriffdeenNoch keine Bewertungen

- Accounting Process. Part 3Dokument18 SeitenAccounting Process. Part 3Karl Alvin Reyes HipolitoNoch keine Bewertungen

- Preparing Financial StatementsDokument6 SeitenPreparing Financial StatementsAUDITOR97Noch keine Bewertungen

- HARD ROCK COMPANY Statement of Financial PositionDokument3 SeitenHARD ROCK COMPANY Statement of Financial PositionJade Lykarose Ochavillo GalendoNoch keine Bewertungen

- Chapter 13 - Relevant Costs For Decision Making PDFDokument34 SeitenChapter 13 - Relevant Costs For Decision Making PDFnafin ayub ArilNoch keine Bewertungen

- Software Associates-Variance Analysis and Flexible BudgetingDokument4 SeitenSoftware Associates-Variance Analysis and Flexible Budgetingk_Dashy846550% (2)

- Finacial Decision CaseDokument7 SeitenFinacial Decision Caseayeshaali20Noch keine Bewertungen

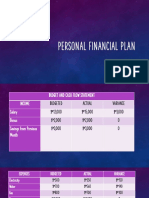

- Personal Financial PlanDokument6 SeitenPersonal Financial PlanThomgie TilaNoch keine Bewertungen

- GT BankDokument1 SeiteGT BankFuaad DodooNoch keine Bewertungen

- Cfas - Reviewer PDFDokument21 SeitenCfas - Reviewer PDFMira Monica D. VillacastinNoch keine Bewertungen

- Value Added Tax (IPCC) 2013-14: Complete Information Relating VATDokument24 SeitenValue Added Tax (IPCC) 2013-14: Complete Information Relating VATTekumani Naveen KumarNoch keine Bewertungen

- Butler Excel Sheets (Group 2)Dokument11 SeitenButler Excel Sheets (Group 2)Nathan ClarkinNoch keine Bewertungen

- Trend AnalysisDokument1 SeiteTrend Analysisangel caoNoch keine Bewertungen

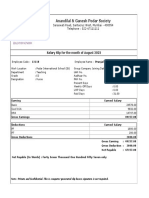

- Anandilal & Ganesh Podar Society: Salary Slip For The Month of August 2022Dokument1 SeiteAnandilal & Ganesh Podar Society: Salary Slip For The Month of August 2022Pradnyesh GuramNoch keine Bewertungen

- Prelim - PART 2Dokument6 SeitenPrelim - PART 2Dan RyanNoch keine Bewertungen

- BusinessFinance12 Q2 Mod6 Managing-Personal-Finance V5Dokument20 SeitenBusinessFinance12 Q2 Mod6 Managing-Personal-Finance V5Emsccy AbeciaNoch keine Bewertungen

- Marketing Plan Banana ChipsDokument34 SeitenMarketing Plan Banana Chipseahpot82% (61)

- Quiz DepletionDokument5 SeitenQuiz Depletionhoneyjoy salapantanNoch keine Bewertungen

- Bata Shoe Company Swot Analysis PDF FreeDokument33 SeitenBata Shoe Company Swot Analysis PDF FreeMB ManyauNoch keine Bewertungen