Das könnte Ihnen auch gefallen

- Utility BillDokument2 SeitenUtility BillMST FIROZA BEGUMNoch keine Bewertungen

- Askari Aviation Services Marketing ReportDokument66 SeitenAskari Aviation Services Marketing Reportsyed usman wazir100% (1)

- IRS Document 6209 Manual (2003 Ed.)Dokument0 SeitenIRS Document 6209 Manual (2003 Ed.)iamnumber8Noch keine Bewertungen

- Red Bull FinalDokument28 SeitenRed Bull FinalYousaf Haroon Yousafzai0% (1)

- Submittal MECH BMI Compressed-CompressedDokument125 SeitenSubmittal MECH BMI Compressed-CompressedAhmad ShiplyNoch keine Bewertungen

- "Billionares": and They Were Not Happy About ItDokument36 Seiten"Billionares": and They Were Not Happy About Itkhanriyaz23941560Noch keine Bewertungen

- NiplesDokument59 SeitenNiplesJose LiraNoch keine Bewertungen

- Mech ValvulasDokument92 SeitenMech ValvulasmoloNoch keine Bewertungen

- Irrational ExuberanceDokument52 SeitenIrrational ExuberancetrendscatcherNoch keine Bewertungen

- 2 Challenges of The Sri Lanka's Petroleum SectorDokument28 Seiten2 Challenges of The Sri Lanka's Petroleum Sectorrameshkarthik810Noch keine Bewertungen

- 2 Challenges of The Sri Lanka's Petroleum SectorDokument28 Seiten2 Challenges of The Sri Lanka's Petroleum SectorArunshanth TharmakumarNoch keine Bewertungen

- KawaiDokument29 SeitenKawaiMehdi SamNoch keine Bewertungen

- Steel Industry Energy & Value Chains: The Threat To CompetitivenessDokument23 SeitenSteel Industry Energy & Value Chains: The Threat To CompetitivenessAhmed AlmaghrbyNoch keine Bewertungen

- Market AnalysisDokument12 SeitenMarket Analysisilasakaa internationalNoch keine Bewertungen

- Manuscript FVDokument31 SeitenManuscript FVkenzaNoch keine Bewertungen

- Ganglands in 1990s Korean Gangster FilmDokument27 SeitenGanglands in 1990s Korean Gangster FilmAbhinandan GhoseNoch keine Bewertungen

- CMO April 2021 Special FocusDokument15 SeitenCMO April 2021 Special FocusabdulazizNoch keine Bewertungen

- MacroDokument10 SeitenMacrothareendaNoch keine Bewertungen

- ITA - Tin Market Outlook James Willoughby June - 22 PDFDokument12 SeitenITA - Tin Market Outlook James Willoughby June - 22 PDFRodrigo RodrigoNoch keine Bewertungen

- Initial Public Offering: Project By:-Dangar Amit WRO number:-WRO0586791 ICAI NavasariDokument24 SeitenInitial Public Offering: Project By:-Dangar Amit WRO number:-WRO0586791 ICAI NavasariFenil RamaniNoch keine Bewertungen

- Understanding Market Channels and Alternatives For Commercial Catfish Farmers (PDFDrive)Dokument95 SeitenUnderstanding Market Channels and Alternatives For Commercial Catfish Farmers (PDFDrive)AmiibahNoch keine Bewertungen

- Nickel Pig Iron in China: CommoditiesDokument8 SeitenNickel Pig Iron in China: CommoditiesDavid Budi SaputraNoch keine Bewertungen

- ContentDokument22 SeitenContentSteve JenkinsNoch keine Bewertungen

- Ferroalloys 99Dokument127 SeitenFerroalloys 99morymohyNoch keine Bewertungen

- 5 LarsWlecke CoalMarketandTradingDokument26 Seiten5 LarsWlecke CoalMarketandTradingtoniphillNoch keine Bewertungen

- Essentially - What Does Concrete Sustainability MeanDokument78 SeitenEssentially - What Does Concrete Sustainability MeanLuis Alberto Galvez ParedesNoch keine Bewertungen

- MECH - Valve - Catalogue FFDokument48 SeitenMECH - Valve - Catalogue FFzaidabusamaha95Noch keine Bewertungen

- Argex Mining IncDokument4 SeitenArgex Mining IncjayrammenonNoch keine Bewertungen

- GDP Growth GDP Growth Per Capita Annual %: Assignment 1Dokument1 SeiteGDP Growth GDP Growth Per Capita Annual %: Assignment 1Adnan AqibNoch keine Bewertungen

- Advanced Oxidation Ditch Process and Screw Press Dewatering: Takashi IshidaDokument35 SeitenAdvanced Oxidation Ditch Process and Screw Press Dewatering: Takashi IshidaSebastian Gomez BetancourtNoch keine Bewertungen

- Summer Intern - ReportDokument23 SeitenSummer Intern - Report08mpe026Noch keine Bewertungen

- FMI 3rd QuarterDokument16 SeitenFMI 3rd Quarterjessyl44Noch keine Bewertungen

- Natural Gas MonetizationDokument45 SeitenNatural Gas MonetizationTobias Okoth100% (1)

- World Energy Consumption by Source: Louis Dreyfus Energy ServicesDokument12 SeitenWorld Energy Consumption by Source: Louis Dreyfus Energy ServicesARMANDO HERNANDEZNoch keine Bewertungen

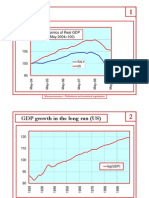

- The Crisis: Dynamics of Real GDP (May 2004 100)Dokument34 SeitenThe Crisis: Dynamics of Real GDP (May 2004 100)Muhammad NaeemNoch keine Bewertungen

- Chinese Steel at CrossroadsDokument31 SeitenChinese Steel at CrossroadsVarun KansalNoch keine Bewertungen

- Firearm Violence: What We Know What To Do: Garen Wintemute, MD, MPHDokument24 SeitenFirearm Violence: What We Know What To Do: Garen Wintemute, MD, MPHNational Press FoundationNoch keine Bewertungen

- Ecopetrol-CCI Asphalt Market Update - Feb162022Dokument26 SeitenEcopetrol-CCI Asphalt Market Update - Feb162022Fabián Quesada UribeNoch keine Bewertungen

- Structures Data SheetDokument1 SeiteStructures Data Sheetkrimchand1825Noch keine Bewertungen

- Tin For The Future Introduction To The Tin Market and The International Tin AssociationDokument4 SeitenTin For The Future Introduction To The Tin Market and The International Tin AssociationRafly Fajar AdiputraNoch keine Bewertungen

- Operations & Supply Chain Management (Unit 3)Dokument31 SeitenOperations & Supply Chain Management (Unit 3)Kiril IlievNoch keine Bewertungen

- The U S Economic Outlook The U.S. Economic OutlookDokument30 SeitenThe U S Economic Outlook The U.S. Economic OutlookZerohedge100% (3)

- NYU 2009 RushmoreDokument30 SeitenNYU 2009 RushmoreJim Butler100% (7)

- O P MishraDokument31 SeitenO P Mishrasanoj kaushikNoch keine Bewertungen

- LME Monthly Overview November 2020 PDFDokument21 SeitenLME Monthly Overview November 2020 PDFMochammad Yaza Azhari BritainNoch keine Bewertungen

- Oil&gasDokument23 SeitenOil&gasPriyankaKesariNoch keine Bewertungen

- Globalization Trends - Guest Lecture May 2023Dokument23 SeitenGlobalization Trends - Guest Lecture May 2023Spare Email AccountNoch keine Bewertungen

- DIA 2010 Presentacion WDCDokument38 SeitenDIA 2010 Presentacion WDCJesús Reinaldo Sanchez AmayaNoch keine Bewertungen

- Entry and Exit in The Public Charity Sector in TheDokument29 SeitenEntry and Exit in The Public Charity Sector in TheBhavesh TrivediNoch keine Bewertungen

- Manufacturing Performance and Services Inputs: Evidence From MalaysiaDokument25 SeitenManufacturing Performance and Services Inputs: Evidence From MalaysiafatincameliaNoch keine Bewertungen

- Chapter 0Dokument32 SeitenChapter 0haigiangofficialNoch keine Bewertungen

- 7th China Nickel Conference May 2010Dokument32 Seiten7th China Nickel Conference May 2010nileshscorpionNoch keine Bewertungen

- (15 Jan) Income Inequality in ASEAN Countries - by Rajah RasiahDokument12 Seiten(15 Jan) Income Inequality in ASEAN Countries - by Rajah Rasiahupnm 1378Noch keine Bewertungen

- Mid Ranja Concept Paper (05-07-2023)Dokument6 SeitenMid Ranja Concept Paper (05-07-2023)Saiba AteeqNoch keine Bewertungen

- WMD2018Dokument263 SeitenWMD2018Álvaro OleasNoch keine Bewertungen

- Real Business Cycles ComDokument30 SeitenReal Business Cycles ComAnubrat SarmaNoch keine Bewertungen

- Steel Industry in Indi1Dokument24 SeitenSteel Industry in Indi1Vatsal JainNoch keine Bewertungen

- T-1 JAPAN'S ECONOMIC DEVELOPMENT Unit 2Dokument28 SeitenT-1 JAPAN'S ECONOMIC DEVELOPMENT Unit 2urbsafeNoch keine Bewertungen

- Fiat SOHC Engine Codes and DimensionsDokument3 SeitenFiat SOHC Engine Codes and DimensionsChrisNoch keine Bewertungen

- RevistasDokument60 SeitenRevistasFreddy E. Pérez CaljaroNoch keine Bewertungen

- MA Material Oct 2021Dokument51 SeitenMA Material Oct 2021Paul GhanimehNoch keine Bewertungen

- Manufacturing of AnilineDokument33 SeitenManufacturing of AnilineYashraj GandhiNoch keine Bewertungen

- Anglo–American Microelectronics Data 1968–69: Manufacturers A–PVon EverandAnglo–American Microelectronics Data 1968–69: Manufacturers A–PNoch keine Bewertungen

- Connector Industry: A Profile of the European Connector Industry - Market Prospects to 1999Von EverandConnector Industry: A Profile of the European Connector Industry - Market Prospects to 1999Noch keine Bewertungen

- Chandoo ProjectDokument42 SeitenChandoo Projectchandoo.upadhyay100% (1)

- CH 06Dokument21 SeitenCH 06chandoo.upadhyayNoch keine Bewertungen

- Chandoo Airtel ProjectDokument60 SeitenChandoo Airtel Projectchandoo.upadhyay100% (21)

- Direct MarketingDokument16 SeitenDirect Marketingchandoo.upadhyayNoch keine Bewertungen

- CH 05Dokument22 SeitenCH 05chandoo.upadhyayNoch keine Bewertungen

- Understanding The Market Environment: Segmenting, Targeting and PositioningDokument14 SeitenUnderstanding The Market Environment: Segmenting, Targeting and Positioningchandoo.upadhyayNoch keine Bewertungen

- Advertising M&MDokument18 SeitenAdvertising M&Mchandoo.upadhyayNoch keine Bewertungen

- Promotion Integrated Marketing CommunicationsDokument23 SeitenPromotion Integrated Marketing CommunicationssupriyarNoch keine Bewertungen

- AluminiumDokument6 SeitenAluminiumchandoo.upadhyayNoch keine Bewertungen

- The International Environment For Promotion and IMCDokument22 SeitenThe International Environment For Promotion and IMCchandoo.upadhyayNoch keine Bewertungen

- Commodity Market of Aluminium: Sourabh SrivastavaDokument11 SeitenCommodity Market of Aluminium: Sourabh Srivastavachandoo.upadhyay0% (1)

- Zinc MarketDokument10 SeitenZinc Marketchandoo.upadhyayNoch keine Bewertungen

- Aluminium Site Presentation 08Dokument24 SeitenAluminium Site Presentation 08cpu1Noch keine Bewertungen

- Credit RatingDokument16 SeitenCredit Ratingchandoo.upadhyay100% (2)

- Ficha Técnica TRIPODE KAYA SAFETY SENTORDokument1 SeiteFicha Técnica TRIPODE KAYA SAFETY SENTORJuan Armas BissoNoch keine Bewertungen

- Why Europe Planned The Great Bank RobberyDokument2 SeitenWhy Europe Planned The Great Bank RobberyRakesh SimhaNoch keine Bewertungen

- 7 Costs of ProductionDokument24 Seiten7 Costs of Productionakshat guptaNoch keine Bewertungen

- Salary Slip (31920472 October, 2017) PDFDokument1 SeiteSalary Slip (31920472 October, 2017) PDFMuhammad Ishaq SonuNoch keine Bewertungen

- Province of AklanDokument3 SeitenProvince of AklanDada N. NahilNoch keine Bewertungen

- Please Quote This Reference Number in All Future CorrespondenceDokument2 SeitenPlease Quote This Reference Number in All Future CorrespondenceSaipraveen PerumallaNoch keine Bewertungen

- Industrialisation in RajasthanDokument4 SeitenIndustrialisation in RajasthanEditor IJTSRDNoch keine Bewertungen

- BioplasticDokument5 SeitenBioplasticclaire bernadaNoch keine Bewertungen

- Rethinking Foreign Aid, SetaDokument5 SeitenRethinking Foreign Aid, SetaAteki Seta CaxtonNoch keine Bewertungen

- Process of Environmental Clerance and The Involve inDokument9 SeitenProcess of Environmental Clerance and The Involve inCharchil SainiNoch keine Bewertungen

- Chapter 8Dokument52 SeitenChapter 8EffeNoch keine Bewertungen

- Moral Education Project: Work of A Financial System and Role of Government in Its Regulation - BYDokument17 SeitenMoral Education Project: Work of A Financial System and Role of Government in Its Regulation - BYshamilNoch keine Bewertungen

- Tanzania Mortgage Market Update 2014Dokument7 SeitenTanzania Mortgage Market Update 2014Anonymous FnM14a0Noch keine Bewertungen

- Project Report of Share KhanDokument117 SeitenProject Report of Share KhanbowsmikaNoch keine Bewertungen

- 2019 Apr 20 Dms Aiu MasterDokument25 Seiten2019 Apr 20 Dms Aiu MasterIrsyad ArifiantoNoch keine Bewertungen

- Income CertificateDokument1 SeiteIncome CertificatedeepakbadimundaNoch keine Bewertungen

- 2019 Marking Scheme Account PDFDokument287 Seiten2019 Marking Scheme Account PDFsaba alamNoch keine Bewertungen

- TYS 2007 To 2019 AnswersDokument380 SeitenTYS 2007 To 2019 Answersshakthee sivakumarNoch keine Bewertungen

- Five Year PlanDokument5 SeitenFive Year PlanrakshaksinghaiNoch keine Bewertungen

- Registration of PropertyDokument13 SeitenRegistration of PropertyambonulanNoch keine Bewertungen

- Tata Vistara - Agency PitchDokument27 SeitenTata Vistara - Agency PitchNishant Prakash0% (1)

- 2023 - Forecast George FriedmanDokument17 Seiten2023 - Forecast George FriedmanGeorge BestNoch keine Bewertungen

- The Importance of Public TransportDokument1 SeiteThe Importance of Public TransportBen RossNoch keine Bewertungen

- Tax Invoice GJ1181910 AK79503Dokument3 SeitenTax Invoice GJ1181910 AK79503AnkitNoch keine Bewertungen

- Gross Domestic ProductDokument3 SeitenGross Domestic ProductAbeer WarraichNoch keine Bewertungen

- Working Capital NumericalsDokument3 SeitenWorking Capital NumericalsShriya SajeevNoch keine Bewertungen