Das könnte Ihnen auch gefallen

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (345)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- Remote Deposit Capture ProjectDokument9 SeitenRemote Deposit Capture ProjectRavi Chandra0% (1)

- Prudential Regulations For Microfinance Banks (MFBS)Dokument23 SeitenPrudential Regulations For Microfinance Banks (MFBS)Abid RasheedNoch keine Bewertungen

- Second Semester Accounting Paper 1Dokument8 SeitenSecond Semester Accounting Paper 1egi.academicinfoNoch keine Bewertungen

- Synopsis Title:-"A Study On Compensation Management in HDFC Bank"Dokument2 SeitenSynopsis Title:-"A Study On Compensation Management in HDFC Bank"saikiabhascoNoch keine Bewertungen

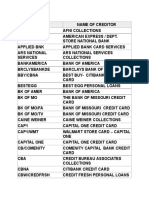

- Creditor AbbreviationsDokument8 SeitenCreditor AbbreviationsAndrés FlórezNoch keine Bewertungen

- Exit 1: Friends and Neighbors: Cross TalkDokument28 SeitenExit 1: Friends and Neighbors: Cross TalkJoyce EnriqueNoch keine Bewertungen

- Fa2 Mock Test 2Dokument7 SeitenFa2 Mock Test 2Sayed Zain ShahNoch keine Bewertungen

- National Bank of PakistanDokument14 SeitenNational Bank of Pakistansarim jawed aziz100% (2)

- SMC vs. KhanDokument19 SeitenSMC vs. KhanGuiller MagsumbolNoch keine Bewertungen

- Lebanese Crisis PDFDokument4 SeitenLebanese Crisis PDFgeorges khairallahNoch keine Bewertungen

- Subprime Mortgage CrisisDokument35 SeitenSubprime Mortgage CrisisParaggNoch keine Bewertungen

- CRMDokument32 SeitenCRMJoel Dsouza100% (1)

- PDF EbooksDokument25 SeitenPDF EbooksS Balagopal SivaprakasamNoch keine Bewertungen

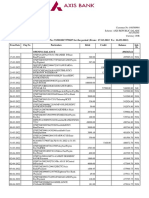

- Statement of Axis Account No:913010017379687 For The Period (From: 17-03-2022 To: 16-09-2022)Dokument7 SeitenStatement of Axis Account No:913010017379687 For The Period (From: 17-03-2022 To: 16-09-2022)Om Namah ShivayNoch keine Bewertungen

- Revised Exam Time Table May 2011Dokument8 SeitenRevised Exam Time Table May 2011nclpjalgaonNoch keine Bewertungen

- Guingona Vs City Fiscal of ManilaDokument6 SeitenGuingona Vs City Fiscal of ManilaSu Kings AbetoNoch keine Bewertungen

- Banks Can't Own Property CASELAWDokument5 SeitenBanks Can't Own Property CASELAWKeith Muhammad: Bey100% (4)

- Comes ADokument209 SeitenComes AAbhishek Rakesh MisraNoch keine Bewertungen

- Project On Micro FinanceDokument44 SeitenProject On Micro Financeredrose_luv23o.in@yahoo.co.in88% (8)

- Chapter 3 2Dokument180 SeitenChapter 3 2dNoch keine Bewertungen

- Hong Dar Impex Co., LTD.: Lten NoDokument2 SeitenHong Dar Impex Co., LTD.: Lten NoSegundo Modesto Romero MallaNoch keine Bewertungen

- February Bank StatementDokument1 SeiteFebruary Bank StatementQuiskeya LLCNoch keine Bewertungen

- Pag Ibig Foreclosed Properties Pubbid 2016-09-14 NCR No DiscountDokument11 SeitenPag Ibig Foreclosed Properties Pubbid 2016-09-14 NCR No DiscountChristian D. OrbeNoch keine Bewertungen

- BRC PDFDokument1 SeiteBRC PDFஇனி ஒரு விதி செய்வோம்Noch keine Bewertungen

- Brgy Reso Availment of Honorarium LoanDokument2 SeitenBrgy Reso Availment of Honorarium LoanErnest Aton97% (37)

- Finance Rti ManualDokument45 SeitenFinance Rti ManualNABARDNoch keine Bewertungen

- PM Event Analyses Report 20110524Dokument29 SeitenPM Event Analyses Report 20110524Bob DijckNoch keine Bewertungen

- NPS LeafletDokument2 SeitenNPS LeafletMOHIT GUPTA jiNoch keine Bewertungen

- Warehouse Receipt Funding - Geared For The Next Trajectory of Growth?Dokument2 SeitenWarehouse Receipt Funding - Geared For The Next Trajectory of Growth?ManojRawatNoch keine Bewertungen