Das könnte Ihnen auch gefallen

- Retailing VocabularyDokument19 SeitenRetailing VocabularyAnand50% (2)

- g90b Plus User ManualDokument50 Seiteng90b Plus User ManualShellnic0% (1)

- Fujifilm EP-6000 Processor - Service Manual PDFDokument445 SeitenFujifilm EP-6000 Processor - Service Manual PDFjames100% (1)

- Exporting Services: A Developing Country PerspectiveVon EverandExporting Services: A Developing Country PerspectiveBewertung: 5 von 5 Sternen5/5 (2)

- Straight Through Processing for Financial Services: The Complete GuideVon EverandStraight Through Processing for Financial Services: The Complete GuideNoch keine Bewertungen

- Business Model of AirtelDokument20 SeitenBusiness Model of Airtelasad siddiqui100% (1)

- Food RetailDokument32 SeitenFood RetailAnand100% (1)

- SMS Call FlowDokument19 SeitenSMS Call FlowKishore Rajput50% (2)

- End-to-End Quality of Service over Cellular Networks: Data Services Performance Optimization in 2G/3GVon EverandEnd-to-End Quality of Service over Cellular Networks: Data Services Performance Optimization in 2G/3GGerardo GomezBewertung: 5 von 5 Sternen5/5 (1)

- Tata Mba Project ReportDokument77 SeitenTata Mba Project ReportDarling AbhiNoch keine Bewertungen

- Bharti 2airtel 1227851581611151 8Dokument49 SeitenBharti 2airtel 1227851581611151 8Ramendra SinghNoch keine Bewertungen

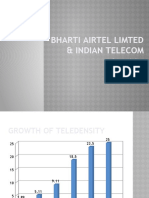

- Bharti Airtel Limted & Indian TelecomDokument18 SeitenBharti Airtel Limted & Indian TelecomAvinash KumarNoch keine Bewertungen

- Bharti 2airtel 1227851581611151 8Dokument49 SeitenBharti 2airtel 1227851581611151 8mayankvohraNoch keine Bewertungen

- Strategic Management Group AssignmentDokument15 SeitenStrategic Management Group Assignmentabhishek guptaNoch keine Bewertungen

- Icfai National College: JaipurDokument15 SeitenIcfai National College: JaipurShelly BhartiNoch keine Bewertungen

- Annual Report of Airtel: - A.VinaykumarDokument49 SeitenAnnual Report of Airtel: - A.VinaykumarVinay KumarNoch keine Bewertungen

- AIRTELDokument49 SeitenAIRTELSaroj MuduliNoch keine Bewertungen

- AirtelDokument62 SeitenAirtelMahesh SindhaNoch keine Bewertungen

- Hutch Vodafone Idea DealDokument13 SeitenHutch Vodafone Idea DealCHINMAY SANKHENoch keine Bewertungen

- Bharti Airtel LTD and Indian Telecom SectorDokument14 SeitenBharti Airtel LTD and Indian Telecom SectorNishant GoldyNoch keine Bewertungen

- Ethiopia Success and Failure Under MonopolyDokument29 SeitenEthiopia Success and Failure Under MonopolySamuel GetachewNoch keine Bewertungen

- World Mobile Equipment Market Growth PredictedDokument3 SeitenWorld Mobile Equipment Market Growth PredictedsusansumamaNoch keine Bewertungen

- Challenges To Indian GrowthDokument40 SeitenChallenges To Indian GrowthVarsha BhutraNoch keine Bewertungen

- Cellular War in India - 2010Dokument38 SeitenCellular War in India - 2010Mohammad Iqbal Khan100% (1)

- Reliance Communications: Group 8 Presented By: Nichelle Kamath Mitali Mistry Komal Tambade - F65 Mansi Morajkar - F39Dokument31 SeitenReliance Communications: Group 8 Presented By: Nichelle Kamath Mitali Mistry Komal Tambade - F65 Mansi Morajkar - F39sachinborade11997Noch keine Bewertungen

- PerformanceDokument60 SeitenPerformancevivek dhankharNoch keine Bewertungen

- Interim Report On Telecom Industry in 2010Dokument13 SeitenInterim Report On Telecom Industry in 2010HEM BANSALNoch keine Bewertungen

- India Telecom Market OverviewDokument4 SeitenIndia Telecom Market Overviewprince vivekNoch keine Bewertungen

- Project on Bharti-Airtel's History and FinancialsDokument19 SeitenProject on Bharti-Airtel's History and Financialsak3372Noch keine Bewertungen

- Bharti-Airtel StrategyDokument52 SeitenBharti-Airtel Strategyshree0312Noch keine Bewertungen

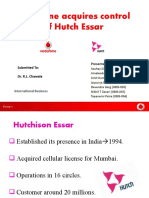

- Vodafone acquires control of Hutch EssarDokument30 SeitenVodafone acquires control of Hutch EssarvidhijagnaniNoch keine Bewertungen

- Teleco M Sector: BY: Nitin Agarwal Ashu Sahu Ishan Sharma Aitrey Banerjee Rohit MathurDokument42 SeitenTeleco M Sector: BY: Nitin Agarwal Ashu Sahu Ishan Sharma Aitrey Banerjee Rohit MathurashusahuNoch keine Bewertungen

- Dynamics of Indian Telecom Industry 2009 v8Dokument42 SeitenDynamics of Indian Telecom Industry 2009 v8jmadariNoch keine Bewertungen

- No.C/l, G Block, Bandra - Kurla ComplexDokument25 SeitenNo.C/l, G Block, Bandra - Kurla ComplexBhaskar DasguptaNoch keine Bewertungen

- Airtel1 Group GDokument20 SeitenAirtel1 Group GTushar PadoleNoch keine Bewertungen

- AirtelDokument19 SeitenAirtelsaurabh698100% (3)

- Presentation on Consumer Electronics MarketDokument30 SeitenPresentation on Consumer Electronics MarketRakesh SikdarNoch keine Bewertungen

- Presented To Prof. Veenu AroraDokument28 SeitenPresented To Prof. Veenu AroraAnushka GogoiNoch keine Bewertungen

- Bharti 2airtel 1227851581611151 8Dokument48 SeitenBharti 2airtel 1227851581611151 8Venkat NatarajanNoch keine Bewertungen

- EFY-Top100 Oct09 PDFDokument15 SeitenEFY-Top100 Oct09 PDFEnoch L SNoch keine Bewertungen

- Source: From 20 OCT, 2010 From 20 OCT, 2010Dokument13 SeitenSource: From 20 OCT, 2010 From 20 OCT, 2010nandinee15Noch keine Bewertungen

- Telecom Sector: Presented by Pallavi.B - 66 Mms MarketingDokument48 SeitenTelecom Sector: Presented by Pallavi.B - 66 Mms MarketingpaalveeNoch keine Bewertungen

- Marketing Strategy of Airtel and Its Promotional Strategy.Dokument48 SeitenMarketing Strategy of Airtel and Its Promotional Strategy.mbogadhiNoch keine Bewertungen

- Top IT Companies in IndiaDokument15 SeitenTop IT Companies in Indiavenkatesh_1829Noch keine Bewertungen

- About AirtelDokument31 SeitenAbout AirtelVignesh GuruNoch keine Bewertungen

- Shaikha Al-Jabir - Strategic InnovationDokument12 SeitenShaikha Al-Jabir - Strategic InnovationictQATARNoch keine Bewertungen

- Project Report 10Dokument20 SeitenProject Report 10mukiejainNoch keine Bewertungen

- Bharti Airtel Ltd. Research Insight-3: General OverviewDokument6 SeitenBharti Airtel Ltd. Research Insight-3: General OverviewDHRUVI KOTHARINoch keine Bewertungen

- Economics ProjectDokument22 SeitenEconomics ProjectM HABIBULLAHNoch keine Bewertungen

- Telecommunicati On Industry: Reliance JioDokument10 SeitenTelecommunicati On Industry: Reliance JioDineshNoch keine Bewertungen

- Telecom Industry in IndiaDokument13 SeitenTelecom Industry in IndiaGopesh kumar AcharyaNoch keine Bewertungen

- Customer Satisfaction Towards Cellular Services - A Study of Idea Cell Ular"Malwa Market"In PunjabDokument8 SeitenCustomer Satisfaction Towards Cellular Services - A Study of Idea Cell Ular"Malwa Market"In PunjabRakshith RaoNoch keine Bewertungen

- BhartiDokument9 SeitenBhartiabhijitNoch keine Bewertungen

- Business Economics TELECOMMUNICATIONDokument24 SeitenBusiness Economics TELECOMMUNICATIONM HABIBULLAHNoch keine Bewertungen

- Telecom Sector ReportDokument21 SeitenTelecom Sector ReportMohammed SaadiNoch keine Bewertungen

- Download Bharti Airtel PPT and learn about India's largest telecom companyDokument49 SeitenDownload Bharti Airtel PPT and learn about India's largest telecom companyManish TiwariNoch keine Bewertungen

- India's $64B IT-ITES Export Industry Market OverviewDokument27 SeitenIndia's $64B IT-ITES Export Industry Market Overviewarkaprava ghoshNoch keine Bewertungen

- India After 25 YearsDokument25 SeitenIndia After 25 Yearsasad siddiquiNoch keine Bewertungen

- Tata GroupDokument58 SeitenTata GroupSaurabh G100% (1)

- Presented To:-: Prof. KamleshDokument31 SeitenPresented To:-: Prof. KamleshRashmi GandhiNoch keine Bewertungen

- Tales from the Development Frontier: How China and Other Countries Harness Light Manufacturing to Create Jobs and ProsperityVon EverandTales from the Development Frontier: How China and Other Countries Harness Light Manufacturing to Create Jobs and ProsperityNoch keine Bewertungen

- Telecommunications: Present Status and Future TrendsVon EverandTelecommunications: Present Status and Future TrendsBewertung: 4.5 von 5 Sternen4.5/5 (2)

- The Mobile Multimedia Business: Requirements and SolutionsVon EverandThe Mobile Multimedia Business: Requirements and SolutionsNoch keine Bewertungen

- Profile of the Worldwide Semiconductor Industry - Market Prospects to 1997: Market Prospects to 1997Von EverandProfile of the Worldwide Semiconductor Industry - Market Prospects to 1997: Market Prospects to 1997Noch keine Bewertungen

- Sales PromotionDokument11 SeitenSales PromotionAnand0% (1)

- Generic StrategiesDokument32 SeitenGeneric StrategiesAnandNoch keine Bewertungen

- Sales ForecastingDokument16 SeitenSales ForecastingAnandNoch keine Bewertungen

- Agile ManufacturingDokument23 SeitenAgile ManufacturingAnand100% (2)

- Software AgentsDokument27 SeitenSoftware AgentsAnandNoch keine Bewertungen

- Corporate Digital LibraryDokument14 SeitenCorporate Digital LibraryAnand86% (7)

- Module 8 Media Strategy 2003Dokument21 SeitenModule 8 Media Strategy 2003AnandNoch keine Bewertungen

- Module 4 Role of Persusion in Marketing Communication 2003Dokument14 SeitenModule 4 Role of Persusion in Marketing Communication 2003Anand100% (1)

- Module 3 Consumer Behavior 2003Dokument13 SeitenModule 3 Consumer Behavior 2003AnandNoch keine Bewertungen

- Module 6 Creative Strategy - Planning and Development 2003Dokument9 SeitenModule 6 Creative Strategy - Planning and Development 2003AnandNoch keine Bewertungen

- Beer & Wine Osd PresDokument18 SeitenBeer & Wine Osd PresAnand100% (1)

- Module 2 Communication Process 2003Dokument13 SeitenModule 2 Communication Process 2003AnandNoch keine Bewertungen

- AnandDokument45 SeitenAnandAnandNoch keine Bewertungen

- TransportationDokument155 SeitenTransportationAnand100% (3)

- Venture CapitalDokument16 SeitenVenture CapitalAnand100% (1)

- Presented By:: Anand Kumar JU07019 NSB School of Business, New DelhiDokument8 SeitenPresented By:: Anand Kumar JU07019 NSB School of Business, New DelhiAnand100% (1)

- Ad TrendsDokument19 SeitenAd TrendsAnandNoch keine Bewertungen

- Alcohol Facts: Mr. Anand KumarDokument31 SeitenAlcohol Facts: Mr. Anand KumarAnandNoch keine Bewertungen

- Transshipment LPPDokument10 SeitenTransshipment LPPAnandNoch keine Bewertungen

- OneExpert 630 Extended QuickStart Guide V1aDokument153 SeitenOneExpert 630 Extended QuickStart Guide V1ajuan guillermo zapataNoch keine Bewertungen

- Is It Possible To Modify The Output Voltage/current of An Smps ???Dokument3 SeitenIs It Possible To Modify The Output Voltage/current of An Smps ???Delos Santos JojoNoch keine Bewertungen

- How To Calibrate Your Equipment Using Color BarsDokument6 SeitenHow To Calibrate Your Equipment Using Color BarsAnirban GhoseNoch keine Bewertungen

- How2electronics Com BLDC Brushless DC Motor Driver Circuit 555Dokument10 SeitenHow2electronics Com BLDC Brushless DC Motor Driver Circuit 555Janet WaldeNoch keine Bewertungen

- HXGX 7Dokument112 SeitenHXGX 7Tony WahlgrenNoch keine Bewertungen

- HVDC Transmission and Short Circuit CurrentDokument2 SeitenHVDC Transmission and Short Circuit CurrentManasa ReddyNoch keine Bewertungen

- Wireless E Notice BoardDokument5 SeitenWireless E Notice Board1200miqaelNoch keine Bewertungen

- EC 8392 COMMUNICATION ENGINEERING QUESTION BANK ANALOG AND PULSE MODULATIONDokument16 SeitenEC 8392 COMMUNICATION ENGINEERING QUESTION BANK ANALOG AND PULSE MODULATIONDinesh Kumar RNoch keine Bewertungen

- Device 3 Connection GuideDokument9 SeitenDevice 3 Connection Guidemochammad aripinNoch keine Bewertungen

- Iot Based Weather Station Using GSMDokument5 SeitenIot Based Weather Station Using GSMPooja Ban100% (1)

- Mypin: L Series Weighing Batching Controller Instruction ManualDokument1 SeiteMypin: L Series Weighing Batching Controller Instruction ManualSales GISNoch keine Bewertungen

- Migration To Softswitch Solutions: Paul Brittain Product Manager, MetaswitchDokument13 SeitenMigration To Softswitch Solutions: Paul Brittain Product Manager, Metaswitchnguyenductanhn85Noch keine Bewertungen

- SISTEM PENOMORAN AKTIVA ASSET NUMBERING SYSTEMDokument130 SeitenSISTEM PENOMORAN AKTIVA ASSET NUMBERING SYSTEMDior L TobingNoch keine Bewertungen

- 4-2-2 How To Access Service Mode: Standby Info Power On Menu MuteDokument20 Seiten4-2-2 How To Access Service Mode: Standby Info Power On Menu MuteWelkin SkyNoch keine Bewertungen

- JunipericonsDokument30 SeitenJunipericonsAndri AndriyanNoch keine Bewertungen

- DekTec DTE-3137Dokument7 SeitenDekTec DTE-3137Alexander WieseNoch keine Bewertungen

- TDR900 QuickStartGuide PDFDokument2 SeitenTDR900 QuickStartGuide PDFmiamor$44Noch keine Bewertungen

- Ref 550Dokument14 SeitenRef 550Dario AbelNoch keine Bewertungen

- Works With QSC DCP 200 and 300 Cinema Processors To Create The Most Powerful Networked Audio Solution For CinemaDokument2 SeitenWorks With QSC DCP 200 and 300 Cinema Processors To Create The Most Powerful Networked Audio Solution For CinemaguerreroNoch keine Bewertungen

- Asmi-51: 2-Wire 2.3 Mbps MSDSL ModemDokument4 SeitenAsmi-51: 2-Wire 2.3 Mbps MSDSL ModemManuel FreireNoch keine Bewertungen

- A High-Performance FIR Filter Architecture For Fixed and Reconfigurable ApplicationsDokument5 SeitenA High-Performance FIR Filter Architecture For Fixed and Reconfigurable ApplicationsshaliniNoch keine Bewertungen

- Max31855 PDFDokument13 SeitenMax31855 PDFAlfredoSanchezPlaNoch keine Bewertungen

- Samson 7kit PDFDokument12 SeitenSamson 7kit PDFFernando Dario AvilaNoch keine Bewertungen

- Data Sheet: Very Low Dropout Voltage/quiescent Current 5 V Voltage RegulatorDokument16 SeitenData Sheet: Very Low Dropout Voltage/quiescent Current 5 V Voltage RegulatorPablo CiravegnaNoch keine Bewertungen

- (GUIDE) 1st Generation Intel HD Graphics QE:CI - Intel - InsanelyMac ForumDokument44 Seiten(GUIDE) 1st Generation Intel HD Graphics QE:CI - Intel - InsanelyMac Forumnono heryanaNoch keine Bewertungen

- C-Media CMI8738 4 Channel Sound Card: User ManualDokument5 SeitenC-Media CMI8738 4 Channel Sound Card: User ManualGustavo Rosales OrozcoNoch keine Bewertungen

- Malvino MCQDokument27 SeitenMalvino MCQjedminayNoch keine Bewertungen