Das könnte Ihnen auch gefallen

- AAC Plant OpEx and CapEx Rev2Dokument8 SeitenAAC Plant OpEx and CapEx Rev2Kevin CariñoNoch keine Bewertungen

- Construction ManualDokument278 SeitenConstruction ManualUnnikrishnan NairNoch keine Bewertungen

- Ca Final - Ama (Costing) Theory Notes: Amogh Ashtaputre @amoghashtaputre Amogh Ashtaputre Amogh AshtaputreDokument143 SeitenCa Final - Ama (Costing) Theory Notes: Amogh Ashtaputre @amoghashtaputre Amogh Ashtaputre Amogh AshtaputreB GANAPATHY100% (1)

- Rajiv Dua Bsc. (Eng), PMP: Managing Cost Overruns and Project ManagementDokument193 SeitenRajiv Dua Bsc. (Eng), PMP: Managing Cost Overruns and Project Managementfhsn84Noch keine Bewertungen

- Estimation - Construction Time ManagementDokument24 SeitenEstimation - Construction Time ManagementJuanaNoch keine Bewertungen

- Iia Global Internal Audit Standards Public Comment Draft English v2Dokument132 SeitenIia Global Internal Audit Standards Public Comment Draft English v2harshimadushaniNoch keine Bewertungen

- Elements of CostingDokument171 SeitenElements of Costingiisjaffer100% (1)

- 1-4-2 Scheduling Techniques For ConstructionDokument47 Seiten1-4-2 Scheduling Techniques For ConstructionVũ Thị Hà TrangNoch keine Bewertungen

- Survey Study of The RequirementDokument128 SeitenSurvey Study of The Requirementapi-3839680Noch keine Bewertungen

- Cost Estimation Manual Manual Number SM014Dokument0 SeitenCost Estimation Manual Manual Number SM014pankajmayNoch keine Bewertungen

- Manhour Rate INKADokument3 SeitenManhour Rate INKADeny ArifiantoNoch keine Bewertungen

- (PDF) Schedule of Rates For Civil Works Public Works DepartmentDokument407 Seiten(PDF) Schedule of Rates For Civil Works Public Works DepartmentRadha Vaibhav VaishNoch keine Bewertungen

- 10 Estimation Function PT Q2Dokument61 Seiten10 Estimation Function PT Q2Varundeep SinghalNoch keine Bewertungen

- UD06737B-A Baseline Fingerprint Time Attendance Termimal User Manual V1.1.1 20180502Dokument144 SeitenUD06737B-A Baseline Fingerprint Time Attendance Termimal User Manual V1.1.1 20180502davaasuren jargalsaihanNoch keine Bewertungen

- BI Course Ebook PDFDokument22 SeitenBI Course Ebook PDFQorina AzizahNoch keine Bewertungen

- 1 PMHB Complete PDFDokument357 Seiten1 PMHB Complete PDFTayyiba ImranNoch keine Bewertungen

- Construction Planning: Choosing Tech and Defining TasksDokument198 SeitenConstruction Planning: Choosing Tech and Defining TasksHajarath Prasad AbburuNoch keine Bewertungen

- Contractora Estimate Cost - Propelat RapDokument192 SeitenContractora Estimate Cost - Propelat RapMr. RudyNoch keine Bewertungen

- Task 1 BDokument159 SeitenTask 1 Bpentyala88Noch keine Bewertungen

- Overhead Guidance PDFDokument9 SeitenOverhead Guidance PDFanuarNoch keine Bewertungen

- Em - 1110 3 136Dokument203 SeitenEm - 1110 3 136Real VinchenzoNoch keine Bewertungen

- Acounting Atve Summarised NotesDokument118 SeitenAcounting Atve Summarised NotesFolegwe FolegweNoch keine Bewertungen

- S Telp RDB 5279259Dokument14 SeitenS Telp RDB 5279259Pablo NuñezNoch keine Bewertungen

- Project Execution Plan - TemplateDokument12 SeitenProject Execution Plan - TemplateTonny SuakNoch keine Bewertungen

- 2014 Handbook External Costs TransportDokument139 Seiten2014 Handbook External Costs TransportEdoardo CecereNoch keine Bewertungen

- Rig Weight NormsDokument1 SeiteRig Weight NormsDPSprojectsNoch keine Bewertungen

- Dissertation - Delay Analysis TechniqueDokument167 SeitenDissertation - Delay Analysis Techniqueparkjiho79Noch keine Bewertungen

- Engineer ContractingDokument114 SeitenEngineer ContractingAndrew ReidNoch keine Bewertungen

- Selection of Consultants: Request For Proposals Consulting ServicesDokument164 SeitenSelection of Consultants: Request For Proposals Consulting ServicesRani Arun ShakarNoch keine Bewertungen

- Manhour MastersDokument60 SeitenManhour MastersMeetNoch keine Bewertungen

- Construction Master ManualDokument108 SeitenConstruction Master ManualBrian leerNoch keine Bewertungen

- Work ManualDokument684 SeitenWork ManualshashiNoch keine Bewertungen

- Manhour SampleDokument4 SeitenManhour SampleAhmed SaidNoch keine Bewertungen

- Measuring Concrete Work 1Dokument19 SeitenMeasuring Concrete Work 1Akbar RafeekNoch keine Bewertungen

- EPC-2018.10.29-Amendment in Standard RFP - AE BILLINGDokument2 SeitenEPC-2018.10.29-Amendment in Standard RFP - AE BILLINGPremNoch keine Bewertungen

- Costing Materials TombstoneDokument2 SeitenCosting Materials TombstoneMark Anthony Carreon MalateNoch keine Bewertungen

- 2013 Actual Man HourDokument907 Seiten2013 Actual Man HourwessamalexNoch keine Bewertungen

- Open Version Cost Estimation ManualDokument252 SeitenOpen Version Cost Estimation ManualDennis MagajaNoch keine Bewertungen

- Strengthening 49 km of NH-2B in West BengalDokument102 SeitenStrengthening 49 km of NH-2B in West BengalOllie BhattNoch keine Bewertungen

- 4.mechanical (Qa)Dokument22 Seiten4.mechanical (Qa)Osama AzaiemNoch keine Bewertungen

- S ProjectDefinitionOnOffshore PetrofacDokument4 SeitenS ProjectDefinitionOnOffshore PetrofacDiego1980bNoch keine Bewertungen

- W3 - Week 3 Project ManagementDokument53 SeitenW3 - Week 3 Project ManagementEe Ling SawNoch keine Bewertungen

- Carl N. Anderson Bayard E. Bosserman Il Charles D. Morris Contri Butors Casi Cadrecha Joseph E. Lescovich Harvey W. Taylor John VuncannonDokument15 SeitenCarl N. Anderson Bayard E. Bosserman Il Charles D. Morris Contri Butors Casi Cadrecha Joseph E. Lescovich Harvey W. Taylor John Vuncannonshady mohamedNoch keine Bewertungen

- Description Brand U/M Item NO Unit Price (AED) Total Price (AED)Dokument9 SeitenDescription Brand U/M Item NO Unit Price (AED) Total Price (AED)rageshdinesh23Noch keine Bewertungen

- Delft Management of Engineering ProjectsDokument222 SeitenDelft Management of Engineering ProjectsEirinaios ChatzillariNoch keine Bewertungen

- 10 State Standards - Waste Water FacilitiesDokument178 Seiten10 State Standards - Waste Water Facilitiesblin254Noch keine Bewertungen

- Contract DocumentDokument109 SeitenContract DocumentEngineeri TadiyosNoch keine Bewertungen

- UPDATED New Cost Estimation Manual FinalDokument26 SeitenUPDATED New Cost Estimation Manual FinalBerihun AddisNoch keine Bewertungen

- Project WBS EstimateDokument6 SeitenProject WBS EstimateSatria PinanditaNoch keine Bewertungen

- Promineo Cost EPC Tips & Tricks Webinar HighlightsDokument37 SeitenPromineo Cost EPC Tips & Tricks Webinar Highlightspthakur234Noch keine Bewertungen

- Dolidar Norms AdendumDokument33 SeitenDolidar Norms AdendumKiran Kumar AcharyaNoch keine Bewertungen

- Productivity Analysis of EPC WorksDokument8 SeitenProductivity Analysis of EPC Workssimeonochiche3640Noch keine Bewertungen

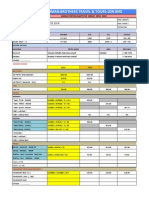

- Rahman Brothers Travel Costing Sheet for 12D 10N Umrah PackageDokument16 SeitenRahman Brothers Travel Costing Sheet for 12D 10N Umrah PackagehanijibrilNoch keine Bewertungen

- Cordelia Project B2-105 Costing ScheduleDokument4 SeitenCordelia Project B2-105 Costing ScheduleMallikarjun PatilNoch keine Bewertungen

- Case-Based Cost Estimation PDFDokument160 SeitenCase-Based Cost Estimation PDFanshu_foruNoch keine Bewertungen

- Capital BudgetingDokument45 SeitenCapital BudgetingdawncpainNoch keine Bewertungen

- Capital Budgeting DecisionsDokument28 SeitenCapital Budgeting DecisionsMoshmi MazumdarNoch keine Bewertungen

- Capital Budgeting MaterialDokument64 SeitenCapital Budgeting Materialvarghees prabhu.sNoch keine Bewertungen

- VI. Capital Budgeting Under Certainty: Professors Simon Pak and John ZdanowiczDokument56 SeitenVI. Capital Budgeting Under Certainty: Professors Simon Pak and John ZdanowiczSonal Power UnlimitdNoch keine Bewertungen

- Statement of Cash Flows: Preparation, Presentation, and UseVon EverandStatement of Cash Flows: Preparation, Presentation, and UseNoch keine Bewertungen

- Term PlanDokument4 SeitenTerm PlanKaushaljm PatelNoch keine Bewertungen

- Macroeconomics Jargons: University of Caloocan CityDokument16 SeitenMacroeconomics Jargons: University of Caloocan CityMyriz AlvarezNoch keine Bewertungen

- Bab I Persamaan Dasar AkuntansiDokument8 SeitenBab I Persamaan Dasar Akuntansiakhmad fauzanNoch keine Bewertungen

- Public Sector Debt Statistical Bulletin No 43 1Dokument57 SeitenPublic Sector Debt Statistical Bulletin No 43 1getupfrontNoch keine Bewertungen

- Fundamental #28 Have A Bias For Structure and Rebar.Dokument9 SeitenFundamental #28 Have A Bias For Structure and Rebar.David FriedmanNoch keine Bewertungen

- RM - Mcom Sem 4Dokument37 SeitenRM - Mcom Sem 4Suryakant FulpagarNoch keine Bewertungen

- Global Construction Paints and Coatings PDFDokument384 SeitenGlobal Construction Paints and Coatings PDFSunny JoonNoch keine Bewertungen

- Investors Preference in Commodities MarketDokument8 SeitenInvestors Preference in Commodities MarketSundar RajNoch keine Bewertungen

- Three questions to grow your investment returnsDokument21 SeitenThree questions to grow your investment returnsMOVIES SHOPNoch keine Bewertungen

- DrewDokument2 SeitenDrewmusunna galibNoch keine Bewertungen

- Comparison of The Markowitz and Single Index Model Based On M-V Criterion in Optimal Portfolio FormationDokument6 SeitenComparison of The Markowitz and Single Index Model Based On M-V Criterion in Optimal Portfolio FormationPavan KumarNoch keine Bewertungen

- Original Proposal of Georgia Bank and Trust To Columbia County For Banking ServicesDokument20 SeitenOriginal Proposal of Georgia Bank and Trust To Columbia County For Banking ServicesAllie M GrayNoch keine Bewertungen

- C C 2021 Cfa® E: Ritical Oncepts For The XamDokument6 SeitenC C 2021 Cfa® E: Ritical Oncepts For The XamGonzaloNoch keine Bewertungen

- PU 4 YEARS BBA IV Semester SyllabusDokument15 SeitenPU 4 YEARS BBA IV Semester SyllabushimalayabanNoch keine Bewertungen

- Week 7 - Financial Management 23Dokument59 SeitenWeek 7 - Financial Management 23jeff28Noch keine Bewertungen

- Soal Latihan Penilaian SahamDokument6 SeitenSoal Latihan Penilaian SahamAchmad Syafi'iNoch keine Bewertungen

- Liken Vs ShafferDokument1 SeiteLiken Vs ShafferMikhail JavierNoch keine Bewertungen

- Fera and Fema: Submitted To: Prof. Anant AmdekarDokument40 SeitenFera and Fema: Submitted To: Prof. Anant AmdekarhasbicNoch keine Bewertungen

- The Yamuna Syndicate Limited: Ratings Upgraded Summary of Rating ActionDokument8 SeitenThe Yamuna Syndicate Limited: Ratings Upgraded Summary of Rating ActionSandy SanNoch keine Bewertungen

- Overconfidence Bias in ThirukkuralDokument3 SeitenOverconfidence Bias in ThirukkuralEditor IJTSRDNoch keine Bewertungen

- 17 PHD Directory F LRDokument16 Seiten17 PHD Directory F LRchetanaNoch keine Bewertungen

- Fiscal PolicyDokument13 SeitenFiscal PolicyAakash SaxenaNoch keine Bewertungen

- International Business & Trade Research Paper ReviewDokument3 SeitenInternational Business & Trade Research Paper ReviewKiyan YunNoch keine Bewertungen

- 2005 10 XBRL Progress ReportDokument18 Seiten2005 10 XBRL Progress ReportkjheiinNoch keine Bewertungen

- CFA1 (2011) Corporate FinanceDokument9 SeitenCFA1 (2011) Corporate FinancenilakashNoch keine Bewertungen

- Solution Past Paper Higher-Series4-08hkDokument16 SeitenSolution Past Paper Higher-Series4-08hkJoyce LimNoch keine Bewertungen

- Case Study Presentation-Consumer BehaviourDokument26 SeitenCase Study Presentation-Consumer BehaviourPravakar KumarNoch keine Bewertungen

- Experience of Inflation Targeting in South AfricaDokument31 SeitenExperience of Inflation Targeting in South AfricaAmmi JulianNoch keine Bewertungen

- Chap 7 Slides Risk ManagementDokument43 SeitenChap 7 Slides Risk ManagementSinpaoNoch keine Bewertungen

- The Global Economic Crisis and The Nigerian Financial SystemDokument35 SeitenThe Global Economic Crisis and The Nigerian Financial SystemKing JoeNoch keine Bewertungen