Das könnte Ihnen auch gefallen

- Kosten- und Leistungsrechnung: Mit Aufgaben und DefinitionenVon EverandKosten- und Leistungsrechnung: Mit Aufgaben und DefinitionenNoch keine Bewertungen

- RechnungswesenDokument4 SeitenRechnungswesenKamil RosiakNoch keine Bewertungen

- Begriffe Aus Dem RechnungswesenDokument6 SeitenBegriffe Aus Dem RechnungswesenDubravka MikalackiNoch keine Bewertungen

- Finanzmanagement souverän meistern: Finanz- und Kostenmanagement erfolgreich umsetzenVon EverandFinanzmanagement souverän meistern: Finanz- und Kostenmanagement erfolgreich umsetzenNoch keine Bewertungen

- Die Grundbegriffe Des Betrieblichen RechnungswesensDokument44 SeitenDie Grundbegriffe Des Betrieblichen Rechnungswesensjdi badrNoch keine Bewertungen

- Rechnungswesen - Aufgaben Mit Lösung - SS 2007 (Powered by Raute-Wirtschaft - De)Dokument64 SeitenRechnungswesen - Aufgaben Mit Lösung - SS 2007 (Powered by Raute-Wirtschaft - De)Olga KatrychNoch keine Bewertungen

- Steuerlehre 1Dokument11 SeitenSteuerlehre 1jan RistauNoch keine Bewertungen

- BWR SkriptDokument26 SeitenBWR SkriptKatrinSchneiderNoch keine Bewertungen

- 09 Handout InvestitionsrechnungDokument12 Seiten09 Handout InvestitionsrechnungmoSphaereNoch keine Bewertungen

- 1 Lernzettel MADokument12 Seiten1 Lernzettel MAjonashagen12Noch keine Bewertungen

- Übung Zur Rechnungslegung Nach IfRSDokument6 SeitenÜbung Zur Rechnungslegung Nach IfRSStefan ZwingelNoch keine Bewertungen

- Bilanzorientierte Kennzahlen Für Wertorientierte SteuerungDokument5 SeitenBilanzorientierte Kennzahlen Für Wertorientierte SteuerungStefan SchmidtNoch keine Bewertungen

- 2022 D LösungenDokument99 Seiten2022 D LösungenNastyaNoch keine Bewertungen

- Ki Theorie KLRDokument3 SeitenKi Theorie KLRminecraft danielNoch keine Bewertungen

- Modulabschlussklausur BB02 SS2018Dokument2 SeitenModulabschlussklausur BB02 SS2018Elena RNoch keine Bewertungen

- Kapitel 2 Fragebogen Zur Verwaltungsbuchhaltung David Noel Ramírez PadillaDokument7 SeitenKapitel 2 Fragebogen Zur Verwaltungsbuchhaltung David Noel Ramírez PadillaScribdTranslationsNoch keine Bewertungen

- Kurzfassung 6.8 PDFDokument10 SeitenKurzfassung 6.8 PDFCatalin LeucutaNoch keine Bewertungen

- Vergleich FIBUDokument3 SeitenVergleich FIBUkzx97853Noch keine Bewertungen

- Ges. WDH 2 KalkulationDokument7 SeitenGes. WDH 2 KalkulationJan LührsenNoch keine Bewertungen

- 64 SSC - BP - MUSTERPRÜFUNG - Finanz - Und Rechnungswesen 2 Mit LösungsansatzDokument8 Seiten64 SSC - BP - MUSTERPRÜFUNG - Finanz - Und Rechnungswesen 2 Mit LösungsansatzSiegler PascalNoch keine Bewertungen

- Mündliches Kostenrechnung 2Dokument5 SeitenMündliches Kostenrechnung 2dilarakatirciNoch keine Bewertungen

- Doppik GemeindenDokument13 SeitenDoppik GemeindenXxx XexoNoch keine Bewertungen

- Multiple-Choice-Aufgaben Vom 2.04.2019 + LösungDokument4 SeitenMultiple-Choice-Aufgaben Vom 2.04.2019 + LösungMartinNoch keine Bewertungen

- MBA-Aktivität 1 M3 2011Dokument10 SeitenMBA-Aktivität 1 M3 2011ScribdTranslationsNoch keine Bewertungen

- Ü B U N G S A U F G A B e NDokument14 SeitenÜ B U N G S A U F G A B e NBoki BorisNoch keine Bewertungen

- Bilanzierung PrüfungpdfDokument4 SeitenBilanzierung Prüfungpdfadamoropeza089Noch keine Bewertungen

- Grundlegendes Buchhaltungsquiz Mit AntwortenDokument7 SeitenGrundlegendes Buchhaltungsquiz Mit AntwortenScribdTranslationsNoch keine Bewertungen

- ... Übungen Kapitel 14Dokument6 Seiten... Übungen Kapitel 14ScribdTranslationsNoch keine Bewertungen

- Financial Accounting I Week 2 PDokument4 SeitenFinancial Accounting I Week 2 PScribdTranslationsNoch keine Bewertungen

- 2021-10-08 SID Rewe HS21 Stud-o-LösDokument35 Seiten2021-10-08 SID Rewe HS21 Stud-o-LöslaneherdeNoch keine Bewertungen

- Investments BasicsDokument37 SeitenInvestments BasicsSharon GnNoch keine Bewertungen

- Skript KLR Grundlagen Bereich TeilkostenrechnungDokument26 SeitenSkript KLR Grundlagen Bereich TeilkostenrechnungfabetayfunNoch keine Bewertungen

- WirtschaftDokument7 SeitenWirtschaftMatthias Brandl0% (1)

- 2022 BuR Quiz 1 (Probequiz) LösungenDokument2 Seiten2022 BuR Quiz 1 (Probequiz) Lösungenzifi jusufiNoch keine Bewertungen

- VO Bilanzierung WS2122 Kap6Dokument52 SeitenVO Bilanzierung WS2122 Kap6MelissaNoch keine Bewertungen

- Banking Finance IDokument20 SeitenBanking Finance I88j5mpfq6hNoch keine Bewertungen

- 60 ReleaseinfoDokument88 Seiten60 ReleaseinfoMelinda BugleditsNoch keine Bewertungen

- RDB Tso LIdja20220405Dokument4 SeitenRDB Tso LIdja20220405benedikt thurnherNoch keine Bewertungen

- Konzeptionelle Karte Der Arten Von Budgets.Dokument1 SeiteKonzeptionelle Karte Der Arten Von Budgets.ScribdTranslationsNoch keine Bewertungen

- Schulaufgabe BWR Komplett 2Dokument10 SeitenSchulaufgabe BWR Komplett 2veri_harle2209100% (1)

- 2.2.2 Bar - Und Einzugsliquidität - S-1Dokument2 Seiten2.2.2 Bar - Und Einzugsliquidität - S-1gamingbaitorgNoch keine Bewertungen

- 2021-10-01 SID Rewe HS21 Stud-o-LösDokument45 Seiten2021-10-01 SID Rewe HS21 Stud-o-LöslaneherdeNoch keine Bewertungen

- Modulabschlussklausur BB02 WS2018 2019Dokument2 SeitenModulabschlussklausur BB02 WS2018 2019Elena RNoch keine Bewertungen

- Conversionzauber Finanzsektor LeitfadenDokument34 SeitenConversionzauber Finanzsektor LeitfadenConversionzauberNoch keine Bewertungen

- KLRDokument2 SeitenKLRNiklas PetersenNoch keine Bewertungen

- Modulabschlussklausur BB02 SS2017Dokument2 SeitenModulabschlussklausur BB02 SS2017Elena RNoch keine Bewertungen

- Der Wertbeitrag der Kapitalstruktur bei der Bewertung von Unternehmen: Der Tax Shield im alten und im neuen UnternehmenssteuersystemVon EverandDer Wertbeitrag der Kapitalstruktur bei der Bewertung von Unternehmen: Der Tax Shield im alten und im neuen UnternehmenssteuersystemNoch keine Bewertungen

- RDB Tso LIdja20220404Dokument4 SeitenRDB Tso LIdja20220404benedikt thurnherNoch keine Bewertungen

- Kalkulation PDFDokument43 SeitenKalkulation PDFKrešo KorbeljNoch keine Bewertungen

- 4.3 Buchung Auf ErfolgskontenDokument6 Seiten4.3 Buchung Auf ErfolgskontenTiTOMNoch keine Bewertungen

- Externes Rechnungswesen Kontrollfragen Mit AntwortenDokument7 SeitenExternes Rechnungswesen Kontrollfragen Mit AntwortenMartinNoch keine Bewertungen

- Kosten-Und Leistungsrechnung: Vollkostenrechnung: Auszahlung Aufwand Kosten Einzahlung Ertrag LeistungDokument13 SeitenKosten-Und Leistungsrechnung: Vollkostenrechnung: Auszahlung Aufwand Kosten Einzahlung Ertrag LeistungAmina KamolovaNoch keine Bewertungen

- Probeklausur FinInv MitlösungenDokument10 SeitenProbeklausur FinInv Mitlösungenpalladium0Noch keine Bewertungen

- Prüfung Zum BuchhaltungsassistentenDokument2 SeitenPrüfung Zum BuchhaltungsassistentenScribdTranslationsNoch keine Bewertungen

- Handlers BeispieleDokument35 SeitenHandlers BeispieleChristtianNoch keine Bewertungen

- Grundlagen Der CashFlow-RechnungDokument16 SeitenGrundlagen Der CashFlow-RechnungFatih ÜnalNoch keine Bewertungen

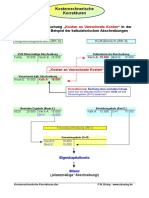

- Kostenrechnerische KorrekturenDokument1 SeiteKostenrechnerische KorrekturenhkfNoch keine Bewertungen

- Aufgabe 1 - Multiple ChoiceDokument9 SeitenAufgabe 1 - Multiple ChoiceHind TebbaiNoch keine Bewertungen

- 14.4.2023 Präs Finanzierung PDFDokument46 Seiten14.4.2023 Präs Finanzierung PDFKerstin RitterNoch keine Bewertungen

- BP Skript PPT Wiwi7 Termin 22.09.21 20.09.21 Controlling IIDokument29 SeitenBP Skript PPT Wiwi7 Termin 22.09.21 20.09.21 Controlling IIEnki BilalNoch keine Bewertungen